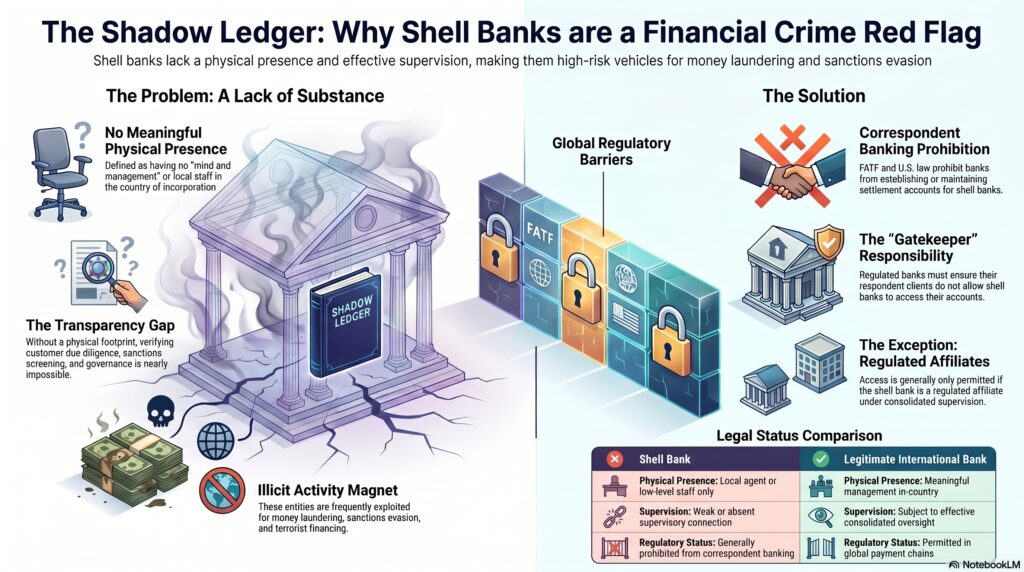

A shell bank is a bank that has no physical presence in the country in which it is incorporated and licensed and is not affiliated with a regulated financial group subject to effective consolidated supervision. FATF’s glossary uses that definition and adds that “physical presence” means meaningful mind and management located within a country, not merely a local agent or low-level staff. In the U.S. BSA framework, the narrower legal term foreign shell bank is defined in 31 CFR 1010.605(g) as a foreign bank without a physical presence in any country.

In the financial crime environment, shell banks matter because they create extreme transparency and control problems. A bank with no real physical presence and weak or absent supervisory connection can be difficult to assess, difficult to oversee, and easier to misuse for money laundering, sanctions evasion, terrorist financing, or other illicit financial activity. FATF therefore prohibits financial institutions from entering into, or continuing, correspondent banking relationships with shell banks, and also requires institutions to satisfy themselves that respondent banks do not permit their accounts to be used by shell banks.

Watch on YouTube: Shell Bank

From a professional perspective, the concern is not simply that a bank operates internationally or digitally. The issue is the absence of meaningful presence and effective supervision. A legitimate international bank may operate across borders while still having real management, licensing, and consolidated oversight. A shell bank, by contrast, lacks that substance, which makes due diligence and regulatory accountability much weaker. FATF’s definition is built precisely around this distinction between genuine regulated presence and a nominal banking entity with no meaningful location or oversight.

This is why shell banks are especially relevant in correspondent banking. Correspondent relationships allow one bank to access payment and settlement services through another bank’s infrastructure. If shell banks are allowed into that chain, they can gain indirect access to the wider financial system without the level of transparency and supervision expected of regulated institutions. The FFIEC states that banks are prohibited from establishing, maintaining, administering, or managing a correspondent account in the United States for, or on behalf of, a foreign shell bank, unless the foreign shell bank is a regulated affiliate.

In practical financial crime terms, shell banks are a high-risk concern because they can weaken confidence in who is really behind a payment, account, or institutional relationship. If the institution itself lacks real substance, the quality of its customer due diligence, sanctions screening, transaction monitoring, and governance may also be unreliable or unverifiable. That is why prohibition, rather than mere enhanced monitoring, is the core response in major AML frameworks. This is an inference supported by FATF Recommendation 13 and the U.S. prohibition in 31 CFR 1010.630.

Ultimately, a shell bank is significant in the financial crime environment because it represents a banking vehicle without the physical presence and supervisory substance needed to support trust, transparency, and accountability. For that reason, shell banks are treated not as ordinary higher-risk institutions, but as entities that regulated financial institutions are generally prohibited from serving through correspondent relationships.