Application fraud is a significant financial crime typology in which a person seeks to obtain a product, service, account, or financial facility by providing false, misleading, manipulated, or incomplete information during the application process. In the financial crime environment, this can involve the use of stolen identities, synthetic identities, falsified documents, misrepresented income or employment details, hidden beneficial ownership, or deception regarding the intended use of the product. Although application fraud is often associated with onboarding and account opening, its true significance is much broader. It is a method of gaining entry into the financial system under false pretences, and once successful, it can create exposure across fraud, money laundering, sanctions, credit risk, and wider control failure.

From a professional risk perspective, application fraud is best understood as an attack on the integrity of customer acceptance. Financial institutions rely on the application stage to assess who the customer is, what risk they present, whether the relationship is permissible, and what level of controls should apply. If that assessment is undermined by deception, the institution may onboard a customer, extend a facility, or provide access to payment infrastructure on a fundamentally false basis. This makes application fraud more than a discrete onboarding issue. It is a gateway typology that can compromise the reliability of the entire customer lifecycle, because every downstream control may depend on assumptions established at the point of entry.

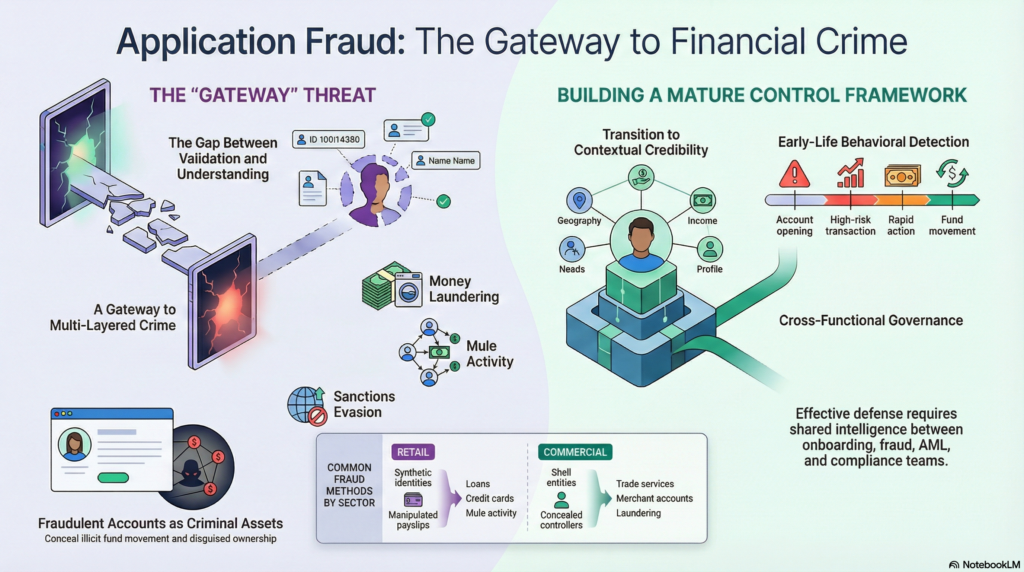

The methods used in application fraud vary according to the product and criminal objective. In retail and consumer settings, it may involve false personal information, manipulated payslips, fabricated employment details, or the use of another person’s identity to obtain loans, credit cards, overdrafts, or accounts. In business and commercial contexts, the fraud may involve shell entities, falsified ownership structures, concealed controllers, misrepresented business activity, or inaccurate financial information provided to obtain banking facilities, merchant accounts, trade services, or lending products. In some cases, the deception is intended to obtain credit that will never be repaid. In others, the objective is not credit abuse at all, but access to accounts and services that can later be used for mule activity, transaction laundering, sanctions evasion, or the movement of illicit funds.

This wider purpose is what makes application fraud especially relevant in the financial crime environment. A fraudulently obtained account or facility is not merely a source of direct loss; it can become a criminal asset. Once opened, the relationship may be used to receive the proceeds of scams, process suspicious transactions, move funds across jurisdictions, disguise beneficial ownership, support fake merchant activity, or create the appearance of legitimacy for transactions that might otherwise be questioned. A customer onboarded through deception may also be more difficult to assess using normal monitoring approaches, because the baseline profile against which activity is measured is itself unreliable. In practical terms, application fraud can therefore function as both an entry mechanism and an enabler of wider criminal misuse.

Watch on YouTube: Application Fraud

One of the defining challenges of application fraud is that it often appears credible at first sight. The information submitted may be internally consistent, documents may look authentic, and the application may fit the general profile of a normal customer or business. In digital and remote onboarding environments, where institutions increasingly rely on uploaded documents, database checks, device information, and automated decisioning, the criminal may need only to satisfy a threshold of plausibility rather than prove authenticity in a deeper sense. This means application fraud often succeeds not because controls are absent, but because they are too fragmented, too static, or too heavily focused on verifying individual data points rather than assessing the overall coherence and credibility of the application.

In professional terms, application fraud frequently exploits the gap between validation and understanding. An address may exist, a phone number may function, a business registration may be real, and an identity document may pass basic format checks. Yet the wider application may still be deceptive in substance. The criminal advantage lies in assembling enough credible-looking material to satisfy minimum acceptance criteria while concealing the underlying falsehood. This is particularly dangerous where firms rely on automated onboarding journeys with limited human challenge, because the application can progress smoothly through a series of isolated checks without any one control assessing whether the full profile makes commercial or behavioural sense.

The typology also overlaps significantly with identity-related risk. Application fraud may involve direct identity theft, where a real person’s details are used without consent, or synthetic identity abuse, where genuine and fictitious elements are combined to create a new customer profile. In some cases, the applicant is a real individual misrepresenting material facts such as income, source of funds, criminal background, or intended use of the account. In others, the application is submitted by a criminal intermediary, fraud ring, or complicit third party. These variations matter because they affect both the institution’s control response and the broader financial crime implications. What appears initially as a simple false statement may in fact be part of organized fraud, mule recruitment, or a wider laundering scheme.

Application fraud is especially important in relation to products that create immediate transactional capability or deferred financial exposure. Current accounts, cards, digital wallets, merchant accounts, business banking facilities, consumer lending, and short-term credit products can all be attractive targets because they provide either access to value or infrastructure through which value can move. Criminals may use a fraudulently obtained account to establish legitimacy, build history, and then exploit it later for more serious abuse. Alternatively, they may seek rapid value extraction through lending, credit drawdown, or receipt of illicit transfers. The initial application therefore needs to be viewed not just as a point of acceptance, but as the first stage in a potential criminal lifecycle.

A mature control framework for application fraud requires a combination of prevention, detection, investigation, and governance. Prevention begins with strong onboarding design, including robust identity verification, document validation, corroboration of key data points, beneficial ownership assessment where relevant, and appropriately risk-based challenge of information that appears unusual, incomplete, or inconsistent. However, the most effective institutions go beyond checking whether details can be validated. They assess whether the application is contextually credible. Does the stated employment align with the applicant’s profile? Does the business activity align with the geography, products, and ownership structure? Does the requested product make sense given the customer’s apparent needs and circumstances? These higher-order questions are often where application fraud becomes visible.

Detection after onboarding is equally important because not all fraudulent applications will be identified at the point of submission. Some will only become apparent through early-life account behaviour, such as immediate high-risk transactions, rapid inbound and outbound fund movement, unusual digital channel use, dormant-to-active transitions, inconsistent contact behaviour, suspicious merchant activity, or defaults inconsistent with the original application profile. Early warning indicators are critical because application fraud often reveals itself once the criminal begins using the product in ways that expose the true intent behind the relationship. This means onboarding teams, fraud functions, AML monitoring teams, and customer-service operations all need mechanisms for sharing concerns and identifying patterns that may point back to a deceptive application.

The investigative dimension is also significant. When suspected application fraud is identified, the institution needs to determine not only whether the original application was dishonest, but what that dishonesty was intended to achieve. Was the purpose to obtain credit, to create a mule account, to conceal beneficial ownership, to gain merchant access, or to support a broader network of criminal activity? This requires a review of linked accounts, shared addresses, device overlaps, contact-point reuse, transaction behaviour, identity associations, and any connections to known typologies. A weak investigation may resolve the immediate customer relationship but miss the wider network risk. A stronger investigation treats the application as a possible intelligence source for understanding broader financial crime exposure.

Governance is essential because application fraud often sits across multiple control functions. It should be reflected in fraud risk assessments, customer acceptance frameworks, AML and sanctions onboarding controls, product approval processes, model governance, and management reporting. Institutions should understand which channels, products, geographies, and customer types are most exposed, and whether their acceptance processes are calibrated to the threats they actually face. Useful metrics may include fraud rejection rates, post-onboarding exits for misrepresentation, early-life suspicious activity, document-fraud trends, linked-application clusters, default patterns associated with false applications, and the proportion of fraudulent cases identified only after account opening. These measures help determine whether application controls are genuinely effective or merely creating an appearance of assurance.

There is also a customer and reputational dimension, particularly where application fraud involves stolen identities or innocent parties whose details have been misused. Poor detection can expose victims to credit harm, account disruption, and lengthy remediation. Overly aggressive controls, on the other hand, can unfairly impede genuine customers and create exclusion risk. A professionally mature response therefore requires balance: controls should be rigorous enough to identify deception, but proportionate enough to avoid unnecessary friction or poor outcomes for legitimate applicants. This is especially important in digital-first environments, where onboarding experience has commercial importance but weak acceptance standards can have long-lasting financial crime consequences.

Ultimately, application fraud is a core financial crime threat because it allows criminals to enter the financial system by corrupting the acceptance process itself. It undermines the institution’s ability to assess identity, ownership, legitimacy, and risk at the moment when those judgments matter most. Once successful, it can enable fraud, credit abuse, mule activity, transaction laundering, sanctions exposure, and the movement of illicit funds through relationships that appear legitimate on paper. In a modern financial services environment, strong application fraud controls are not simply a front-end fraud measure; they are a foundational component of a credible financial crime framework. For that reason, application fraud should be treated as a strategic control risk requiring integrated onboarding standards, dynamic monitoring, strong investigative capability, and close coordination across fraud, AML, compliance, operations, and governance functions.