A money mule is a person who transfers or moves money on behalf of criminals, often through their own bank account or other payment channels. Europol describes money muling as a type of money laundering in which a person receives money from a third party and transfers it to another account, in cash, or by another method. The FCA’s 2025 review similarly defines money muling as a money laundering technique where an individual moves the proceeds of crime on behalf of criminals, sometimes unwittingly.

In the financial crime environment, money mules are significant because they provide the bridge between predicate crime and the laundering process. Fraud, scams, cybercrime, and other offences often generate proceeds that cannot be moved safely by the criminals themselves without creating obvious links. Mule accounts solve that problem by receiving the funds first and then sending them onward through transfers, cash withdrawals, cards, money services businesses, or crypto channels. Europol and FinCEN both describe money mule schemes as a way for criminals to move and disguise proceeds while distancing themselves from the original offence.

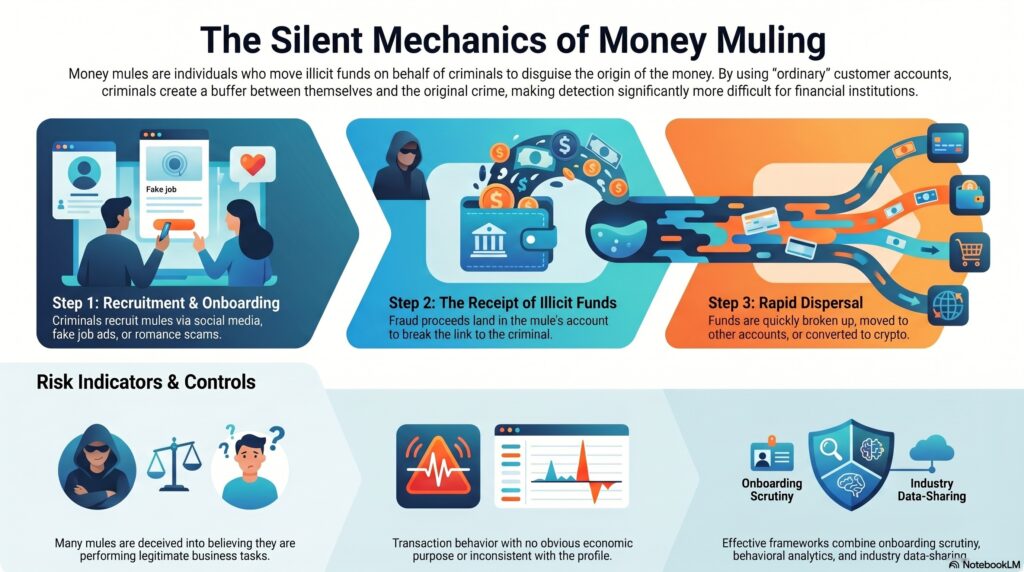

From a professional perspective, money mules matter because they sit at the intersection of fraud prevention, AML, customer-risk management, and account monitoring. A mule account may look like an ordinary customer account, especially at onboarding. The account holder may be a student, a new customer, someone facing financial pressure, or a person recruited through social media, fake jobs, romance scams, or other deceptive approaches. FATF’s work on cyber-enabled fraud notes that criminals recruit money mules across borders at scale, often through social media and messaging platforms.

Watch on YouTube: Money Mules

A key practical point is that not all money mules are knowingly complicit. Some are fully aware they are helping criminals and do so for payment. Others are deceived into believing they are acting as payment agents, processing business payments, handling “job” tasks, or helping someone they trust. The FCA’s 2025 publication explicitly notes that some individuals involved in money muling are unwitting, and Europol’s public guidance makes the same point. That distinction matters for customer treatment and investigations, but it does not reduce the laundering risk created by the account activity itself.

Operationally, mule accounts are important because they are often the receiving point for scam and fraud proceeds. In APP fraud, business email compromise, romance scams, and cyber-enabled fraud, the victim’s payment frequently lands in an account controlled or used by a mule. Once the funds arrive, they are often broken up, moved quickly onward, withdrawn, or converted, which makes tracing and recovery harder. The FCA’s work on proceeds of fraud and money mules is built around this reality and treats mule detection as a core anti-fraud and AML control priority.

This means money mule risk is not just an AML issue after the fact. It is also a customer lifecycle issue. Firms need controls at onboarding, during account use, and at the point of receiving suspicious payments. Relevant indicators can include accounts opened on weak or unusual narratives, activity inconsistent with the customer profile, rapid receipt and dispersal of funds, multiple unrelated incoming payments, sudden changes in usage, and transaction behavior with little obvious economic purpose. The FCA’s 2023 and 2025 reviews both focus on firms’ systems and controls for detecting and preventing mule activity in payment accounts.

A mature control framework therefore needs more than simple transaction monitoring. It should combine onboarding scrutiny, behavioural analytics, receiving-account monitoring, fraud intelligence, industry data-sharing where available, and strong investigative escalation. The FCA’s review on firms’ use of the National Fraud Database and mule-account detection tools reflects the importance of combining internal controls with wider intelligence.

Ultimately, money mules are critical in the financial crime environment because they are one of the main ways criminals move proceeds while hiding their own identity and role. They allow fraud to become laundering, and they turn ordinary customer accounts into temporary criminal infrastructure. For that reason, money mule detection should be treated as a core priority across fraud, AML, payments, and customer-risk functions.