Payment fraud is a broad and evolving financial crime typology involving the unauthorized, deceptive, or manipulated movement of funds through payment channels, instruments, or related account infrastructure. In the financial crime environment, it is not limited to stolen card usage or isolated unauthorized transactions. It includes a wide spectrum of abuse across cards, accounts, digital wallets, instant payments, e-commerce, account-to-account transfers, merchant relationships, and payment initiation processes. At its core, payment fraud is about exploiting weaknesses in trust, authentication, transaction flow, or user behaviour in order to extract value, disguise illicit movement, or shift financial loss onto victims, institutions, or counterparties.

From a professional financial crime perspective, payment fraud is best understood as both a direct loss event and a broader control-risk issue. A fraudulent payment is often the visible output of a much larger chain of compromise. That chain may begin with stolen credentials, identity theft, account takeover, social engineering, mule recruitment, merchant abuse, or the manipulation of internal or customer-facing processes. By the time the payment itself is initiated, the underlying controls that should have prevented misuse may already have been weakened or bypassed. For this reason, payment fraud should not be treated as a narrow operational issue confined to disputes or chargebacks. It is a cross-functional risk that intersects with fraud prevention, AML, sanctions, cyber security, customer authentication, third-party risk, and operational resilience.

One of the defining features of payment fraud is its adaptability. Criminals tailor their methods to the payment rail, the speed of execution, the available controls, and the institution’s response capabilities. In card environments, this may involve card-not-present fraud, use of compromised card data, testing attacks, or abuse of stored credentials. In account-based environments, it may involve unauthorized transfers, fraudulently induced payments, takeover of online banking credentials, or manipulation of payee setup and account profile data. In merchant and acquiring contexts, the risk can include fraudulent merchants, transaction laundering, refund abuse, triangulation fraud, or collusive activity designed to exploit settlement mechanisms. In real-time payment environments, the typology becomes more acute because detection windows narrow significantly and recovery opportunities diminish once funds are released.

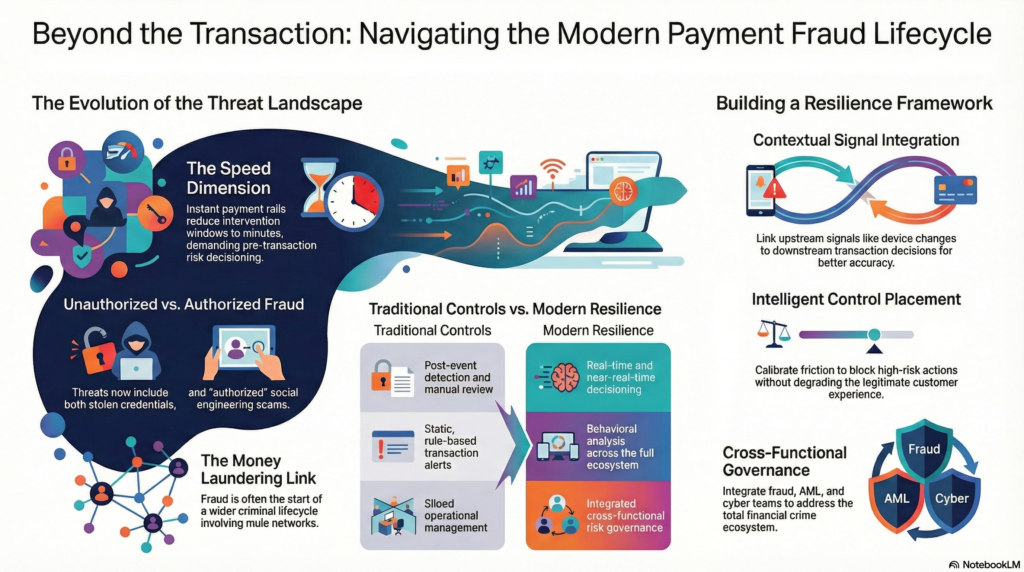

This speed dimension is especially important in modern financial services. Traditional payment controls often relied on post-event detection, delayed settlement, or manual review before final loss crystallised. Faster and instant payment rails reduce that margin for intervention. Fraudulent funds can move from the originating account to mule networks and onward dispersal within minutes, leaving institutions with limited opportunity to stop, reverse, or recover the proceeds. As a result, payment fraud increasingly demands pre-transaction and near-real-time risk decisioning rather than reliance on retrospective review. Institutions that cannot detect suspicious payment behaviour before or during execution are likely to face higher losses, weaker recovery outcomes, and greater exposure to wider laundering risk.

Watch on YouTube: Payment Fraud

Payment fraud is also highly dependent on context. The same payment may be legitimate or fraudulent depending on surrounding factors such as device behaviour, account history, payee novelty, channel usage, customer vulnerability, authentication path, or prior changes made to the profile. This means that static rule-based controls, while still useful, are rarely sufficient on their own. A professionally mature framework evaluates the payment not in isolation, but as part of an event chain. A transfer to a new beneficiary immediately after a password reset, mobile number change, and login from an unfamiliar device presents a very different risk profile from an equivalent payment made under stable account conditions. Effective payment fraud detection therefore relies on linking upstream signals to downstream transaction decisions.

In the financial crime environment, payment fraud also has a strong relationship with money laundering risk. Fraud-generated funds often require rapid movement and concealment, and payment channels provide the mechanism through which this occurs. Mule accounts, intermediary wallets, shell businesses, complicit merchants, and layered transfer patterns can all be used to move or obscure the proceeds of fraud. This means a fraudulent payment may not be the end of the crime but the start of another stage in the criminal lifecycle. An institution that identifies only the initial fraud loss without examining downstream flows may miss associated suspicious activity, organized network behaviour, or evidence of wider criminal coordination. For this reason, fraud teams and AML teams should not operate in complete separation where payment fraud is concerned. The typology often sits directly between them.

A further complexity is that payment fraud increasingly includes both unauthorized and authorized components. Unauthorized payment fraud involves transactions made without the genuine customer’s knowledge or consent, often using stolen credentials, compromised payment instruments, or account takeover. Authorized fraud, by contrast, occurs when the customer is manipulated into initiating the transaction themselves under false pretences, as seen in impersonation scams, invoice redirection fraud, romance scams, investment fraud, and other forms of social engineering. From a financial crime standpoint, both are significant. The distinction may matter for reimbursement, legal treatment, or consumer protection obligations, but in operational terms both involve criminal exploitation of payment systems and both require robust prevention and detection frameworks.

Institutions must therefore understand payment fraud as a lifecycle threat rather than a single event. The relevant control question is not only whether a suspicious payment can be identified, but also whether the conditions that enabled it were visible earlier in the customer journey. Were there indications of identity compromise, abnormal login behaviour, profile changes, new payee creation, unusual device activity, or scripted customer interaction? Was the merchant relationship itself suspicious? Were there previously overlooked red flags around onboarding, beneficiary risk, channel abuse, or transaction velocity? The strongest payment fraud frameworks are those that connect these signals into a coherent risk narrative, rather than assessing each event in a silo.

Preventive controls in this area must be layered and proportionate. Strong customer authentication, secure credential management, robust device and session analysis, trusted payee mechanisms, step-up verification for high-risk actions, payee-confirmation processes, and targeted friction for anomalous payments all have a role. However, control design must be calibrated carefully. Too little friction exposes the institution to loss; too much friction can degrade customer experience, increase abandonment, and create operational inefficiency. Professional payment fraud management therefore depends on intelligent control placement: introducing friction where risk is elevated, while allowing low-risk legitimate transactions to proceed efficiently. This is particularly important in digital-first businesses where payment experience is commercially sensitive.

Detection capability must extend beyond the payment instruction itself. High-performing institutions monitor for behavioural anomalies across the full payment ecosystem, including login events, authentication failures, device changes, unusual account navigation, beneficiary additions, profile updates, transaction splitting, repeated testing payments, abnormal merchant activity, and linked-party relationships. They also assess the characteristics of the receiving side where possible, including mule indicators, shared identifiers, unusual beneficiary concentration, and suspicious network patterns. The aim is not simply to detect a single fraudulent payment, but to identify the broader pattern in which the payment sits. That broader perspective is what allows institutions to move from reactive loss management to proactive crime disruption.

Operational response is equally critical. Once suspected payment fraud is identified, firms need clear escalation pathways covering transaction hold or decline decisions, customer contact, account restriction, beneficiary review, internal investigation, suspicious activity assessment, and recovery action where feasible. In many cases, the payment event may warrant simultaneous review by fraud operations, AML investigations, cyber teams, and customer service functions. A single high-risk payment may indicate account takeover, social engineering victimization, mule usage, or organized fraud activity across multiple customers. Without coordinated handling, important intelligence may be lost and the institution may respond only to the immediate transaction rather than the wider criminal pattern.

Governance and assurance are also central. Payment fraud should be represented explicitly in fraud risk assessments, financial crime typologies, product approval processes, payment-control design reviews, scenario testing, and management information. Institutions should understand which rails, customer segments, counterparties, and transaction journeys generate the highest exposure, and whether their existing controls reflect current criminal methods rather than historic assumptions. Metrics such as fraud attempt rates, confirmed loss rates, false-positive volumes, intervention timing, scam typologies, mule-linked beneficiaries, and recovery outcomes can help measure whether the framework is operating effectively. Payment fraud environments change quickly, and control frameworks that are not actively reviewed and recalibrated tend to degrade faster than management expects.

There is also a major customer harm and reputational dimension. Payment fraud can result in immediate financial loss, disrupted access to funds, emotional distress, operational inconvenience, and erosion of trust in the institution’s ability to safeguard transactions. In business settings, it can also create contractual disputes, merchant disruption, settlement issues, and legal liability. A professionally mature response must therefore combine security with clarity, fairness, and timely customer communication. Institutions that respond well not only contain losses more effectively, but also preserve customer confidence in the integrity of their payment environment.

Ultimately, payment fraud is a core financial crime threat because it weaponises the movement of money itself. It exploits trust in payment instruments, accounts, merchants, users, and transaction flows to generate unlawful value and, in many cases, to support the onward movement of illicit proceeds. In a modern environment shaped by digital channels, instant settlement, and increasingly sophisticated criminal methods, payment fraud can no longer be addressed through isolated transaction review or narrow operational controls. It requires an integrated framework combining fraud prevention, identity assurance, AML awareness, behavioural analytics, real-time decisioning, effective investigations, and strong governance. Only by treating payment fraud as a central part of the financial crime ecosystem can institutions build controls that are resilient, proportionate, and credible.