Know Your Employee, or KYE, refers to the policies, procedures, and controls an institution uses to understand its employees well enough to identify insider risk, conflicts of interest, misconduct indicators, and vulnerabilities that could expose the firm to financial crime. ACAMS defines KYE as anti-money laundering policies and procedures for acquiring a better knowledge and understanding of employees for the purpose of detecting conflicts of interest, money laundering, past criminal activity, and suspicious activity.

In the financial crime environment, KYE is significant because firms do not face risk only from customers, counterparties, and external criminals. They also face risk from people inside the organization who may misuse access, ignore controls, conceal misconduct, be compromised by external actors, or facilitate fraud, money laundering, sanctions breaches, or market abuse. A financial crime framework that focuses only on customers and transactions, while neglecting employee integrity and insider risk, leaves a critical gap in the control environment. This is an inference supported by the ACAMS definition of KYE and by broader regulatory focus on insider threat and employee conduct within financial institutions.

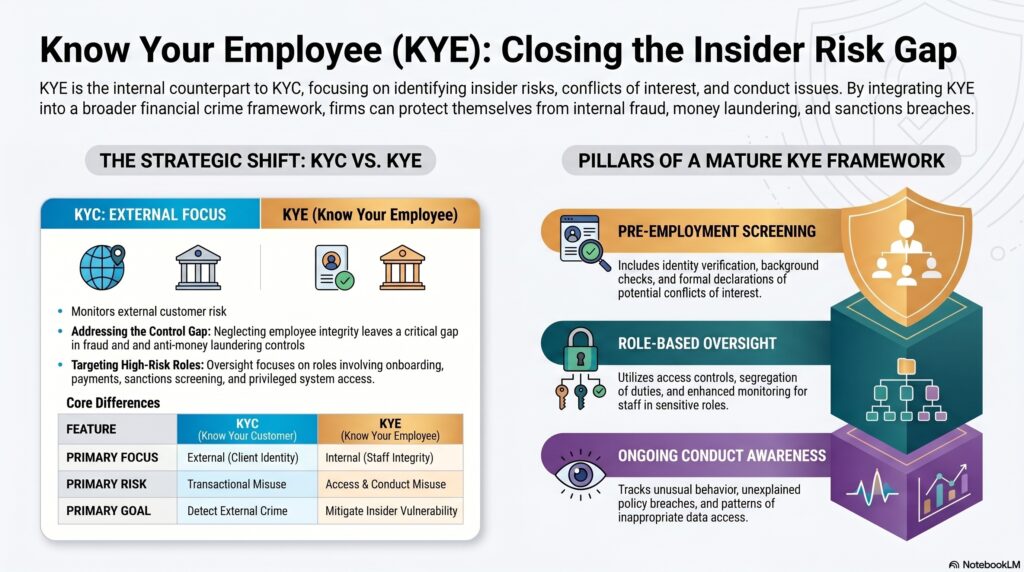

From a professional perspective, KYE is the employee-side counterpart to KYC. KYC seeks to understand who the customer is and what risk they present. KYE seeks to understand who the employee is, what access they have, whether their conduct or background creates risk, and whether there are indicators that they may be vulnerable to corruption, coercion, collusion, or misuse of privileged systems and information. The aim is not indiscriminate scrutiny of employees. It is proportionate risk management around roles that can materially affect the firm’s exposure to financial crime. This is an inference based on the core purpose described in the ACAMS glossary entry.

Watch on YouTube: Know Your Employee (KYE)

In practice, KYE is especially relevant for staff in higher-risk roles. These may include onboarding teams, relationship managers, payments and operations staff, sanctions and screening analysts, transaction-monitoring teams, trading and markets personnel, control-room staff, privileged technology users, and employees with access to customer data, payment approvals, case-management systems, or sensitive market information. The more a role can open access, suppress alerts, alter data, influence customer acceptance, or move funds, the greater the value of strong KYE controls. This is a professional inference supported by the ACAMS definition’s focus on conflicts of interest, suspicious activity, and prior criminal concerns.

A mature KYE framework usually includes several components. One is pre-employment screening, including identity verification, background checks where lawful and appropriate, conflict-of-interest declarations, qualifications verification, and review of role-specific integrity risks. Another is role-based oversight once the employee is in post, including access controls, segregation of duties, supervision, personal account dealing controls where relevant, and enhanced monitoring for staff in sensitive roles. A third is ongoing conduct awareness, including monitoring for unusual behaviour, unexplained policy breaches, inappropriate data access, override patterns, and other indicators that an employee may be acting dishonestly or under pressure. This structure is a practical inference from the purpose of KYE as understanding employees to detect risks before they become misconduct.

KYE is also closely linked to insider threat and conduct risk. An employee may present financial crime risk not only through deliberate collusion, but also through negligence, weak judgment, poor security behaviour, or susceptibility to social engineering and coercion. In that sense, KYE is not just about identifying “bad employees.” It is also about identifying vulnerabilities that could allow a trusted insider to be exploited. A firm with strong KYE practices is better placed to detect when access, incentives, or circumstances are creating risks that could compromise the effectiveness of fraud, AML, sanctions, and market-conduct controls. This is an inference from the employee-risk focus of KYE and the broader financial crime logic of insider-risk management.

There is also a governance dimension. KYE should not be treated as an isolated HR exercise. In the financial crime environment, it belongs within a broader control framework that connects HR, compliance, financial crime, security, operations, and management oversight. The objective is to ensure that employee-risk information is handled lawfully and proportionately, while still enabling the institution to protect sensitive roles and detect concerning patterns. Weak coordination between these functions often leads to blind spots, where concerning employee behaviour is seen in one area but not connected to financial crime exposure elsewhere. This is a professional inference grounded in the control purpose of KYE.

Training and culture are equally important. Employees need to understand not only customer-facing AML and fraud obligations, but also their own personal responsibilities around confidentiality, conflicts, escalation, access use, and internal misconduct. ACAMS material referencing KYE reporting and training illustrates that some institutions use KYE not just for screening, but also for targeting awareness and reinforcing employee accountability.

Ultimately, Know Your Employee matters in the financial crime environment because employees are part of the control framework and, in some cases, part of the threat environment. KYE helps firms understand who has access, where insider risk may exist, and how employee-related vulnerabilities could weaken fraud, AML, sanctions, and conduct controls. For that reason, KYE should be understood as a practical insider-risk and integrity discipline within a mature financial crime framework.