Financial crime has always evolved in response to controls. When banks improved sanctions screening, criminals used name variation, layering and intermediaries. When fraud teams deployed rules-based monitoring, fraudsters tested thresholds and changed transaction patterns. When cyber teams relied on signatures and indicators of compromise, malware authors developed polymorphic code that changed its appearance while preserving its intent.

Artificial intelligence has now accelerated that cycle.

Attackers are increasingly using AI to launch polymorphic attacks: campaigns that adapt in real time, at machine speed, to evade detection, exploit weaknesses and continue operating even as defenders respond. This is not simply “better malware” or “more convincing phishing.” It is a structural shift in the economics of cyber-enabled financial crime. AI reduces the time, cost and skill required to personalize attacks, modify malicious code, rotate infrastructure, generate synthetic identities, test controls and optimize fraud typologies.

For financial institutions, the implications are significant. The traditional model of detecting known bad activity through fixed rules, static signatures, blacklists and retrospective case reviews is no longer sufficient on its own. AI-enabled adversaries can observe defensive friction and adjust faster than many compliance, fraud and cybersecurity workflows can escalate, investigate and remediate.

Google Threat Intelligence Group has described a maturing shift toward the industrial-scale use of generative AI across adversarial workflows, including vulnerability exploitation and cyber operations. Palo Alto Networks’ Unit 42 has similarly warned that AI is changing the economics of intrusions by increasing attacker speed, scale and effectiveness.

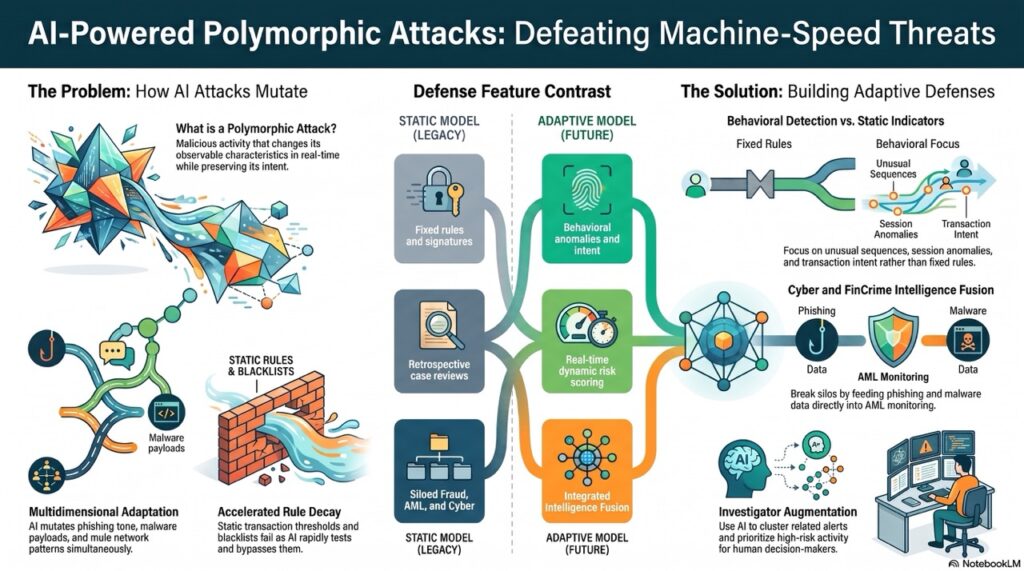

What Makes an Attack “Polymorphic”?

In cybersecurity, polymorphic malware refers to malicious code that changes its observable characteristics to avoid detection. The underlying purpose remains the same, but the form changes. The malware may alter file hashes, encrypt portions of its code, change execution paths, modify payloads or vary command-and-control behaviour.

AI expands this concept beyond malware. A modern polymorphic campaign may adapt across multiple dimensions at once:

The phishing email changes tone, language and pretext depending on the victim’s role.

The fraudulent onboarding journey changes device, document and behavioural signals.

The malware modifies its payload or obfuscation method after probing endpoint controls.

The mule account network changes transaction timing, payment rails and counterparties.

The social engineering script changes in real time based on the victim’s responses.

The attack infrastructure rotates domains, IPs, cloud services and communication channels.

In financial crime terms, this means typologies are becoming dynamic. Instead of a fixed fraud pattern that analysts can document, detect and tune against, institutions face campaigns that continuously mutate. The typology becomes less like a static checklist and more like an adaptive operating model.

Research into polymorphic malware detection has shown why this matters. Static antivirus tools can struggle against mutation techniques, while stronger results come from combining static rules, endpoint telemetry and network-layer analytics. One 2025 study found that integrated detection across antivirus, YARA/Sigma-style rules and endpoint telemetry produced substantially stronger coverage than any single layer alone.

Why This Matters for Financial Crime Teams

Financial institutions sit at the convergence point of cybercrime, fraud, money laundering and sanctions evasion. AI-powered polymorphic attacks do not respect internal organisational boundaries. A single campaign may begin as credential phishing, become account takeover, move into authorized push payment fraud, cash out through mule accounts, and then require transaction monitoring, fraud operations, cyber incident response and law enforcement engagement.

This creates several pressure points.

First, detection latency becomes a critical weakness. Machine-speed attacks can exploit the gap between alert generation, triage, escalation and interdiction. If a fraud control takes hours to identify a pattern, an adaptive campaign may have already changed its indicators, emptied accounts and moved funds across jurisdictions.

Second, rule decay accelerates. Traditional rules often depend on stable assumptions: known risky geographies, transaction thresholds, device fingerprints, keywords, IP ranges or behavioural patterns. AI-enabled attackers can test and evade those assumptions more quickly.

Third, false positives become more expensive. As criminals mimic legitimate behaviour more effectively, institutions may respond by tightening controls. But excessive friction can damage customer experience and overwhelm investigators. The challenge is not simply to detect more; it is to detect better.

Fourth, fraud and AML typologies become increasingly blended. Cyber intrusion data, behavioural biometrics, identity intelligence, transaction monitoring, sanctions exposure and open-source intelligence need to be connected. A suspicious transaction may only make sense when viewed alongside a recent device change, credential compromise, synthetic document, mule typology or phishing campaign.

Europol’s 2025 cybercrime reporting has highlighted the hidden economy of stolen data and the role of AI-generated content in modern cybercrime. This stolen data economy is directly relevant to financial crime because compromised credentials, identity documents, personal data and payment information are the raw materials for fraud, mule recruitment and money laundering.

The Financial Crime Attack Chain Is Becoming Adaptive

A practical example shows how these attacks may unfold.

An AI-enabled criminal group identifies employees, customers or high-net-worth individuals using breached data, social media, corporate filings and dark web intelligence. Generative AI creates highly tailored phishing messages, voice scripts or deepfake-enabled impersonation attempts. The campaign automatically tests which message formats produce engagement.

Once credentials are captured, the attacker adapts. If multi-factor authentication blocks access, the campaign shifts to device-code phishing, session hijacking, push fatigue or social engineering against support teams. If endpoint tools block a payload, the malware mutates. If transaction rules block a payment, the funds are split, delayed, rerouted or moved through alternative rails.

The attack does not follow a fixed script. It behaves like a feedback loop.

This is particularly dangerous in financial crime because criminals are not only trying to breach systems; they are trying to monetize access. The value chain includes identity takeover, payment fraud, invoice redirection, card testing, mule account usage, crypto conversion, trade-based laundering, sanctions circumvention and data extortion.

In this environment, compliance teams cannot treat cyber signals as separate from financial crime controls. A compromised account is not just an IT event. It may be the opening stage of fraud, money laundering or market abuse.

Why Static Defences Are No Longer Enough

Many institutions still rely heavily on static or semi-static controls. These include fixed transaction thresholds, list-based screening, rules-based alerting, known-bad indicators, periodic typology refreshes and manual post-event investigations. These controls remain important, but they are insufficient against adaptive adversaries.

AI-enabled polymorphic campaigns exploit predictable controls. If a bank’s fraud rule blocks transfers above a certain amount, the attack can break payments into smaller values. If a sanctions control depends on exact name matching, criminals can vary spelling, intermediaries and corporate structures. If an endpoint tool relies on known malware hashes, polymorphic code can change the hash. If onboarding checks detect a known synthetic identity pattern, AI can generate new document, image and behavioural variations.

The defender’s challenge is therefore to identify intent and behaviour, not merely indicators.

This requires a shift from static detection to adaptive detection. Institutions need controls that can learn from emerging patterns, correlate weak signals, detect behavioural anomalies, and escalate risk dynamically across customer, account, device, transaction and network levels.

Building a FinCrime Defence Model for Machine-Speed Attacks

A stronger response starts with convergence. Financial crime, fraud, cyber, compliance, data science and threat intelligence teams need shared visibility and shared operating protocols. AI-powered attacks move too quickly for siloed teams to exchange information through slow handoffs.

Key defensive priorities include:

- Behavioural detection over static indicators

Institutions should focus on behavioural analytics that detect unusual sequences, velocity, device behaviour, beneficiary changes, session anomalies and transaction intent. A single indicator may be weak, but a chain of weak signals can reveal a high-risk event. - Real-time risk scoring

Customer and transaction risk should update dynamically based on live signals. A customer logging in from a new device after a phishing campaign, changing contact details and initiating a high-risk payment should not be treated the same as a normal returning user. - Cyber and FinCrime intelligence fusion

Threat intelligence about phishing domains, malware campaigns, credential leaks, bot activity and mule networks should feed directly into fraud and AML monitoring. Conversely, suspicious transaction patterns should inform cyber investigations. - Adaptive model governance

Financial institutions using AI defensively must ensure model explainability, validation, bias testing and auditability. Regulators will expect institutions to understand not only that a model works, but how it works, when it fails and how decisions are governed. - Red-teaming and control testing

Institutions should test their controls against adaptive attack scenarios, not just known typologies. This includes simulations of AI-generated phishing, synthetic identity variation, mule network behaviour, malware mutation and real-time evasion of transaction rules. - Investigator augmentation

AI should also support defenders by summarizing cases, clustering related alerts, identifying typology drift, enriching entities and prioritizing high-risk activity. The goal is not to replace investigators, but to reduce noise and increase decision speed. - Stronger identity and authentication controls

As AI improves impersonation and social engineering, institutions need layered identity assurance. This may include phishing-resistant authentication, device binding, behavioural biometrics, step-up verification and stronger controls around account recovery. - Scenario-based resilience planning

Boards and senior management should treat AI-enabled polymorphic attacks as an enterprise risk, not a niche technical issue. Crisis playbooks should cover cyber intrusion, fraud loss, regulatory reporting, customer harm, law enforcement engagement and communications.

The Regulatory and Governance Dimension

Financial institutions are expected to maintain systems and controls proportionate to their risks. As AI changes the threat landscape, regulators will increasingly scrutinize whether institutions have adapted their control environment accordingly.

The governance question is simple: if attackers can change faster than your controls, how does your institution know that its financial crime framework remains effective?

This requires evidence. Institutions should be able to demonstrate typology refresh cycles, alert effectiveness, fraud loss trends, model monitoring, incident learnings, customer harm analysis, suspicious activity reporting quality and board-level oversight.

The Reserve Bank of India’s 2026 Financial Stability Report reportedly identified AI-enabled cyberattacks as a major near-term cyber threat for the financial system, reflecting broader supervisory concern that AI-driven attacks could affect operational resilience and financial stability. (

From Detection to Adaptation

The core lesson is that financial institutions cannot defeat adaptive attacks with purely static controls. The defensive model must itself become adaptive.

This does not mean blindly deploying AI everywhere. Poorly governed AI can create false positives, opaque decisions, privacy issues and regulatory exposure. But refusing to modernize is also risky. Criminals are already using automation, generative AI and real-time optimization to increase scale and precision.

The institutions best positioned to respond will be those that combine intelligence-led investigation, behavioural analytics, cyber-fincrime convergence, strong governance and rapid feedback loops. They will not rely solely on known indicators. They will look for changing intent, abnormal behaviour and emerging typologies.

AI-powered polymorphic attacks represent a new phase in financial crime: faster, more personalized, more evasive and more scalable. The answer is not just better technology. It is better integration between people, process, data and controls.

In the machine-speed era of financial crime, the winning defence is not the one that knows yesterday’s attack pattern. It is the one that can recognize tomorrow’s mutation before the money moves.

GIPHY App Key not set. Please check settings