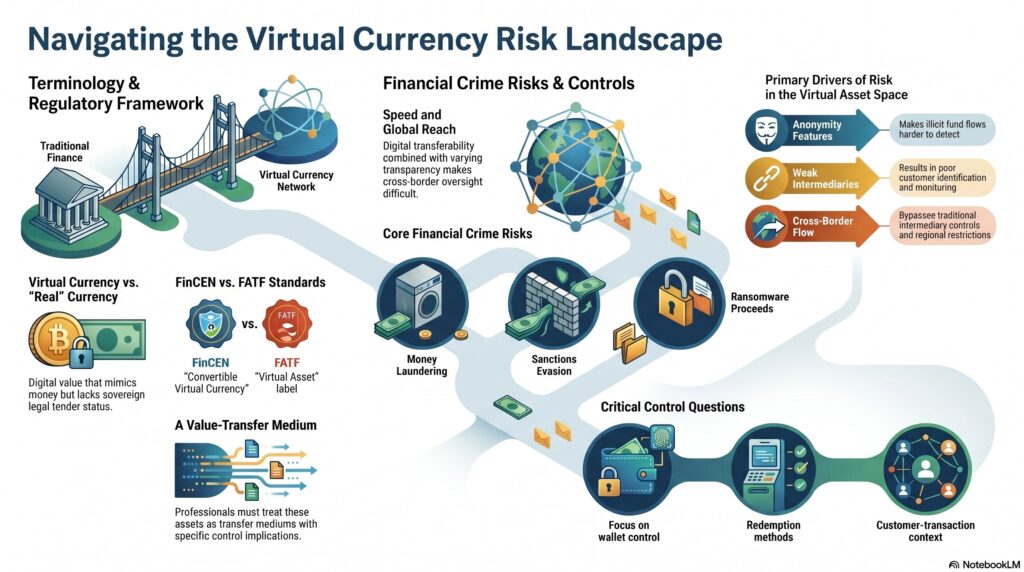

Virtual currency is a digital medium of exchange that can function like money but does not have the legal status of sovereign currency. FinCEN says virtual currency is a medium of exchange that can operate like currency but does not have all the attributes of “real” currency, including legal tender status, and that convertible virtual currency (CVC) is a type of virtual currency that either has an equivalent value as currency or acts as a substitute for currency.

In the financial crime environment, virtual currency matters because it allows value to be stored, transferred, and exchanged digitally outside traditional payment rails. That creates legitimate uses, but also distinct risks around money laundering, fraud, sanctions evasion, ransomware proceeds, scam payments, and cross-border movement of value. FATF now generally uses the term virtual assets (crypto assets) for digital representations of value that can be traded, transferred, or used for payment, and explicitly says this category does not include digital representations of fiat currencies.

From a professional perspective, “virtual currency” is an older but still important term, especially in U.S. FinCEN guidance, while virtual asset has become the broader international standard in FATF materials. That distinction matters because firms may still encounter both labels in policy, law, and operations. FinCEN continues to use virtual currency and CVC terminology in its regulatory guidance, while FATF frames the modern risk landscape through virtual assets and virtual asset service providers.

Watch on YouTube: Virtual Currency

A key reason virtual currency is significant is that it combines speed, digital transferability, and cross-border reachwith varying degrees of transparency or opacity depending on the asset, wallet structure, and service provider. In the financial crime environment, that means virtual currency can be used for legitimate investment and payment activity, but it can also be used to move proceeds of fraud, obscure fund flows, or bypass traditional intermediary controls. FATF’s updated virtual asset guidance says jurisdictions must assess and mitigate the risks associated with virtual asset activity and subject providers to relevant AML/CFT measures.

This is why virtual currency is closely linked to AML and sanctions controls. The financial crime concern is not simply that the asset is digital. The concern is whether the activity involves anonymity-enhancing features, weak intermediary oversight, poor customer identification, or cross-border flows that make illicit activity harder to detect. FATF’s virtual asset materials stress that virtual asset service providers should be subject to the same relevant AML/CFT measures that apply to financial institutions.

A mature professional view therefore treats virtual currency as a value-transfer medium with specific control implications, not just as a technology label. The key questions are who controls the wallet or account, how the asset is acquired and redeemed, whether an intermediary is involved, what screening and monitoring exist, and whether the customer and transaction make sense in context. In regulatory practice, those questions now sit increasingly within the broader virtual-asset framework, even where the older term virtual currency remains in use.

Ultimately, virtual currency is important in the financial crime environment because it represents digital value that can mimic some functions of money without being sovereign legal tender. That makes it commercially significant and also a major focus for AML, sanctions, fraud, and regulatory controls.