First-party fraud is a financial crime typology in which a genuine customer, or someone acting through a genuine customer relationship, deliberately misrepresents information, abuses a product, or dishonestly disputes a legitimate obligation for financial gain. Industry definitions commonly distinguish it from third-party fraud because the offender is not primarily impersonating someone else; instead, they are using their own identity, a real customer relationship, or a transaction tied to them while introducing deception into the application, payment, repayment, or dispute process. This makes first-party fraud especially difficult to detect because many of the identity signals that would normally indicate legitimacy can still appear valid.

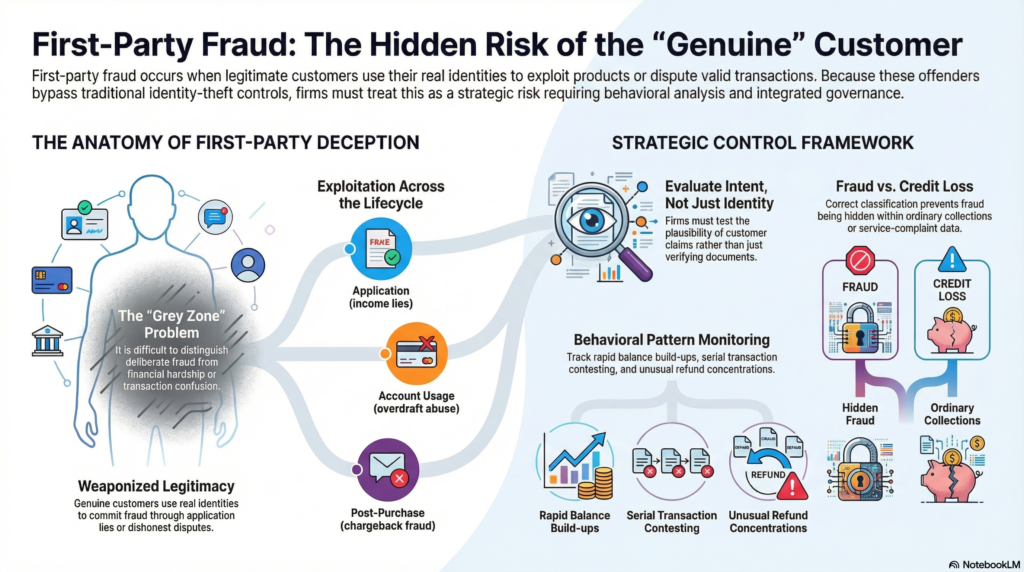

In the financial crime environment, first-party fraud is significant because it sits in a grey zone between ordinary customer default, abusive conduct, and deliberate criminal deception. A customer may exaggerate income on a credit application, open an account with no intention of using it legitimately, run up balances they never intended to repay, falsely claim that a genuine transaction was unauthorized, or exploit refund and chargeback mechanisms after receiving the goods or services. Some firms and industry bodies also treat “friendly fraud” as a subset or close relative of first-party fraud, particularly where a genuine cardholder intentionally or opportunistically disputes a valid purchase. The operational challenge is that the customer is real, the relationship may be real, and the transaction may have been technically authorized, yet the conduct is fraudulent in substance.

From a professional control perspective, first-party fraud is best understood as an abuse of trust embedded in the customer lifecycle. Traditional fraud controls are often designed to detect imposters, stolen identities, counterfeit credentials, or account compromise. First-party fraud bypasses much of that logic because the individual may satisfy onboarding checks, authentication checks, and account ownership checks while still acting deceptively. That means the core risk is not simply “who is the customer,” but whether the customer’s intent, representations, and later conduct are honest. This is why first-party fraud should not be treated as a narrow disputes issue or a routine collections problem. It is a strategic control risk that can affect onboarding, credit underwriting, transaction monitoring, dispute management, merchant risk, and financial crime governance.

The typology can emerge at several points in the product lifecycle. At application stage, it may involve false statements about income, employment, affordability, business purpose, or intended use of funds. In lending environments, this can shade into first-party lending fraud, where the institution is induced to provide credit on a knowingly false basis. During account usage, the customer may deliberately exploit overdrafts, promotional incentives, buy-now-pay-later structures, or short-term credit with no genuine intention of honoring the obligation. At the post-purchase stage, first-party fraud may present through abusive chargebacks, false claims of non-receipt, or disputes over transactions that were in fact recognized and authorized. This breadth is important because first-party fraud is not one scenario; it is a family of deceptive behaviors that exploit different stages of the customer relationship.

Watch on YouTube: First-Party Fraud

One of the reasons first-party fraud is so challenging is that it is often difficult to distinguish from adjacent non-criminal outcomes. A genuine customer may default because of hardship rather than deception. A cardholder may dispute a transaction because of confusion rather than dishonesty. A household member may use a stored card without the primary cardholder’s knowledge, creating a contested transaction that is neither classic third-party fraud nor a straightforward criminal chargeback. Mastercard’s discussion of first-party and friendly fraud highlights this problem of transaction confusion, where a legitimate charge is mistaken for fraud, as well as cases involving household misuse and intentional false disputes. For firms, that ambiguity creates a serious evidential burden: they must identify deceptive intent without collapsing all customer error or distress into fraud treatment.

This ambiguity has direct implications for financial crime management. Because the identity is genuine, first-party fraud can be under-classified, written off as credit loss, or absorbed into ordinary customer-service operations rather than recognized as deliberate abuse. That weakens institutional visibility and can distort risk appetite decisions. Where firms fail to classify first-party fraud accurately, they may underestimate loss drivers, underinvest in controls, and miss links between abusive disputes, credit abuse, account misuse, and repeat conduct across products or channels. The result is that a meaningful part of the fraud landscape may remain hidden inside broader portfolios of delinquencies, chargebacks, refunds, or “customer complaints.” This inference is supported by industry descriptions of first-party fraud as especially hard to detect because the customer and account may appear genuine.

In the wider financial crime ecosystem, first-party fraud can also intersect with other typologies. A customer who commits first-party lending fraud may later use the account for suspicious fund movements. Abusive disputes can overlap with merchant fraud exposure and refund abuse. Repeated deception by a real customer can coexist with mule activity, collusive behaviour, or misuse of accounts to receive or pass on criminal proceeds. Not every first-party fraud case is a money laundering case, but some are part of broader patterns of deception and value extraction that should concern fraud, AML, and payments teams alike. Industry material on first-party abuse and dispute fraud, combined with broader fraud-governance guidance, supports treating the issue as more than a narrow consumer-credit problem.

A mature control framework therefore needs to assess intent and behaviour, not just identity validity. At onboarding, firms should test plausibility as well as document quality: do the declared income, employment, business purpose, and requested product make sense together? During the life of the account, they should monitor for patterns consistent with abuse, such as rapid balance build-up followed by non-payment, repeated use of promotional offers without normal repayment behaviour, unusual refund or dispute concentration, serial transaction contesting, and account activity inconsistent with the stated purpose of the relationship. In merchant and card environments, strong post-purchase evidence, clear billing descriptors, customer communication, and dispute analytics are also critical because many first-party fraud cases surface through the dispute channel rather than at authorization. This approach is consistent with the payment-industry focus on preventing and deflecting friendly fraud and post-purchase misuse.

Detection is only part of the response. Governance is equally important. First-party fraud should appear explicitly in fraud taxonomies, product risk assessments, underwriting governance, collections strategy, dispute management frameworks, and management information. Firms need to know where the exposure sits: which products, customer segments, channels, and merchant categories are most affected; how often suspicious disputes recur; how much apparent credit loss may actually be fraud loss; and whether abusive behaviour is clustered around particular acquisition routes or customer journeys. Where these data points are absent, the institution is likely to treat first-party fraud as noise rather than as a material control issue. The growing payments-industry emphasis on first-party misuse and dispute prevention supports this more formal governance approach.

There is also a customer-treatment dimension that requires care. Some cases involve deliberate abuse and should be treated as fraud. Others involve confusion, family misuse, poor descriptor recognition, or financial distress. A professionally mature framework should therefore avoid binary assumptions and apply proportionate investigation, evidence review, and escalation. Overly aggressive treatment can create conduct and reputational risk; overly passive treatment can normalize abuse and increase losses. The control objective is to separate misunderstanding from deception, and opportunism from genuine hardship, while preserving a consistent standard for what constitutes dishonest customer conduct. Mastercard’s treatment of transaction confusion and first-party dispute abuse illustrates why this distinction matters operationally.

Ultimately, first-party fraud is a serious financial crime risk because it weaponises the legitimacy of the genuine customer relationship. It allows a real customer, or a real account context, to be used deceptively in order to obtain credit, reverse valid transactions, abuse products, or externalize financial loss onto firms and merchants. In a modern financial services environment, where much of the control architecture is designed to distinguish genuine customers from imposters, first-party fraud presents a more difficult challenge: the customer may be genuine, but the conduct is not. For that reason, first-party fraud should be treated as a core element of the financial crime landscape, requiring integrated underwriting controls, behavioural analytics, dispute intelligence, governance, and coordinated action across fraud, payments, credit, collections, and compliance functions.