The USA PATRIOT Act is the post-September 11, 2001 U.S. law that significantly expanded the anti-money laundering and counter-terrorist-financing framework applying to the financial system. FinCEN’s official summary says the Act was intended to strengthen U.S. measures to prevent, detect, and prosecute international money laundering and terrorist financing, subject higher-risk foreign jurisdictions and institutions to special scrutiny, require broader reporting of potential money laundering, and make records more useful to investigators.

In the financial crime environment, the significance of the USA PATRIOT Act is that it reshaped AML from a narrower reporting framework into a more expansive risk-based, intelligence-linked control regime. Its importance is not just historical. Many of the core concepts still used in financial crime compliance today — customer identification, correspondent banking due diligence, information sharing, and stronger institutional AML obligations — were materially reinforced or operationalized through the Act and its implementing rules.

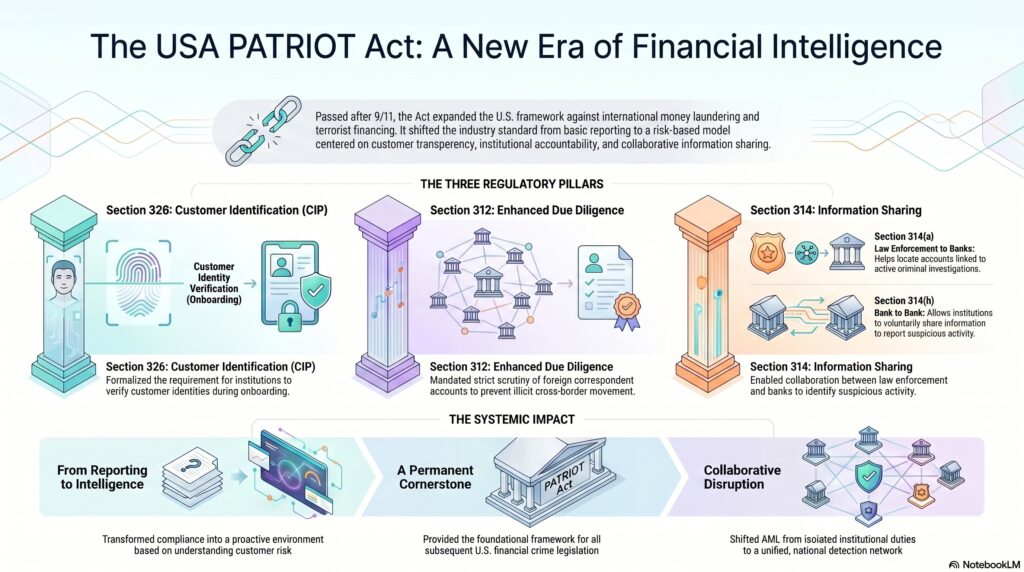

From a professional perspective, one of the Act’s most important legacies is Section 326, which led to the modern Customer Identification Program (CIP) requirement. FinCEN’s official CIP guidance says the final CIP rule implements Section 326 of the USA PATRIOT Act and requires covered financial institutions to maintain a Customer Identification Program. In practical terms, this helped formalize the idea that firms must verify enough about a customer’s identity at onboarding to support a credible AML framework.

Watch on YouTube: USA PATRIOT Act

Another major provision is Section 312, which requires due diligence — and in some cases enhanced due diligence — for certain foreign correspondent accounts and private banking accounts. The FFIEC says the goal of Section 312 is to help prevent money laundering through accounts that give foreign financial institutions a base for moving funds through the U.S. financial system. This remains highly relevant because correspondent banking is one of the main channels through which cross-border illicit finance can move if transparency and oversight are weak.

The Act is also central because of Section 314, especially 314(a) and 314(b). FinCEN’s current materials explain that Section 314(a) enables law enforcement, through FinCEN, to reach out to certain financial institutions to locate accounts and transactions linked to investigative subjects, while Section 314(b) permits financial institutions, after notifying Treasury, to share information with one another to identify and report activity that may involve money laundering or terrorist activity. In the financial crime environment, that is a major shift toward making AML more intelligence-driven and collaborative rather than purely institution-by-institution.

This is why the USA PATRIOT Act matters beyond any single provision. It helped push financial crime compliance toward a model based on customer transparency, higher-risk account scrutiny, broader AML program obligations, and structured information sharing. The result was a more proactive control environment in which institutions were expected not only to file reports, but to understand customers, identify risk, and cooperate in disrupting illicit finance. This is an inference supported by FinCEN’s official summary of the Act’s objectives and by the implementing guidance for Sections 312, 314, and 326.

It is also important to place the Act in today’s context. The USA PATRIOT Act remains foundational, but it no longer stands alone. Later legislation, including the Anti-Money Laundering Act of 2020, built on and updated the U.S. AML framework rather than replacing the PATRIOT Act’s core legacy. That means the PATRIOT Act is best understood as a cornerstone of the modern U.S. financial crime regime, especially in relation to AML, terrorist financing prevention, correspondent banking controls, and information sharing.

Ultimately, the USA PATRIOT Act matters in the financial crime environment because it transformed how the U.S. financial system is expected to prevent and detect illicit finance. It strengthened onboarding controls, expanded scrutiny of higher-risk relationships, enabled broader information sharing, and reinforced the role of financial institutions as active participants in national financial crime detection and disruption.