eComms surveillance refers to the monitoring, review, capture, and analysis of electronic communications used in business activity, including email, chat, messaging platforms, collaboration tools, and other digital channels. In the financial crime environment, it is a core control because misconduct is often discussed, coordinated, or concealed through communications before it becomes visible in trades, payments, or account activity. The FCA has reaffirmed that firms must record, monitor, and keep auditable relevant electronic communications, and take reasonable steps to prevent staff from using unrecorded channels for in-scope business activity.

From a professional financial crime perspective, eComms surveillance is not simply a recordkeeping exercise. It is a detection and evidencing function. Transaction data can show what happened, but electronic communications often help explain why it happened, whether there was intent, whether multiple parties were coordinating, and whether someone knew the conduct was improper. This makes eComms surveillance particularly relevant to market abuse, insider dealing, unlawful disclosure, fraud, bribery and corruption, sanctions evasion, and off-channel misconduct. ESMA’s market integrity framework is explicitly aimed at protecting European financial markets from insider dealing, unlawful disclosure, and market manipulation.

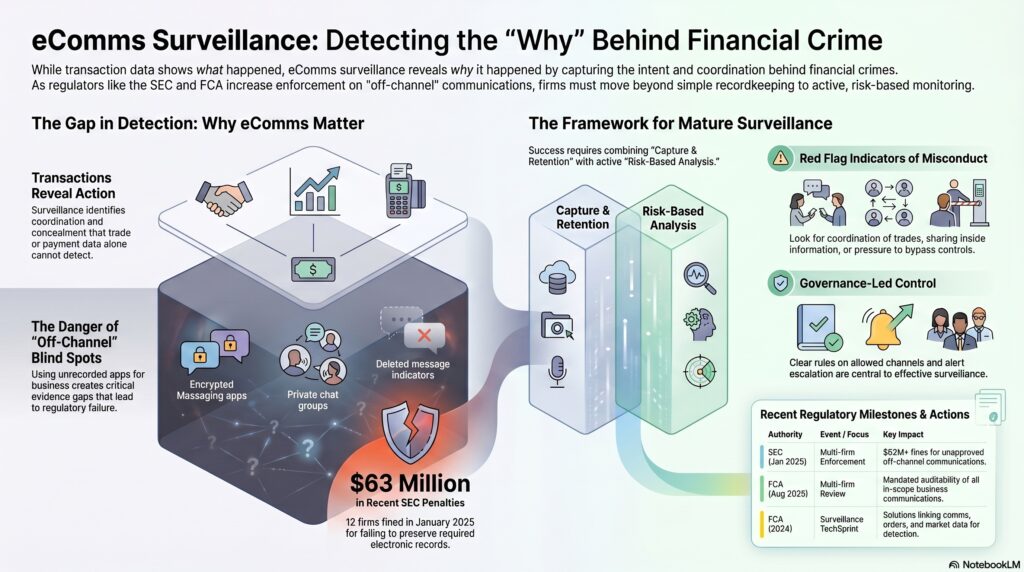

A major reason eComms surveillance has become more important is the expansion of communication channels. Business discussions no longer occur only through corporate email and recorded phone lines. Staff may use chat tools, collaboration platforms, mobile messaging, and other digital channels in ways that create surveillance blind spots if the firm’s capture and monitoring arrangements are weak. The FCA’s August 2025 multi-firm review on off-channel communications states that firms must ensure communications related to in-scope activities are auditable and that they must take reasonable steps to prevent employees from using unrecorded channels for those communications.

Watch on YouTube: eComms Surveillance

This has direct regulatory significance. The SEC announced in January 2025 that twelve firms agreed to pay more than $63 million combined over failures involving unapproved off-channel communications, and said those failures involved personnel at multiple levels, including supervisors and senior managers. The core issue was not only that the firms used the wrong channels, but that records required under securities laws were not preserved. In the financial crime environment, that matters because if relevant communications are not captured, the firm and regulators may lose critical evidence of misconduct, decision-making, and intent.

A mature eComms surveillance framework therefore has two linked objectives. The first is capture and retention: ensuring that relevant business communications occur on approved channels and are preserved in a reviewable form. The second is risk-based surveillance: analyzing those communications for indicators of misconduct. Firms that achieve only the first objective may satisfy a basic recordkeeping requirement without actually detecting much. Firms that attempt the second without the first will have major blind spots because the relevant evidence may never enter the surveillance environment at all. This inference is supported by the FCA’s rules on recording and monitoring and the SEC’s enforcement focus on off-channel and unpreserved communications.

In practical terms, eComms surveillance often looks for indicators such as discussion of confidential information, attempts to coordinate trading or client activity improperly, references to workarounds or concealment, inappropriate sharing of inside information, pressure to avoid controls, or use of side channels for business discussions. Increasingly, firms are also correlating communications with trade and order data. The FCA’s 2024 Market Abuse Surveillance TechSprint highlighted solutions that linked communications, orders, and market data to identify potentially coordinated manipulative behavior.

This is especially important in market abuse surveillance. A suspicious trade pattern may be difficult to interpret on its own, but the surrounding electronic communications may show whether staff were discussing inside information, pre-arranging conduct, or attempting to influence prices or liquidity. FCA Market Watch 69 and later FCA communications continue to stress the importance of effective surveillance arrangements for firms subject to market abuse surveillance obligations.

Governance is central to all of this. Effective eComms surveillance requires clear decisions about which channels are allowed, which staff populations are higher risk, how communications are captured, how alerts are triaged, who reviews them, and when matters escalate into compliance, legal, HR, or regulatory reporting. Weak governance can leave firms with a nominal surveillance programme but poor practical visibility. The FCA’s off-channel review and the SEC’s recent enforcement actions both point to the same lesson: without strong governance, firms can drift into unrecorded and unsupervised communications habits that materially weaken the control environment.

Ultimately, eComms surveillance is a critical financial crime and conduct control because many serious risks are communicated before they are executed. It helps firms detect intent, coordination, concealment, and awareness in ways that payment monitoring or trade surveillance alone cannot. In a digital business environment, it is also inseparable from channel governance and recordkeeping discipline. A firm that cannot capture and analyze relevant electronic communications is likely to have significant blind spots in its broader financial crime framework.