Check fraud is a financial crime typology involving the fraudulent creation, alteration, negotiation, interception, or misuse of checks in order to obtain funds, redirect payments, or exploit weaknesses in deposit and clearing processes. Although checks are an older payment instrument, law enforcement and regulators continue to treat check fraud as a significant modern threat. The FBI and U.S. Postal Inspection Service warned in January 2025 that check fraud is rising and that a significant share is enabled by mail theft, while the U.S. Postal Inspection Service continues to highlight counterfeit checks, altered checks, and check-deposit scams as active risks.

In the financial crime environment, check fraud is important because it combines features of payment fraud, identity misuse, document fraud, mule activity, and money laundering. A fraudulent check can be used to extract funds directly, but it can also serve as the first step in a broader criminal chain. Criminals may steal checks from the mail, alter payee or amount information, produce counterfeit items using stolen account data, deposit fraudulent instruments into mule accounts, or induce victims to deposit fake checks and forward part of the proceeds before the instrument is returned unpaid. The Postal Inspection Service specifically warns about scams in which victims are told to deposit checks and send money onward, which is why check fraud often overlaps with money mule schemes and wider laundering risk.

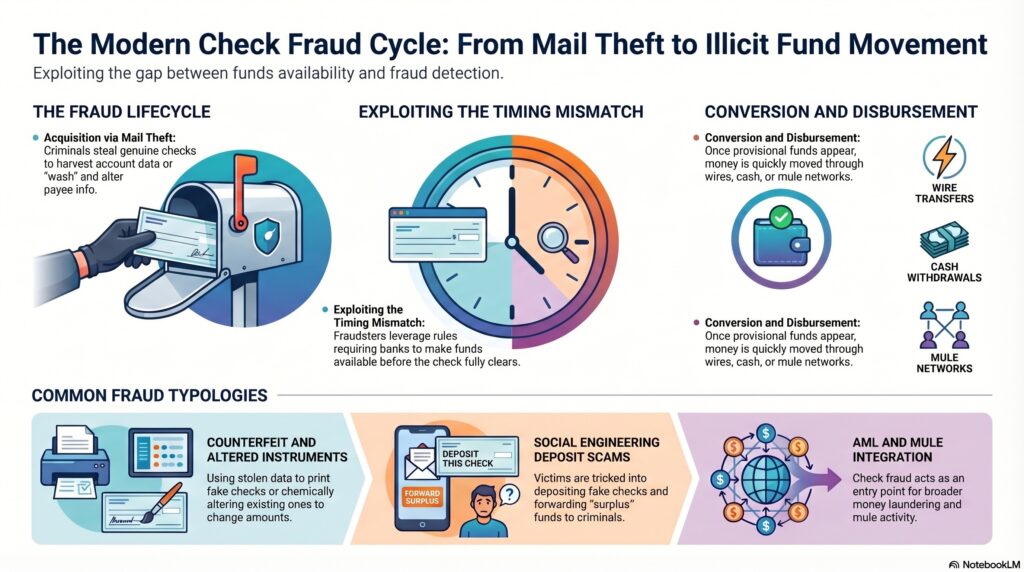

A major reason check fraud remains operationally significant is the timing mismatch between funds availability and fraud detection. The FBI and USPIS note that fraudsters exploit rules requiring financial institutions to make deposited check funds available within relatively short timeframes, which can be too short for the customer or institution to detect and stop the fraud before money is withdrawn or transferred onward. This makes check fraud especially damaging because the loss often crystallizes before the institution has fully confirmed whether the item is genuine, altered, or payable. In practical terms, the check-clearing process can create a window in which criminals convert a fraudulent instrument into spendable or transferable funds.

Watch on YouTube: Check Fraud

From a professional financial crime perspective, check fraud is not just a document-integrity problem. It is a control-integrity problem. A legitimate check carries account information, routing details, signature expectations, and apparent payment authority. Once stolen or copied, those features can be repurposed to create altered or counterfeit items that appear plausible enough to move through deposit and clearing channels. Mail theft has become particularly important in this area because it gives criminals access to genuine checks that can be chemically washed, altered, copied, or used to harvest account information for additional fraud attempts. The FBI and USPIS expressly tied the current rise in check fraud to mail theft.

The typology also intersects directly with fraud and AML obligations. A deposited fraudulent check may not be the endpoint of the crime. Once provisional funds are made available, those funds may be withdrawn in cash, wired onward, moved to other accounts, or dispersed through mule networks. This means a financial institution confronting check fraud may also be seeing suspicious fund movement rather than only a payment dispute or counterfeit item issue. The FFIEC BSA/AML Manual emphasizes that banks should report suspected fraud and related suspicious activity through SAR processes, which is relevant because check fraud often generates exactly the sort of suspicious transactional behavior that merits escalation beyond routine item return handling.

There are several common forms of check fraud. These include counterfeit checks created from stolen or fabricated account data, altered checks where payee or amount details are changed, forged endorsements, duplicate deposits, and deposit scams involving fake cashier’s checks, business checks, or money orders. The Postal Inspection Service’s current public guidance specifically highlights counterfeit-check scams and the misuse of blank check stock, printers, and scanners to create fraudulent instruments. In modern practice, this means check fraud often blends traditional paper-instrument abuse with digital facilitation, social engineering, and fast movement of funds after deposit.

For financial institutions, effective control requires more than rejecting bad items after loss has occurred. A mature framework includes deposit risk controls, exception handling, hold decisions where appropriate, customer and account profiling, monitoring for unusual deposit-and-withdrawal patterns, and escalation where check activity appears inconsistent with the account purpose or customer profile. The FBI and USPIS warning underscores the need for rapid recognition because the fraud window is compressed by funds-availability rules, and recent Federal Reserve and state-regulator requests for information also identify check fraud as a significant current payments-fraud issue.

Customer behavior is also central to this typology. Many check fraud schemes depend on victims not understanding that funds shown as “available” are not the same as final confirmation that a check is legitimate. Fraudsters exploit that misunderstanding by persuading people to deposit a check and quickly send money back, purchase goods, or transfer funds onward. The Postal Inspection Service’s fraud guidance directly addresses this mechanism. In the financial crime environment, this means check fraud prevention is partly a matter of customer protection and communication, not just back-office processing.

Ultimately, check fraud remains a serious financial crime threat because it weaponises a familiar payment instrument that many people and businesses still trust. It exploits weaknesses in mail security, instrument integrity, deposit timing, and customer understanding to generate fraudulent value and move suspicious funds before the fraud is fully recognized. Even in a digital payments era, check fraud is not a legacy nuisance. It is an active typology that requires integrated controls across fraud operations, deposit risk, customer education, investigations, and AML escalation.