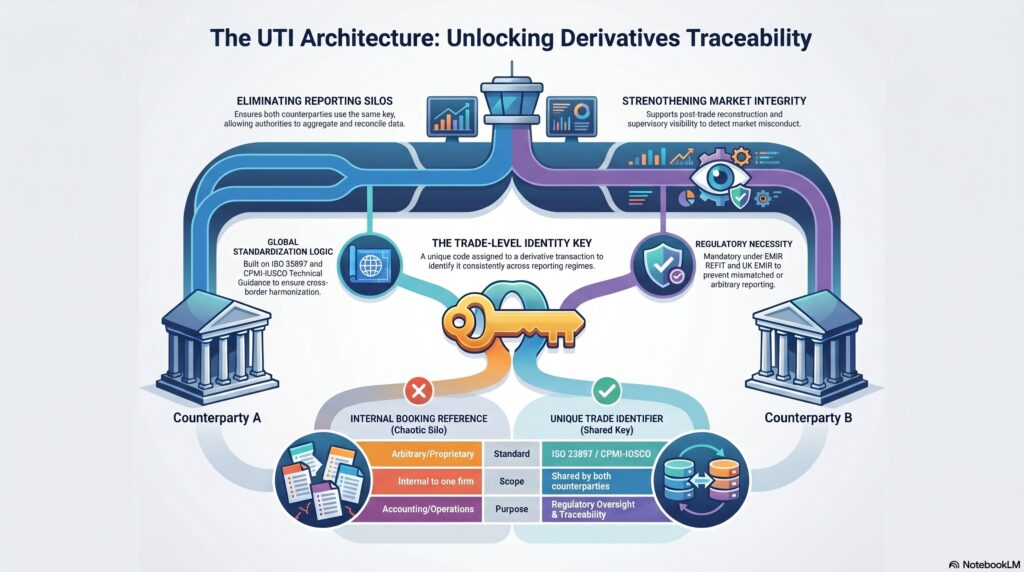

A Unique Trade Identifier (UTI) is a unique code assigned to a reportable derivatives transaction so that both counterparties and trade repositories can identify the same trade consistently across regulatory reporting. ESMA’s EMIR REFIT guidance describes the UTI as a unique code of a derivative between two counterparties, and the FCA’s UK EMIR reporting Q&A says the updated UTI structure in UK EMIR is based on the CPMI-IOSCO Technical Guidance on the Harmonisation of the Unique Transaction Identifier.

In the financial crime environment, the UTI matters because it strengthens traceability, reconciliation, and supervisory visibility in derivatives markets. It is not itself an AML or sanctions control, but it is a foundational data element that helps authorities and firms ensure that the same transaction is reported consistently and can be followed across counterparties, trade repositories, and regulatory datasets. ESMA said these harmonised data elements are essential for the aggregation of data by authorities, specifically through the use of the UTI and related identifiers.

From a professional perspective, the UTI is best understood as a trade-level identity key. Its purpose is to avoid a situation where the same derivative is reported differently by each side and becomes difficult to match, reconcile, or supervise. Under EMIR REFIT, ESMA says a pair of counterparties should use a specific UTI for one single derivative. The FCA’s UK EMIR materials likewise require use of an ISO 23897 UTI and state that counterparties must determine the entity responsible for generating it in line with the applicable waterfall logic.

Watch on YouTube: Unique Trade Identifier (UTI)

This is important in the financial crime environment because derivatives markets can be complex, cross-border, and highly data-intensive. If authorities cannot reliably identify that two reports relate to the same transaction, the quality of oversight weakens. Better UTI usage improves reporting consistency and supports market transparency, supervisory review, and post-trade reconstruction. This is an inference supported by ESMA’s and the FCA’s emphasis on UTI-driven aggregation and reconciliation of derivatives data.

The UTI is especially relevant under EMIR and UK EMIR reporting. The FCA states that UTIs generated by non-UK counterparties under another reporting regime should still align with UK EMIR formatting requirements, which shows the importance of cross-border harmonisation. CPMI-IOSCO’s guidance was developed specifically to harmonise UTIs for reportable OTC derivatives across jurisdictions.

A key professional point is that the UTI is not a commercial label or an internal booking reference. It is a regulatory identifier used to support accurate trade reporting and supervisory data quality. The FCA’s validation rules and policy materials show that uniqueness must be preserved at counterparty level and that the identifier structure is prescribed rather than arbitrary.

Ultimately, the UTI matters in the financial crime environment because it helps make derivatives transactions uniquely identifiable, reconcilable, and traceable across the reporting chain. That improves the quality of post-trade transparency and supports the wider control environment for market oversight, misconduct detection, and supervisory data integrity.