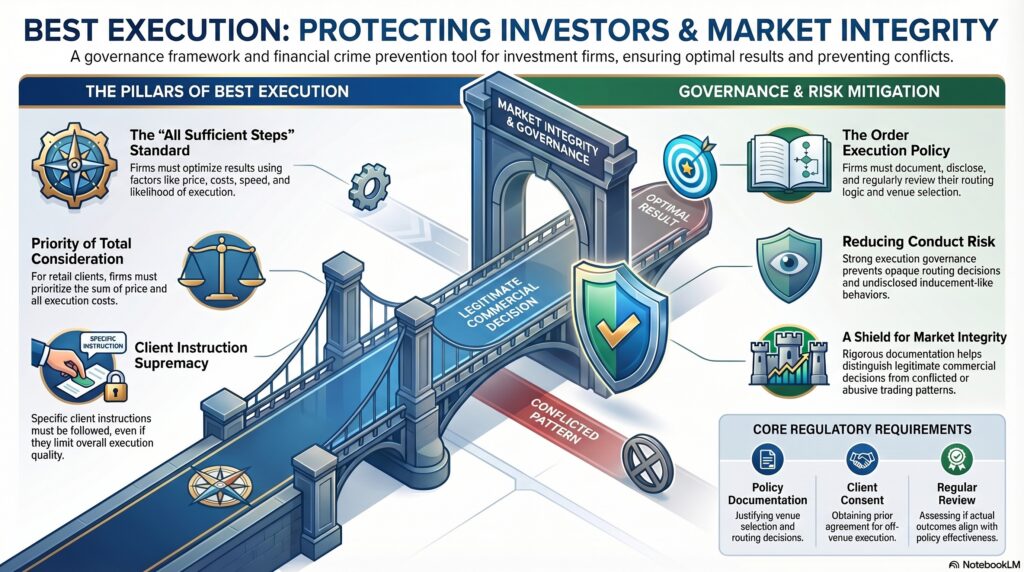

Best execution is the regulatory obligation requiring investment firms to take all sufficient steps to obtain the best possible result for clients when executing orders, taking into account factors such as price, costs, speed, likelihood of execution and settlement, size, nature, and any other relevant execution consideration. Under MiFID II Article 27 and the FCA’s COBS 11.2A, firms must also establish and implement an order execution policy, provide appropriate information to clients about that policy, and review their execution arrangements regularly.

In the financial crime environment, best execution is not primarily an AML control in the same way that customer due diligence or transaction monitoring is. Its core purpose is investor protection and market integrity. However, it remains highly relevant to the broader financial crime framework because weak execution governance can create conditions in which conflicts of interest, market abuse risk, opaque routing decisions, poor surveillance visibility, and misconduct become harder to detect or challenge. ESMA’s recent work on firms’ order execution policies notes supervisory findings that some firms did not sufficiently document venue-selection analysis or adequately demonstrate that they executed orders in line with best execution requirements.

From a professional compliance perspective, best execution is fundamentally about how a firm handles client orders when commercial incentives, market structure, and execution quality may pull in different directions. A firm may face choices among venues, brokers, liquidity providers, internalization arrangements, and execution methods. The best execution obligation is designed to ensure that those choices are made in the client’s interest rather than distorted by convenience, economics, or internal preference. That matters in the wider financial crime environment because governance failures in execution can overlap with conflicts of interest, poor conduct, undisclosed inducement-like behavior, and reduced transparency over how orders are routed and filled. This is an inference from the regulatory purpose and supervisory emphasis in the cited rules and reports.

A key feature of the regime is that best execution is not a single mechanical test. It is a framework for decision-making and control. MiFID II requires firms to take all sufficient steps, not simply to pursue the best price in every isolated circumstance. That means execution quality must be assessed across a range of factors, with different weighting depending on the client type, order characteristics, financial instrument, and available venues. For retail clients, the regulatory framework places particular weight on total consideration, meaning price plus costs. Firms must also follow a client’s specific instruction where one is given, though doing so may limit the firm’s ability to achieve the best possible result for the parts of the order covered by that instruction.

Watch on YouTube: Best Execution

In practical terms, best execution requires a firm to understand and document how it routes and executes orders, why it uses particular venues or counterparties, how it monitors execution quality, and when it needs to amend its execution arrangements. This is why the execution policy is such a central control document. It should not be a generic disclosure drafted once and left unchanged. It is supposed to explain clearly how the firm seeks best execution and to provide a basis for testing whether actual execution outcomes align with the policy. ESMA’s April 2025 final report specifically addresses the criteria for how firms should establish their order execution policies and assess their effectiveness, reflecting continuing supervisory concern about weak implementation.

Within the financial crime environment, the relevance of best execution becomes clearer when viewed through the lens of market integrity. If firms cannot explain why orders were routed a certain way, whether venue choices were justified, or whether execution quality was properly reviewed, then it becomes harder for compliance, surveillance, audit, and regulators to distinguish legitimate commercial decisions from conflicted or abusive ones. Poor execution governance can obscure whether clients were disadvantaged, whether routing decisions were influenced by improper incentives, or whether trading patterns deserve closer scrutiny. This is an inference supported by the supervisory focus on documented analysis, justified venue selection, and effective policy implementation.

There is also an important control relationship between best execution and order routing transparency. The FCA’s rules require firms to tell clients about their execution policy and to obtain prior consent to it. Where orders may be executed outside a trading venue, firms must inform clients of that possibility and obtain prior express consent. These obligations matter because opaque execution pathways can increase conduct and governance risk if clients do not understand how their orders are handled or where conflicts may arise. In the wider financial crime context, transparency over execution arrangements supports accountability and makes it easier to challenge patterns that may otherwise remain hidden within complex market structures.

A professionally mature best execution framework therefore depends on more than a dealing desk following market convention. It requires governance, monitoring, documented analysis, challenge, and periodic review. Firms should be able to evidence why particular execution venues are included in the policy, how execution quality is assessed, what data is used in that assessment, and how exceptions or weaknesses are escalated. ESMA’s 2024 consultation and 2025 final report show that regulators are still refining expectations in this area because actual practice has often fallen short of the formal standard.

For financial crime and compliance professionals, best execution is therefore best understood as part of the broader market-conduct control environment. It does not replace surveillance for insider dealing, market manipulation, or other abuse, but it supports the integrity of the execution process on which those wider controls depend. Where best execution is weak, firms may have poorer evidence, weaker oversight, and more room for conflicted or inappropriate order-handling decisions. Where it is strong, firms are better placed to demonstrate that client interests were protected and that execution choices were governed in a disciplined, reviewable way. This is an inference from the investor-protection purpose of MiFID II Article 27 and the supervisory findings highlighted by ESMA and the FCA.

Ultimately, best execution is a core market-conduct obligation that sits adjacent to the financial crime environment because it helps preserve fairness, transparency, and accountability in how client orders are executed. It requires firms to make execution decisions in the client’s interest, to document and disclose how those decisions are made, and to review whether their execution arrangements remain effective over time. In market environments where poor governance and opaque routing can weaken surveillance and heighten misconduct risk, best execution remains an important part of a credible compliance framework.