A wire transfer is an electronic transfer of funds sent through a funds transfer system from an originator to a beneficiary. Under the U.S. BSA/AML framework, a funds transfer is the series of transactions beginning with the originator’s payment order and ending when the beneficiary’s bank accepts a payment order for the benefit of the beneficiary. FATF guidance similarly says a wire transfer is any transaction carried out on behalf of an originator through a financial institution by electronic means to make funds available to a beneficiary at another financial institution.

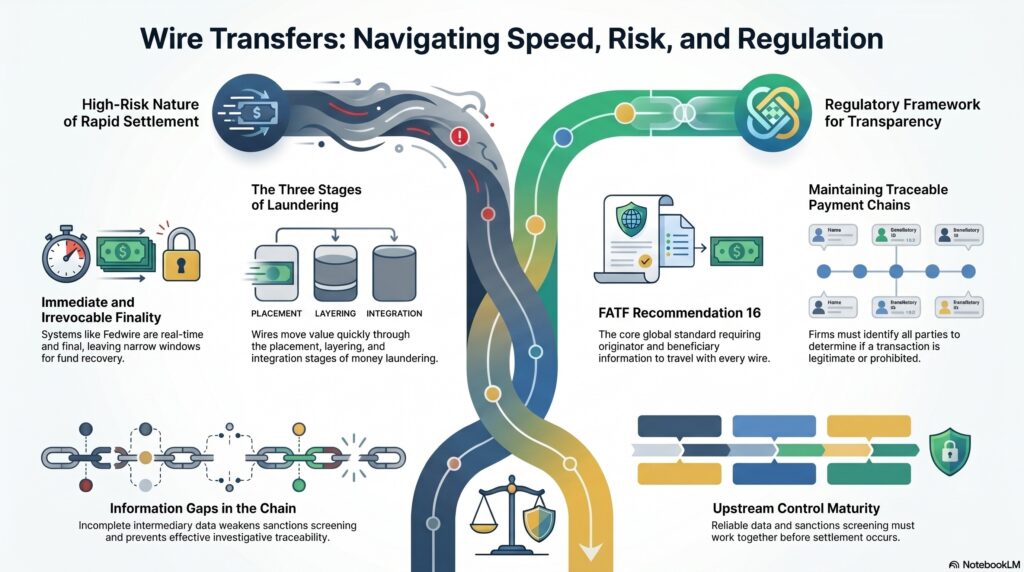

In the financial crime environment, wire transfers matter because they are one of the most important mechanisms for moving value quickly across institutions, jurisdictions, and payment chains. They are central to legitimate commerce and treasury activity, but they can also be used in the placement, layering, and integration stages of money laundering. The FFIEC states this directly and notes that funds transfer systems can present an attractive method to disguise the source of funds derived from illegal activity.

From a professional perspective, the key feature of a wire transfer is not just speed, but traceable payment-chain information. FATF Recommendation 16 is built around this point: wire transfers should carry originator and beneficiary information so firms and authorities can identify who is sending and receiving funds and assess whether the transaction is legitimate, suspicious, or prohibited. FATF updated Recommendation 16 in June 2025 to reflect modern payment-domain changes and evolving risks, reinforcing that payment transparency remains a live control issue.

Watch on YouTube: Wire Transfer

This is why wire transfers are closely linked to AML, sanctions, fraud prevention, and payment transparency. A wire may be used to move criminal proceeds, route funds through higher-risk jurisdictions, obscure the real parties through intermediaries, or execute fraud at speed once an account or payment instruction is compromised. The FFIEC’s red-flag materials include funds transfers to or from secrecy havens or higher-risk jurisdictions without an apparent business reason as relevant indicators of concern.

Wire transfers are also important because they often involve intermediary banks and multiple stages in the payment chain. That creates both utility and risk. The utility is that funds can move efficiently across borders and institutions. The risk is that incomplete or poor-quality information, especially around the originator or beneficiary, can weaken sanctions screening, transaction monitoring, and investigative traceability. FATF’s Recommendation 16 framework is specifically designed to preserve that information across the transfer chain.

In practical terms, firms treat wire transfers as a high-relevance control area because they combine speed, scale, and finality pressures. In some infrastructures, such as Fedwire Funds Service, transfers are immediate, final, and irrevocable once processed. The Federal Reserve says Fedwire is a real-time gross settlement system and that funds transfers are immediate, final, and irrevocable once processed. That makes upstream controls particularly important, because once settlement occurs, opportunities to stop loss or recover funds are much narrower.

A mature control framework for wire transfers therefore depends on several things working together: reliable originator and beneficiary data, sanctions and payment screening, customer and counterparty understanding, transaction monitoring, and strong escalation where payment activity is inconsistent with the relationship or business purpose. In the financial crime environment, the question is not whether wire transfers are inherently suspicious. It is whether the institution can understand and control the risks created by their speed, reach, and ability to move value across the financial system quickly.

Ultimately, wire transfers are significant in the financial crime environment because they are one of the main ways large values move electronically between financial institutions. They are essential to legitimate finance, but they also create major AML, sanctions, fraud, and transparency challenges when payment-chain data is weak or controls are ineffective.