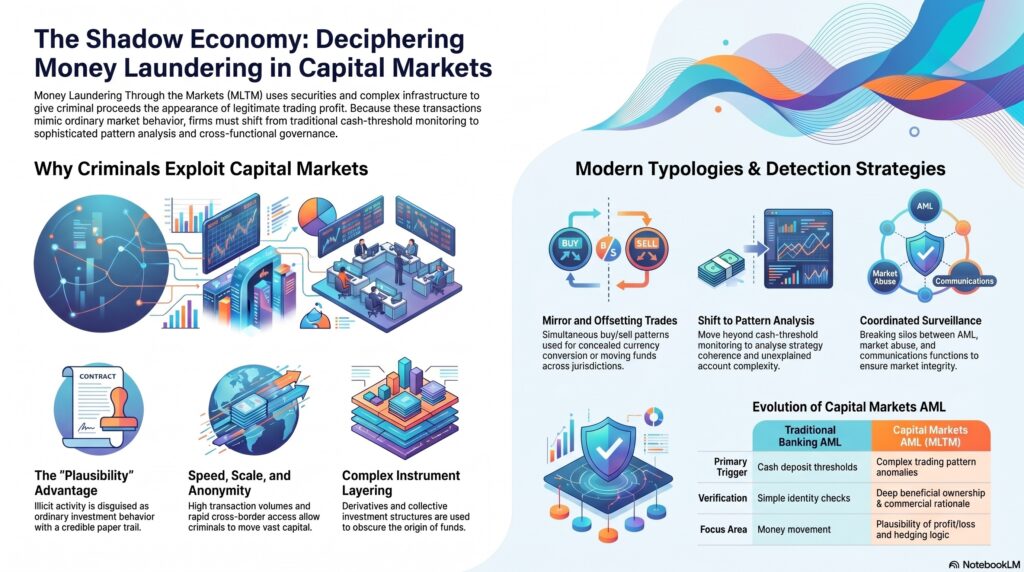

Money laundering in capital markets is the use of securities, derivatives, funds, trading accounts, and related market infrastructure to move criminal proceeds in a way that makes them appear to arise from legitimate investment or trading activity. The FCA’s 2025 review defines money laundering through the markets (MLTM) as the use of capital markets to launder funds obtained through criminal activity so that they appear legitimately generated from trading activity, and says the threat is continuing to rise as criminals exploit complex products and the movement of large volumes of capital.

In the financial crime environment, this typology matters because capital markets offer exactly the features criminals value: speed, scale, cross-border access, complex instruments, layered intermediaries, and transactions that can have plausible commercial explanations. FATF’s work on the securities sector says the sector provides core access to the financial system and that characteristics such as high volumes, speed, and anonymity can create opportunities for money laundering and terrorist financing.

From a professional perspective, money laundering in capital markets is not limited to one tactic. It can involve the use of brokerage accounts, listed securities, fixed income products, derivatives, collective investment structures, custody arrangements, and cross-market trading patterns to place, layer, or integrate illicit funds. FATF’s securities-sector study notes vulnerabilities at all three stages of the laundering cycle, while the FCA’s 2025 review stresses that MLTM is a broad and evolving threat rather than a single scenario.

A key reason this area is difficult is that the underlying activity can look like ordinary market behavior. Buying and selling securities, moving cash through trading accounts, settling transactions across jurisdictions, or holding assets through layered corporate structures may all be legitimate. The control challenge is to determine whether the activity has a genuine investment or hedging rationale, or whether the market activity is simply being used as a vehicle to obscure origin, ownership, or destination of funds. The FCA says capital markets facilitate the movement of vast amounts of capital from different geographical regions with relative ease, making detection challenging.

Watch on YouTube: Money Laundering in Capital Markets

This is why capital-markets laundering often relies on plausibility rather than obvious anomaly. Funds may be routed through accounts that appear professionally managed, invested in liquid instruments, or moved through transactions that generate a paper trail of seemingly legitimate profit and loss. The laundering objective is not only concealment, but the creation of a credible explanation for wealth. FATF’s securities-sector work explicitly states that illicit funds can be placed into the securities industry and then layered or integrated through market activity.

Certain typologies are especially important. These include mirror trading and offsetting trades, use of securities transactions for concealed currency conversion, misuse of omnibus or introduced-account structures, rapid in-and-out trading with little economic rationale, suspicious subscriptions and redemptions in investment products, and trading patterns inconsistent with the customer profile. FINRA’s AML red flags include mirror trades or transactions involving securities used for currency conversions, and the FCA’s 2025 review refers back to the Deutsche Bank mirror-trading case as a major example of how capital markets can be misused for laundering.

The role of intermediaries is central. Brokers, dealers, investment firms, private banks, clearing participants, and fund-related service providers may each see only part of the overall pattern. FATF’s risk-based approach for the securities sector emphasizes that different activities and services offered by securities-sector participants present different ML/TF risks, which means firms cannot rely on generic banking assumptions when building controls for market activity.

A mature control framework therefore starts with strong customer due diligence and beneficial ownership analysis. In capital markets, that means understanding not only who the legal customer is, but also who ultimately controls the account, where the wealth comes from, why the products used make sense, how the account is expected to behave, and whether the trading strategy is commercially coherent. The FCA’s 2025 review highlights gaps in firms’ understanding of customers and notes the importance of robust systems, controls, risk awareness, and training in wholesale markets.

Ongoing monitoring is equally important, but it needs to be tailored to markets activity rather than copied from retail banking. Traditional cash-threshold thinking is often less useful in capital markets than pattern analysis. Firms need to look for unnecessary complexity, offsetting trades, unexplained transfers between related accounts, unusual use of low-risk liquid instruments as movement channels, sudden shifts in strategy, and transaction flows that do not fit the client’s stated purpose. FATF’s securities-sector guidance supports a risk-based approach precisely because the typologies and delivery models vary widely across the sector.

Market-integrity and AML controls also overlap here. ESMA notes that the market abuse framework is intended to guarantee market integrity and increase investor confidence, and in its MAR review it indicated that schemes such as mirror trading can damage market integrity even where the concern is not only classic market abuse. That means firms in capital markets need coordinated surveillance across AML, market abuse, communications, and client-risk functions rather than isolated control silos.

Governance is a decisive factor. The FCA’s 2026 wholesale-markets regulatory priorities keep money laundering through the markets on the supervisory agenda, showing this is not a niche historical issue. Senior management should understand where capital-markets laundering risk sits in the business, whether surveillance is calibrated to the products and client base, whether control functions can connect activity across desks and entities, and whether staff in the front office understand that seemingly sophisticated market activity can still be financially criminal in purpose.

Ultimately, money laundering in capital markets is a serious financial crime threat because it uses the appearance of legitimate investment activity to hide illicit origin and create lawful-looking proceeds. It is harder to identify than simple cash placement because the transactions often carry commercial form, market language, and institutional legitimacy. For that reason, firms active in securities and derivatives markets need AML frameworks that understand the specific typologies of the sector, not just the general principles of banking AML.