Marking the close is a form of manipulative trading in which a person buys or sells a financial instrument near the end of the trading session with the aim, or effect, of distorting the closing price or creating a misleading impression about the instrument’s value. ESMA’s market-abuse materials describe it as buying or selling at the close of the market with the effect of misleading investors acting on the basis of closing prices, and FINRA’s oversight materials continue to treat marking the close as a live manipulative-trading risk.

In the financial crime environment, marking the close is significant because the closing price is not just an end-of-day datapoint. It can influence portfolio valuations, fund NAVs, benchmark calculations, derivative settlements, margin calculations, performance reporting, and investor decisions. If that price is manipulated, the harm can extend beyond one trade to a wide range of downstream valuations and market outcomes. The FCA states that market abuse damages market integrity and investor confidence, and FINRA identifies manipulative trading as prohibited conduct under several rules.

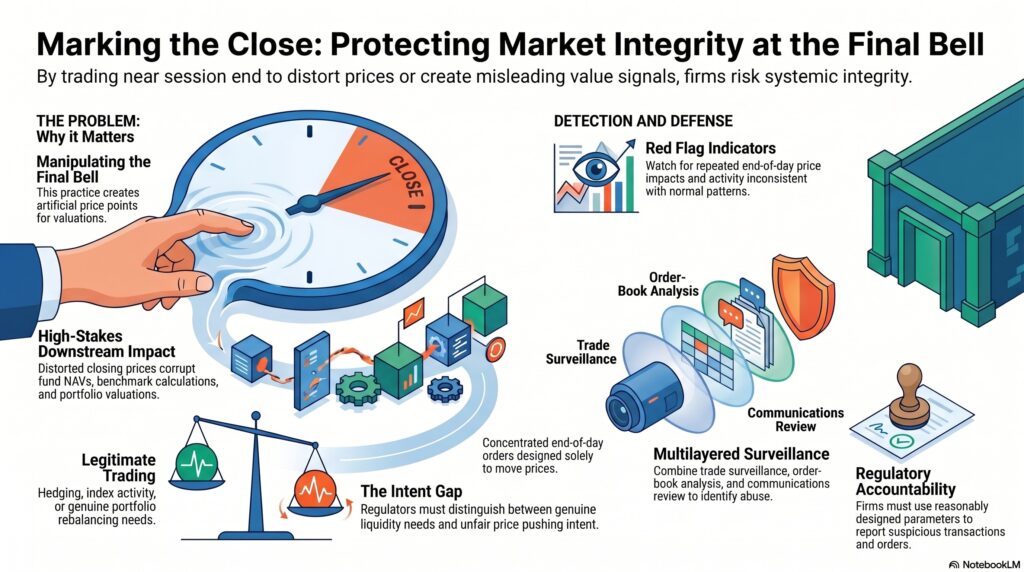

From a professional perspective, marking the close is a market-integrity offence because it exploits the market’s reliance on the closing price as a trusted reference point. A trader may place aggressive orders or execute transactions near the close not for genuine investment or hedging reasons, but to push the price in a favorable direction. That may benefit an existing position, improve reported performance, influence a benchmark-linked exposure, or create a misleading market signal. This is an inference supported by ESMA’s description of the practice and by FINRA’s ongoing treatment of it as manipulative trading.

Watch on YouTube: Marking the Close

A key issue is that trading near the close is not automatically abusive. Legitimate trading, portfolio rebalancing, hedging, index activity, and genuine liquidity needs can all occur late in the session. The regulatory question is whether the conduct had a legitimate commercial rationale or whether it was intended, or structured, to influence the closing price unfairly. FCA materials note that signals of market manipulation are not exhaustive or determinative on their own, because a transaction meeting one or more signals may still have a legitimate explanation.

That means detection depends heavily on context. Relevant indicators may include concentrated trading near the close, repeated end-of-day price impact, activity inconsistent with normal trading patterns, benefit to an existing position or valuation point, and communications or order behavior suggesting intent to move the price. FINRA’s 2026 oversight report specifically lists marking the close as one of the manipulative trading schemes firms should surveil for with reasonably designed parameters and thresholds.

For firms, effective control requires a mix of trade surveillance, order-book analysis, communications review, and governance. Surveillance should be able to identify potentially price-moving activity around the close, link it to positions and other incentives, and distinguish normal end-of-day execution from manipulative behavior. Where firms operate in markets subject to MAR or similar regimes, suspicious patterns may also need escalation through internal market-abuse processes and, where appropriate, suspicious transaction and order reporting. This is an inference supported by the FCA’s market-abuse framework and FINRA’s manipulative-trading guidance.

Ultimately, marking the close matters in the financial crime environment because it targets one of the market’s most important reference prices. By distorting the closing level, the misconduct can affect valuations, investor perception, and market confidence far beyond the individual trade itself. For that reason, it should be treated as a serious market-abuse risk requiring strong surveillance, clear escalation, and disciplined governance.