An Indication of Interest (IoI) is a non-firm expression of trading interest used in securities markets to communicate that a person or firm may be willing to buy or sell a financial instrument, usually at or around a particular size or price, but without creating the binding commitment associated with a firm quote or executable order. In market practice, IoIs are commonly used to signal potential liquidity, invite engagement, and support price discovery in less transparent or less continuously quoted environments. FINRA materials and related market-structure discussions treat IoIs as communications of trading interest rather than firm commitments.

In the financial crime environment, IoIs matter because they sit at the intersection of market conduct, communications control, and market integrity. Although an IoI is not itself a trade, it can influence market expectations, reveal or imply client interest, shape order-flow behavior, and create opportunities for misuse if it is false, misleading, improperly labeled, or based on confidential information. That means IoIs are not just a trading convenience. They are a communication channel capable of creating conduct risk and, in some cases, market-abuse risk. FCA market-abuse materials emphasize that firms need safeguards against abusive conduct, while FINRA has specifically focused on the accuracy and origin of IoIs.

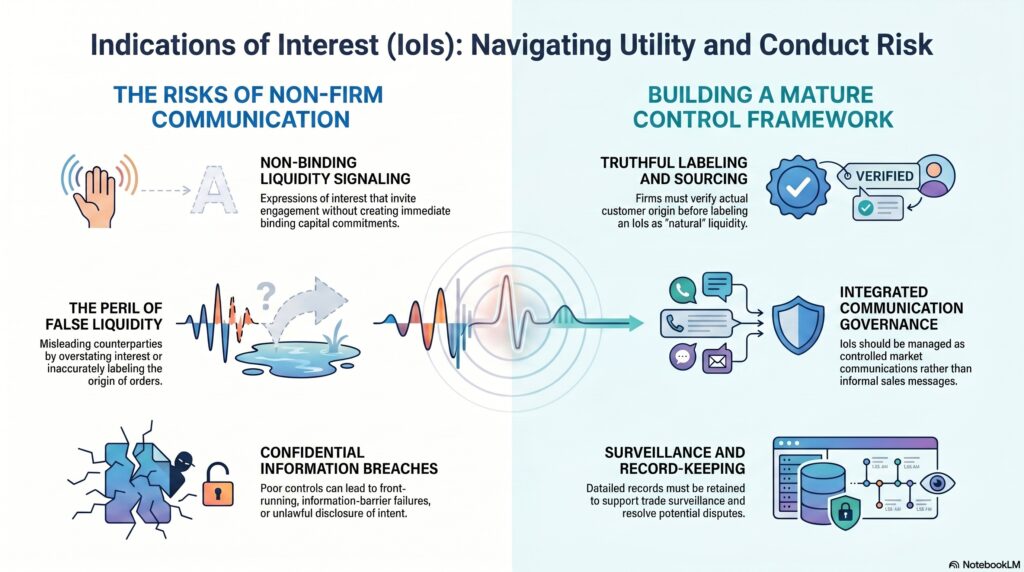

From a professional perspective, the key feature of an IoI is that it expresses interest without firmness. That flexibility is commercially useful because it allows market participants to signal liquidity and test interest without committing capital immediately. But the same flexibility creates control challenges. If an IoI overstates genuine interest, implies customer origin when none exists, or is used to create a false impression of liquidity or demand, it can distort fair market behavior. FINRA’s Regulatory Notice 11-43 addressed this directly by proposing that firms should have received a customer order before displaying a quotation or IoI in a way that purports to represent customer origin, such as labeling it “natural.”

Watch on YouTube: Indication Of Interest (IoI)

This is why IoIs are relevant to the financial crime environment even though they are not, on their face, AML tools or fraud products. The central risk is misrepresentation. An IoI can become problematic if it is used to imply false liquidity, mislead counterparties about the existence of a customer order, signal information that should remain confidential, or facilitate conduct that edges toward manipulation. In that sense, IoIs raise issues of honesty, fair dealing, communications governance, and sometimes market abuse. This is an inference supported by FINRA’s focus on truthful labeling and by broader FCA/ESMA market-integrity frameworks.

IoIs are especially sensitive where they intersect with confidential client information. If a firm communicates an IoI that reflects client interest, pending block activity, or inside information without proper controls, it may expose the firm to front-running risk, information-barrier failure, or unlawful disclosure concerns. That is why IoI governance is closely tied to control-room functions, information barriers, restricted lists, and front-office supervision. In professional terms, the question is not only whether the IoI is non-firm, but whether it is accurate, appropriately sourced, and properly controlled. This is an inference supported by the cited FINRA treatment of customer-origin labeling and the FCA’s wider market-abuse framework.

IoIs are also relevant because they sit inside the broader category of electronic trading communications. Modern markets often use systems designed to communicate trading interest in dealer-to-customer and other market segments. The SEC’s 2023 market-structure release discussed such systems as significant means of communicating trading interest, which shows that these communications are part of live regulatory thinking about market access and structure. In practical financial crime terms, this means IoIs should be governed not just as informal sales messages, but as controlled market communications that can affect price formation, client treatment, and surveillance outcomes.

A mature control framework for IoIs therefore requires clear standards around when they may be sent, what they may say, how they may be labeled, and how they are supervised. Firms should understand whether the IoI reflects proprietary interest, customer interest, or more general market color; whether it could reveal confidential or inside information; whether it is consistent with firm rules on fair dealing and communications; and whether records are retained for surveillance and review. If IoIs are used loosely, they can create ambiguity that makes later surveillance or dispute resolution harder. If they are used in a disciplined way, they can support legitimate liquidity-seeking activity without compromising market integrity. This is an inference grounded in the cited regulatory treatment of truthful and properly sourced IoIs.

Ultimately, an Indication of Interest is important in the financial crime environment because it is a non-firm market communication that can still have real conduct, surveillance, and integrity implications. Its commercial purpose is to express possible trading interest, but its regulatory significance lies in whether that expression is honest, controlled, and free from misuse of confidential information or misleading market signals. For that reason, IoIs should be treated as part of the firm’s broader market-conduct and communications-control framework, not merely as informal trading language.