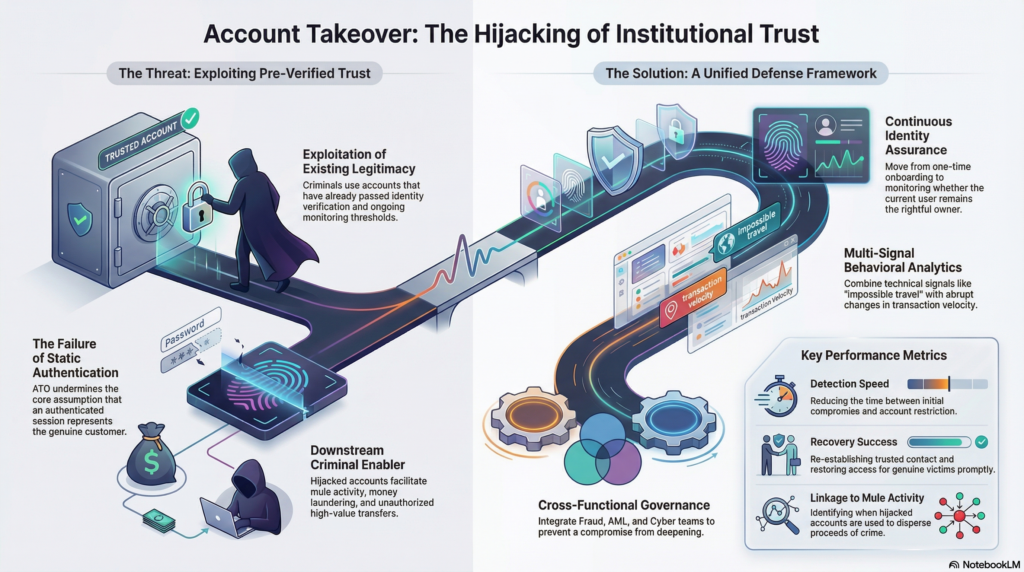

Account takeover is a serious financial crime typology in which a criminal gains unauthorized control of a legitimate customer account and then uses that access to commit fraud, move funds, obtain sensitive information, or facilitate wider criminal activity. In the financial crime environment, the significance of account takeover lies in the fact that the offender is not creating a false relationship from the outset, but exploiting an existing one that has already passed customer onboarding, identity verification, and, in many cases, ongoing monitoring thresholds. That gives the criminal a level of apparent legitimacy which can make the activity harder to detect and more operationally damaging than many other forms of fraud.

From a control perspective, account takeover is particularly disruptive because it undermines one of the core assumptions within financial services: that an authenticated customer session represents the genuine customer. Once that assumption fails, a wide range of downstream controls can be weakened. Transactions may appear to originate from a trusted account, profile changes may seem customer initiated, and behaviour that would ordinarily be suspicious can initially be masked by the history and standing of the genuine relationship. This is why account takeover should not be viewed only as a cyber incident or a customer service issue. It is a financial crime risk that sits across fraud prevention, anti-money laundering, identity assurance, cyber security, and operational risk management.

The methods used to carry out account takeover are varied and increasingly sophisticated. Criminals may obtain credentials through phishing, malware, credential stuffing, social engineering, SIM swap attacks, data breaches, or the manipulation of password-reset and account recovery processes. In many cases, the account is not compromised by defeating a single control, but by exploiting small weaknesses across several stages of the customer journey. A customer may be deceived into revealing login details, a device may be infected, a one-time passcode may be intercepted, or a call centre process may be manipulated using stolen personal information. The result is the same: the criminal inserts themselves into a legitimate account environment and begins to operate as though they were the customer.

In the financial crime environment, the consequences extend well beyond unauthorized access. A compromised account can be used to transfer funds to mule accounts, make card-not-present purchases, access stored value, redeem loyalty or rewards balances, apply for additional products, change contact details, or obtain further personal information for future fraud. In some cases, the account becomes a temporary vehicle for laundering proceeds of crime, particularly where stolen funds are moved rapidly through apparently legitimate customer infrastructure before being dispersed onward. This is what makes account takeover especially important for financial crime professionals: it is not only a loss event, but a potential enabler of broader criminal networks and downstream illicit flows.

Watch on YouTube: Account Takeover (ATO)

One of the most challenging aspects of account takeover is that it exploits trust already embedded in the institution’s systems and processes. Traditional customer due diligence is designed to establish who the customer is at onboarding. Account takeover tests something different: whether the person interacting with the account today is still the rightful user, and whether the behaviour remains consistent with the true customer’s profile. That distinction is critical. A firm may have strong onboarding controls and still be highly exposed to account takeover if authentication, account recovery, device trust, and behavioural detection are weak. In that sense, account takeover represents a failure of ongoing identity assurance rather than initial identification alone.

This risk is heightened in digital and remote-service environments, where customer interactions are increasingly conducted without face-to-face contact. As firms expand mobile banking, digital wallets, instant payments, and self-service functionality, they also create more opportunities for criminals to exploit remote channels at speed and scale. The same convenience features that improve customer experience can increase vulnerability if they are not supported by strong verification controls, layered authentication, and effective anomaly detection. Fast payments, instant profile changes, frictionless login journeys, and automated servicing processes may each be commercially attractive, but they also reduce the time available to identify and interrupt criminal behaviour once an account has been compromised.

A mature financial crime framework therefore treats account takeover as a lifecycle risk rather than a single-event fraud scenario. Prevention begins with robust authentication architecture, strong enrollment and recovery processes, careful management of device trust, and enhanced verification for high-risk actions such as changes to phone numbers, email addresses, passwords, payees, or linked accounts. However, prevention alone is not sufficient. Even strong front-end controls can be bypassed, particularly where the criminal has access to the customer’s device, credentials, or communication channels. Detection capability is therefore equally important. Institutions need to identify behavioural anomalies that suggest the person controlling the account is no longer the legitimate user, even where login credentials appear valid.

This requires a combination of technical and operational controls. Behavioural analytics, session monitoring, device intelligence, transaction analysis, and velocity checks all have a role to play. Indicators may include unusual login patterns, new devices, impossible travel signals, abrupt changes in transaction behaviour, rapid amendments to contact details, newly created beneficiaries followed by immediate outbound payments, or activity inconsistent with the customer’s known profile. These signals become more effective when they are assessed in combination rather than isolation. A single anomalous login may not justify intervention, but a suspicious login followed by a password reset, a change of mobile number, and a high-value transfer to a new payee presents a very different risk picture.

Operational response is just as important as technical detection. Once account takeover is suspected, firms need clear and well-rehearsed procedures for restricting access, stopping suspicious payments, validating recent changes, re-establishing trusted contact with the legitimate customer, and investigating linked activity. In many cases, the response must be cross-functional. Fraud teams may focus on preventing immediate loss, cyber teams may assess compromise vectors, AML teams may evaluate whether the account has been used to move illicit funds, and operations or customer service teams may be responsible for customer remediation and account restoration. Weak coordination between these functions can allow a compromise to deepen, especially where one team treats the incident as isolated fraud while another has not yet considered the wider financial crime implications.

Governance is another critical dimension. Account takeover should be explicitly recognized in fraud risk assessments, financial crime typologies, control testing programmes, and management reporting. Firms should understand which products, channels, customer segments, and servicing journeys are most exposed, and whether their current controls are calibrated to the actual threat. Metrics such as takeover attempts, confirmed compromises, loss values, detection speed, false-positive rates, recovery success, and links to mule activity can help determine whether the control environment is effective or overly reliant on reactive intervention. A high volume of profile-change fraud, for example, may indicate weaknesses in account recovery or change-of-details verification rather than a purely transactional problem.

There is also an important customer treatment dimension. Because account takeover affects genuine customers, firms must respond in a way that protects the institution without compounding harm to the victim. Delayed recognition, poor communication, or failure to restore access promptly can create significant financial and reputational damage. Equally, overly rigid controls that repeatedly block legitimate users can undermine trust and create operational burden. The most effective firms therefore balance security with usability, ensuring that high-risk actions are subject to greater scrutiny while routine customer activity remains proportionate and manageable. In professional terms, account takeover management is as much about calibrated control design as it is about fraud prevention.

From a wider financial crime perspective, account takeover also highlights the growing convergence of fraud, cybercrime, and money laundering risk. A compromised account may begin as a customer authentication failure, but it can quickly become a vehicle for unauthorized payments, data theft, identity misuse, and the onward movement of criminal proceeds. That convergence means firms should avoid managing account takeover in a narrow silo. When viewed only as an online banking fraud problem, important warning signs may be missed. When treated as part of the broader financial crime ecosystem, it becomes easier to see how customer compromise, mule account usage, suspicious payment flows, and control evasion fit together.

Ultimately, account takeover is a major financial crime threat because it turns legitimate customer infrastructure into a criminal asset. It allows offenders to exploit trust, bypass elements of the control environment, and conduct suspicious activity through accounts that initially appear genuine. In a modern financial services environment, it is no longer enough to verify identity at onboarding and rely on static credentials thereafter. Firms must be able to assess continuously whether the person controlling the account is the true customer and whether the activity remains consistent with legitimate ownership. For that reason, account takeover should be treated as a core financial crime risk requiring integrated controls, strong governance, dynamic detection, and close coordination across fraud, AML, cyber, operations, and customer service functions.