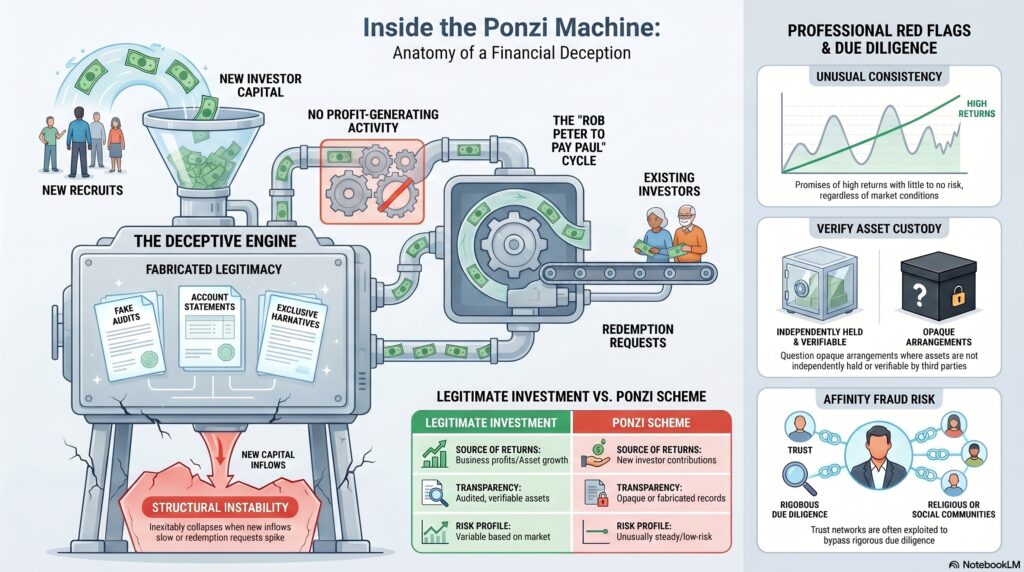

A Ponzi scheme is an investment fraud in which returns paid to existing investors come primarily from money contributed by new investors rather than from genuine profit-generating activity. The SEC’s Investor.gov defines a Ponzi scheme in exactly those terms, and the FBI similarly says Ponzi schemes use current investors’ money to pay previous investors and inevitably collapse.

In the financial crime environment, a Ponzi scheme is significant because it is not simply a bad investment or a business failure. It is a deception-based financial crime that depends on creating a false appearance of legitimate performance, steady returns, and controlled risk. Investors are led to believe that profits are being generated through genuine trading, asset management, lending, or other business activity, when in fact the scheme is being sustained by continuous inflows from newer victims. The SEC notes that promoters often promise high returns with little or no risk, even though the money is frequently not invested as claimed.

From a professional perspective, the central feature of a Ponzi scheme is cash-flow dependence on recruitment of new capital. The scheme survives only while enough new money arrives to fund redemptions, purported returns, and the promoter’s own extraction of funds. That is why Ponzi schemes are structurally unstable. They can appear credible for long periods, especially when markets are calm and investors do not withdraw heavily, but they eventually fail when inflows slow, redemption requests rise, or scrutiny exposes the absence of genuine underlying returns. The FBI states plainly that Ponzi schemes inevitably collapse.

Watch on YouTube: Ponzi Scheme

A key control issue is that Ponzi schemes often create the illusion of legitimacy. Fraudsters may produce account statements, fabricated valuations, fake audits, false custodial arrangements, or convincing narratives about proprietary strategies and exclusive access. Early investors may even receive real payments, which reinforces trust and encourages reinvestment or referrals. But those payments are not evidence of genuine investment success; they are usually distributions funded by later investors. The SEC’s investor materials emphasize this exact mechanism.

In the financial crime environment, Ponzi schemes matter for several reasons at once. They are a form of investment fraud, but they also create money-laundering and control-risk issues. Funds may move through multiple accounts, affiliated entities, feeder structures, or professional intermediaries. False records may be used to conceal the real source and use of investor money. Customer due diligence, source-of-funds review, transaction monitoring, and suspicious activity escalation can all become relevant, especially where fund flows or claimed strategies do not align with the commercial reality of the business. This is an inference supported by the SEC and FBI definitions together with the broader financial crime-control logic of proceeds movement and concealment.

Ponzi schemes also overlap frequently with affinity fraud. The SEC warns that many affinity frauds are Ponzi or pyramid schemes, where money from new investors is paid to earlier investors to create the illusion that the investment is successful. This matters professionally because affinity-based trust networks can reduce skepticism and make due diligence less rigorous, particularly where the promoter is embedded in a religious, ethnic, professional, or social community.

A mature financial crime perspective therefore looks beyond the headline promise of returns and asks more fundamental questions. What is the actual business model? Where are returns coming from? Are assets independently held and verifiable? Do redemption patterns depend heavily on continuing subscriptions? Are account statements, audits, and counterparties credible? Does the pattern of cash flow make sense if the stated strategy were real? These questions are critical because Ponzi schemes often fail not only because of one dramatic lie, but because institutions and investors do not challenge whether the underlying economics are plausible. This is an inference based on the SEC’s description of how purported returns are funded.

Operationally, firms may encounter Ponzi risk through unusual investment products, referral-heavy distribution models, opaque custody arrangements, unexplained consistency of returns, unusual redemption behavior, or customer funds flowing through structures that do not match the stated investment purpose. In a financial crime framework, these are not just investment suitability issues; they may indicate large-scale deception, misappropriation, and wider illicit fund movement. This is an inference supported by the SEC and FBI definitions and by how Ponzi schemes function in practice.

Ultimately, a Ponzi scheme is a major financial crime threat because it uses trust, false performance, and continual inflows of new money to sustain the appearance of a legitimate investment enterprise. It harms investors directly, distorts financial decision-making, and often creates wider fraud, money movement, and control-failure issues for institutions connected to the scheme. For that reason, Ponzi schemes should be treated not merely as classic investment scams, but as structurally deceptive financial operations requiring strong due diligence, transaction scrutiny, and governance challenge.