Money mule schemes are a core financial crime typology in which individuals, knowingly or unknowingly, receive and move criminal proceeds through their accounts on behalf of others. Law enforcement bodies describe money muling as a form of money laundering because it helps criminals distance themselves from the original offence and obscure the trail of funds. Europol states that money muling is a type of money laundering, and the FBI similarly explains that money mules move illegally acquired money for someone else.

In the financial crime environment, the significance of money mule schemes lies in their function as an enabling mechanism rather than an isolated offence. Mule accounts are often used to receive the proceeds of fraud, scams, cybercrime, trafficking, or other predicate offences, and then to transfer those funds onward through domestic or cross-border payment routes. The Home Office’s UK action plan states that money muling allows criminal gangs, including fraudsters and traffickers, to profit from crime, while Garda guidance describes mules as people who transfer illegally obtained money between accounts, often across borders, for others.

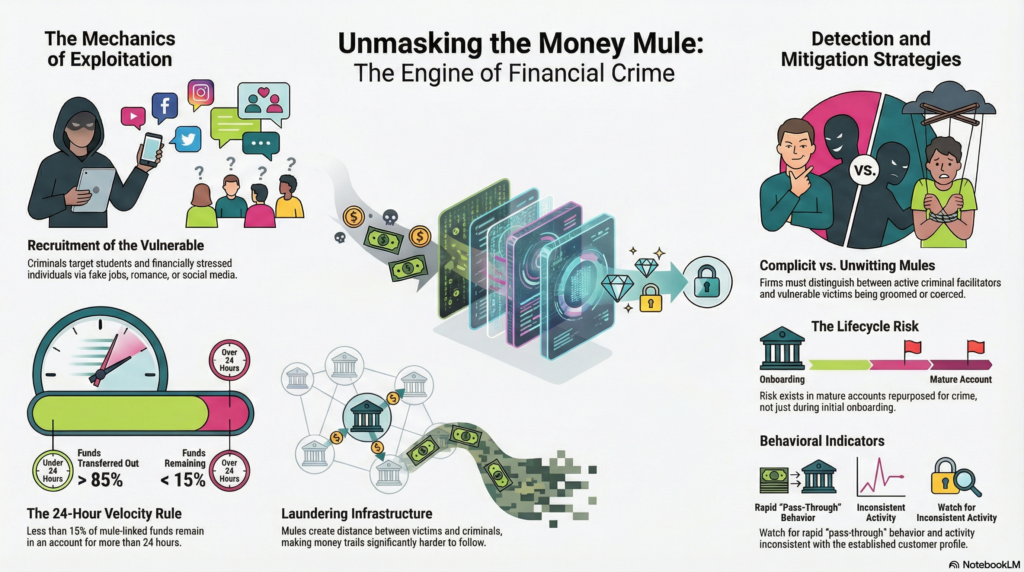

From a professional financial crime perspective, money mule activity is especially important because it sits directly between predicate crime and the apparent legitimisation of funds. Fraud may generate the proceeds, but mule accounts help criminals move those proceeds quickly, fragment ownership, complicate tracing, and reduce the chance that investigators can connect the receiving account to the true controller of the scheme. Europol notes that money mules create distance between victims and criminals, making money trails harder to follow. That means mule activity is not merely a downstream operational issue; it is a structural part of how organized fraud and laundering ecosystems function.

A defining feature of money mule schemes is that the account holder may not always be a fully complicit criminal actor. Official guidance distinguishes between complicit, witting, and unwitting mules. Europol’s educational material notes that some mules are recruited through fake job offers, romance approaches, social media contact, or apparently legitimate business opportunities, while other individuals knowingly ignore warning signs or actively participate for payment. This distinction matters because firms must balance disruption with safeguarding: some account holders are active facilitators, while others are vulnerable people being exploited by criminal networks.

Watch on YouTube: Money Mule Schemes

Recruitment dynamics are therefore central to understanding mule schemes. Young people, students, migrants, financially stressed individuals, and victims of coercion or grooming are often targeted because they may be more susceptible to “easy money” offers or less aware of the legal and financial consequences. The Home Office action plan frames money muling as a public-protection issue as well as a crime threat, emphasizing the need for both deterrence and safeguarding. In practical terms, this means institutions should not treat every mule case as a simple account-closure decision. Some cases may call for enhanced customer engagement, vulnerability assessment, and information-sharing responses in addition to traditional fraud and AML action.

Operationally, mule schemes are dangerous because of the speed at which funds move. UK Finance has highlighted that mule-linked funds can pass through accounts extremely quickly, citing research that less than 15% of funds linked to money mules remain in an account for more than 24 hours. This speed compresses the window for intervention and means that delayed detection materially reduces the chance of recovery, traceability, and effective disruption. In real-time and faster-payment environments, the problem becomes more acute because institutions often have minutes, not days, to identify whether inbound funds are being received into a laundering conduit rather than a legitimate customer account.

The financial crime implications extend far beyond the receiving account itself. A mule account may be used to collect fraud proceeds from multiple victims, route funds through layered transfer chains, convert proceeds into cash, cryptoassets, or foreign transfers, or distribute value across networks of linked accounts. For this reason, mule activity often overlaps with authorized push payment scams, account takeover, synthetic identity abuse, application fraud, and organized payment fraud. The account holder may appear to be a normal retail customer, but the transaction pattern can reflect networked criminal orchestration rather than personal banking behaviour. This is an inference drawn from the way official sources describe mule activity as a laundering mechanism for fraud and other serious crime.

One of the most difficult control challenges is that mule accounts are not always newly opened accounts. The FCA has emphasized both the prevention and detection of money mule accounts and, more recently, the role of National Fraud Database and other detection tools in identifying mule misuse. UK Finance has also noted growing concern around mule risk in existing accounts, not only newly onboarded ones. This is important because institutions that focus too narrowly on onboarding may miss mature customer accounts that have been repurposed, compromised, or recruited into criminal flows after a period of ordinary use.

A professionally mature approach therefore treats money mule risk as a lifecycle issue. At onboarding, firms need to assess whether the applicant profile, product choice, expected activity, and account purpose are credible. During the life of the relationship, they need to monitor for indicators such as rapid pass-through behaviour, incoming credits followed by immediate onward transfers, repeated receipt of funds from unrelated parties, activity inconsistent with the customer profile, unusual use of cash withdrawals, concentration of counterparties, frequent international transfers, or links to known fraud patterns. FCA findings on firms’ systems and controls against mule activity underscore the importance of proportionate but effective management of mule-account risk.

Governance and intelligence-sharing are equally important. The UK’s money mule action plan was explicitly framed as a cross-sector response, reflecting the reality that no single institution can address mule activity in isolation. Financial institutions, law enforcement, regulators, educational bodies, and technology platforms all have roles in disrupting recruitment, sharing typologies, flagging suspected accounts, and protecting vulnerable people. This broader model matters because mule networks often span multiple banks, payment providers, digital platforms, and jurisdictions. A firm that looks only at its own narrow account activity may see fragments of the pattern but not the network as a whole.

The consequences for individuals involved are also severe. Garda guidance warns that a money mule may face frozen accounts, difficulty accessing banking services, and criminal investigation. Europol’s educational materials similarly stress that acting as a mule is not harmless and can have serious legal and financial consequences. From a financial crime management standpoint, this matters because many recruits underestimate the seriousness of their conduct. Effective frameworks therefore combine enforcement with education, prevention messaging, and vulnerability-aware intervention.

In institutional terms, mule schemes expose weaknesses across fraud, AML, customer risk-rating, transaction monitoring, and operational response. If an institution identifies only the suspicious payment but not the role of the receiving account, it may stop a transaction without disrupting the mule infrastructure that enables repeated crime. Conversely, if it focuses only on the account holder without understanding the upstream fraud or downstream laundering chain, it may miss the wider criminal network. The strongest controls therefore connect inbound fraud intelligence, behavioural account monitoring, customer due diligence, case investigation, and where appropriate suspicious activity escalation. This is an inference from the official emphasis on mule activity as both fraud facilitation and money laundering.

Ultimately, money mule schemes are a central financial crime threat because they turn ordinary bank and payment accounts into laundering infrastructure. They allow criminals to separate themselves from stolen funds, exploit vulnerable or complicit intermediaries, and move proceeds rapidly through the financial system before detection and recovery can occur. In a modern payment environment shaped by instant transfers, digital recruitment, and organized fraud networks, mule activity cannot be treated as a peripheral issue. It should be recognized as a core component of the financial crime ecosystem, requiring integrated controls, faster detection, stronger intelligence-sharing, and a response model that combines disruption with safeguarding where exploitation is present.