Real-time processing is the execution and handling of transactions, messages, or control decisions as they occur, with little or no delay between initiation, validation, and outcome. In payments, this usually means funds verification, decisioning, and processing happening immediately rather than through batch cycles or deferred review. The ECB describes instant payments as making funds available within seconds, and OFAC notes that instant payment systems create an expectation that funds be made available to the payee in real time.

In the financial crime environment, real-time processing matters because it changes the timing of risk management. In slower, batch-based environments, firms may have more time to review exceptions, investigate alerts, or intervene before funds settle or become available. With real-time processing, much of that decision-making has to happen before or during execution. The Federal Reserve’s authentication guidance notes that digital payment services can involve shorter processing windows and limited time for fraud management, while its pay-by-bank analysis says instant payment systems use real-time funds verification and real-time fraud monitoring.

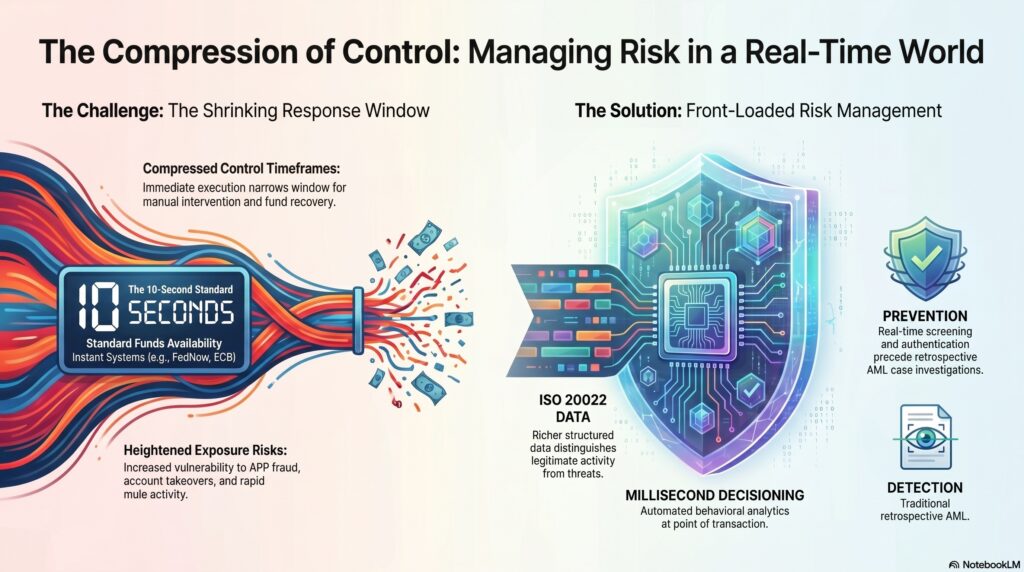

From a professional perspective, real-time processing is not just a technology feature. It is an operating model with direct implications for fraud prevention, sanctions compliance, AML monitoring, and operational resilience. The core issue is that once a real-time transaction is executed and funds are available, the window for prevention or recovery narrows sharply. OFAC’s guidance for instant payment systems emphasizes exactly this point by warning that real-time availability can create sanctions-compliance challenges unless controls are built into the design.

Watch on YouTube: Real-Time Processing

This is why real-time processing increases the importance of front-loaded controls. Firms need stronger authentication, better customer and device understanding, faster sanctions screening, more reliable payment data, behavioral analytics, and escalation logic capable of acting in milliseconds or seconds rather than hours. In the financial crime environment, that means controls must shift closer to the point of transaction rather than relying mainly on retrospective review. This is an inference supported by OFAC’s instant-payments compliance guidance and the Federal Reserve’s discussion of shorter fraud-management windows.

Real-time processing is especially relevant to instant payments and faster payments systems. The ECB’s instant payments materials define these as transfers where funds are made available within ten seconds, and the Federal Reserve’s materials on pay-by-bank and FedNow note real-time verification and fraud tools as part of the control environment. In practical terms, this means real-time processing is closely tied to customer expectations of immediacy, but also to heightened exposure to APP fraud, account takeover, mule-account activity, and rapid onward movement of proceeds.

A key control implication is that real-time processing raises the value of better data. The Bank of England’s ISO 20022 materials say richer structured payment data can bring improved fraud prevention and greater information and analysis capabilities. That matters because faster decision-making is only credible if the system has enough high-quality information to distinguish legitimate activity from suspicious or prohibited activity at speed.

At the same time, real-time processing does not eliminate the need for post-event monitoring. It changes the balance between preventive and detective control. Firms still need retrospective AML review, suspicious-activity escalation, and case investigation, but they also need real-time screening and fraud decisioning where the opportunity to stop harm still exists. The Federal Reserve’s materials explicitly point to real-time transaction monitoring and reporting as fraud-mitigation tools in instant payment systems.

Ultimately, real-time processing is significant in the financial crime environment because it compresses the time available to detect and stop fraud, sanctions breaches, and suspicious payments. It supports faster and more seamless financial services, but it also demands stronger upstream controls, better data, and more immediate decision-making. For that reason, real-time processing should be understood not simply as faster execution, but as a control challenge that reshapes how financial crime risk must be managed.