A cardholder is the individual or entity to whom a payment card is issued, or the person authorized to use that card under the card account terms. In the financial crime environment, the cardholder is not simply the owner of a card product. The cardholder is a central participant in the payment ecosystem because card-based fraud, disputes, authentication controls, chargebacks, account abuse, and reimbursement decisions often depend on whether activity can properly be attributed to the legitimate cardholder and whether that activity was genuinely authorized.

From a professional financial crime perspective, the importance of the cardholder lies in the relationship between identity, authority, and liability. Card payment controls are built around the assumption that the person using the card, or the associated card credentials, is the legitimate and authorized cardholder. When that assumption fails, the result may be card-not-present fraud, counterfeit card use, account takeover, friendly fraud, first-party fraud, or disputed transactions. This makes the cardholder concept foundational to card fraud management. The issue is not only who holds the card, but whether the person initiating the transaction is acting with legitimate authority and whether the cardholder relationship is being misused or impersonated.

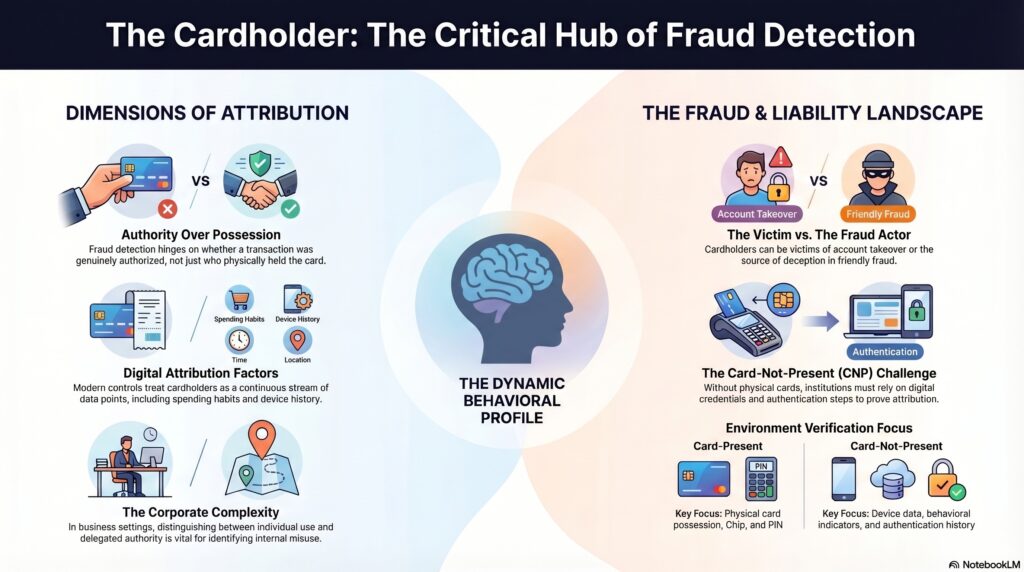

In card-present environments, the cardholder is traditionally linked to physical possession of the card and, depending on the payment method, the use of chip, PIN, or other verification measures. In card-not-present environments, the cardholder relationship becomes more complex because the physical card is absent and the institution must rely on card credentials, authentication steps, device data, behavioral indicators, and transaction context. In these situations, the financial crime question is not whether the card exists, but whether the transaction is truly attributable to the legitimate cardholder. This is why cardholder authentication is such a critical part of payment fraud controls.

Watch on YouTube: Cardholder

The cardholder is also central to disputes and post-transaction fraud outcomes. Many chargeback and reimbursement decisions turn on whether the cardholder authorized the transaction, whether the cardholder participated in or benefited from it, and whether the subsequent dispute is genuine or abusive. In cases of unauthorized card fraud, the cardholder is typically treated as the victim whose account or credentials have been misused. In first-party or friendly fraud scenarios, however, the cardholder may be the source of the deception, disputing a legitimate transaction for personal gain. This means the cardholder can occupy different roles in the financial crime framework: victim, customer, account owner, disputing party, or, in some cases, fraud actor.

The concept also matters in relation to account takeover and identity theft. A criminal may not need to steal the physical card if they can compromise the cardholder’s account, credentials, or personal data. Once that happens, the criminal may operate in a way that appears consistent with legitimate cardholder activity, especially in digital or remote payment environments. This creates a major control challenge for issuers, acquirers, merchants, and payment service providers, because they must distinguish genuine cardholder behavior from fraudulent use of valid cardholder data.

From a risk and controls perspective, understanding the cardholder means understanding expected behavior. Spending patterns, merchant types, geography, transaction timing, device usage, authentication history, and dispute behavior all help institutions assess whether activity is consistent with the legitimate cardholder profile. A transaction that looks ordinary in value may still be suspicious if it is inconsistent with the cardholder’s known behavior or follows recent account changes, unusual login activity, or newly added digital-wallet provisioning. For this reason, the cardholder is not just a static customer record. In a modern fraud framework, the cardholder is a behavioral and transactional profile that must be monitored continuously.

The cardholder concept is also important in corporate and commercial card environments. In those cases, the legal account may belong to a business, but the cardholder may be an employee or authorized user. This can complicate fraud analysis, authorization review, and misuse investigations because the distinction between business liability, individual use, and delegated authority becomes more significant. Card misuse in such settings may involve external fraud, internal abuse, policy breaches, or fraudulent disputes, all of which require a clear understanding of who the authorized cardholder is and what authority they were given.

Ultimately, the cardholder is a core concept in the financial crime environment because card-based controls, fraud decisions, and liability assessments depend on whether transactions can be linked to the rightful and authorized user of the card account. Whether the issue is unauthorized use, account takeover, chargeback abuse, card-not-present fraud, or internal misuse, the central question remains the same: was the transaction truly initiated or approved by the legitimate cardholder, and does the surrounding evidence support that conclusion? For that reason, the cardholder should be understood not merely as the person named on the card, but as the key reference point for attribution, authorization, and fraud risk across the card payments ecosystem.