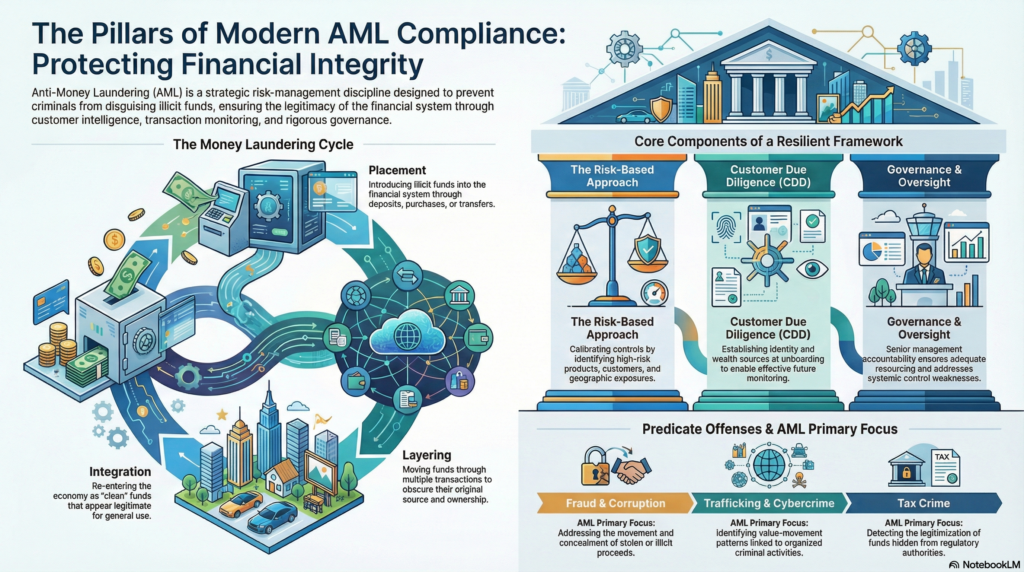

Anti-Money Laundering, commonly referred to as AML, is the framework of laws, controls, procedures, and operational measures designed to prevent criminals from disguising the origins of illicit funds and integrating them into the legitimate financial system. In the financial crime environment, AML is one of the central pillars of compliance because it addresses the movement, concealment, and legitimisation of proceeds derived from predicate offences such as fraud, corruption, drug trafficking, tax crime, cybercrime, human trafficking, and other serious criminal activity. AML is not simply a regulatory obligation. It is a core risk-management discipline intended to protect institutions from being used as vehicles for criminal finance.

At its foundation, AML is concerned with the classic laundering process of placement, layering, and integration. Placement involves introducing illicit funds into the financial system, often through deposits, purchases, transfers, or other entry points. Layering refers to the movement of those funds through multiple transactions or structures to obscure their origin and ownership. Integration occurs when the funds re-enter the economy appearing legitimate and available for use without obvious criminal connection. In practice, however, modern money laundering is rarely so linear. Criminals exploit complex corporate structures, digital payments, cross-border flows, trade-based mechanisms, shell entities, professional intermediaries, money mule networks, and increasingly fast-moving digital channels to move and disguise value. As a result, AML in a modern institution must be dynamic, intelligence-led, and closely integrated with broader financial crime controls.

In the financial crime environment, AML is inseparable from customer due diligence and risk-based control design. Institutions are expected to understand who their customers are, what their expected activity looks like, where their funds come from, and whether their behaviour aligns with the purpose and nature of the relationship. This is why AML begins well before suspicious transactions are detected. It starts at onboarding, where firms assess customer identity, beneficial ownership, source of funds, source of wealth where appropriate, geographic exposure, product risk, and the broader risk profile of the relationship. If these elements are weak or superficial, the institution’s ability to detect laundering later in the customer lifecycle is materially reduced.

A strong AML framework relies on several interdependent components. Customer due diligence establishes the identity and risk profile of the customer. Enhanced due diligence applies deeper scrutiny where the risks are higher, such as with politically exposed persons, high-risk jurisdictions, complex ownership structures, correspondent relationships, or unusual business models. Transaction monitoring is then used to identify activity inconsistent with the customer profile or suggestive of laundering typologies. Sanctions screening, name screening, adverse media review, case investigation, escalation procedures, suspicious activity reporting, staff training, governance oversight, and recordkeeping all support the wider framework. AML is therefore not a single control or a single team’s responsibility. It is an operating model that depends on consistency across front-line teams, compliance functions, investigative units, and senior management.

Watch on YouTube: Anti Money Laundering (AML)

One of the most important professional principles in AML is the risk-based approach. Institutions cannot apply the same level of scrutiny to every customer, transaction, or jurisdiction in exactly the same way. Instead, they are expected to identify where the risk is higher and calibrate controls accordingly. This includes understanding which products are more vulnerable to abuse, which customer types may present heightened laundering risk, which geographies raise concern, and which transactional behaviours require closer review. A well-functioning AML programme therefore depends on the quality of the institution’s financial crime risk assessment. If the institution does not understand its own risk exposure, its monitoring thresholds, due diligence standards, escalation pathways, and governance decisions are unlikely to be proportionate or defensible.

AML also has a strong relationship with fraud and other financial crime typologies. In practice, the proceeds of fraud are often laundered through accounts, businesses, payment instruments, or intermediaries that appear legitimate. This means the distinction between fraud prevention and AML is often operational rather than substantive. Fraud may generate the criminal proceeds, while money laundering enables those proceeds to be moved, disguised, and ultimately enjoyed. In many institutions, this overlap means AML teams must understand payment fraud, account takeover, mule activity, sanctions evasion, trade manipulation, and shell-company abuse as part of the same wider ecosystem of financial crime. A narrow approach that treats AML only as suspicious transaction reporting can miss these interconnected risks.

The investigative element of AML is especially important. Transaction monitoring alerts, customer escalations, adverse media findings, law enforcement enquiries, or internal referrals often require structured case review to determine whether behaviour is suspicious, explainable, or indicative of criminal activity. These investigations require more than checking whether a transaction exceeded a threshold. They involve analysing patterns, customer history, linked counterparties, account purpose, supporting documentation, and any inconsistencies between expected and actual behaviour. The quality of this investigative judgement is a key measure of AML effectiveness. Poor-quality review can lead either to under-reporting of suspicious behaviour or to excessive defensive escalation that overwhelms the institution’s own processes and weakens the value of its reporting.

Governance sits at the centre of AML effectiveness. Senior management and boards are expected to understand the institution’s exposure to money laundering risk and to ensure that adequate systems and controls are in place. This includes approving risk appetite, overseeing remediation, reviewing management information, ensuring sufficient resourcing, and maintaining accountability for the performance of the AML framework. Internal audit, independent testing, quality assurance, and regulatory engagement all play important roles in determining whether the programme is operating as intended. AML failure is often not simply a technical deficiency in transaction monitoring or screening. It is frequently a governance failure in which known control weaknesses, poor data quality, understaffing, fragmented ownership, or weak challenge are allowed to persist.

Technology plays a growing role in AML, but it does not remove the need for professional judgement. Screening systems, transaction monitoring models, network analytics, case management tools, and data integration capabilities can materially strengthen detection and efficiency. However, poorly calibrated systems can generate excessive false positives, miss relevant activity, or give management a misleading sense of assurance. Effective AML requires institutions to understand the limitations of their systems, validate model outputs, investigate unusual patterns thoughtfully, and ensure that technology supports rather than replaces sound compliance judgment. In modern financial crime environments, where speed, complexity, and data volumes are increasing, the challenge is not simply to automate more, but to automate intelligently.

AML also has a broader reputational and societal dimension. Institutions that fail to control money laundering risk may facilitate corruption, organized crime, terrorism financing, sanctions evasion, human exploitation, and other serious harms. In that sense, AML is not only about avoiding enforcement action or financial penalties. It is about preventing the institution from becoming part of a criminal infrastructure. A credible AML programme therefore protects not only the firm itself, but also the integrity of the wider financial system.

Ultimately, Anti-Money Laundering is a core discipline within the financial crime environment because it addresses the mechanisms through which criminal proceeds are concealed, moved, and legitimised. It requires institutions to understand their customers, assess risk intelligently, monitor activity effectively, investigate suspicious behaviour thoroughly, and maintain governance strong enough to support consistent control execution. In a financial system shaped by increasingly sophisticated criminals, rapid digital payments, global connectivity, and evolving regulatory expectations, AML cannot be treated as a narrow compliance requirement. It must be understood as a strategic control framework that underpins the credibility, resilience, and integrity of the institution as a whole.