Insider dealing is a form of market abuse in which a person uses inside information to acquire or dispose of financial instruments, or attempts to do so, for their own account or for another person. Under the UK Market Abuse Regulation, insider dealing includes using inside information by acquiring or disposing of financial instruments to which that information relates, and also includes related conduct such as cancelling or amending an order on the basis of inside information. The FCA describes market abuse as behavior that damages the integrity of UK markets and investor confidence.

In the financial crime environment, insider dealing is significant because it strikes at one of the core principles of fair and orderly markets: that participants should not trade on confidential, price-sensitive information unavailable to the wider market. It creates an unfair informational advantage, distorts price formation, undermines confidence in capital markets, and can cause direct harm to other investors who trade without access to the same information. ESMA’s market integrity framework is designed specifically to prevent insider dealing, unlawful disclosure of inside information, and market manipulation in EU markets.

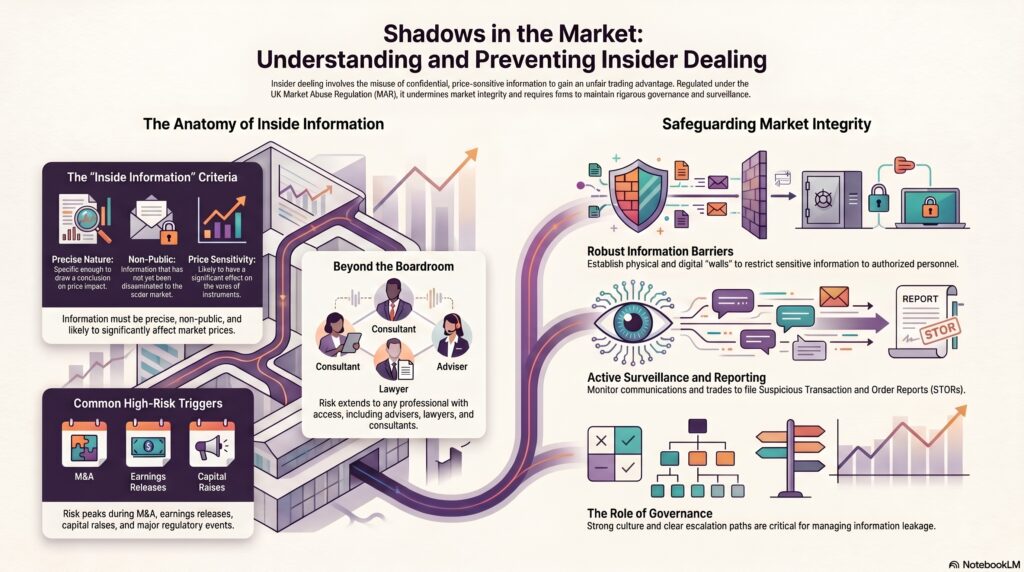

From a professional perspective, insider dealing is not limited to corporate insiders in the narrow sense. The risk extends to anyone who possesses inside information and uses it improperly. That may include employees, advisers, bankers, lawyers, accountants, consultants, brokers, connected persons, or recipients of information passed on through improper channels. UK legislation and MAR guidance focus on possession and misuse of inside information, not just formal corporate title. This matters because many insider dealing cases arise through professional access, deal work, client order knowledge, or information leakage rather than through board-level involvement alone.

Watch on YouTube: Insider Dealing

A central concept here is inside information. Under the UK Market Abuse Regulation, it is information of a precise nature, which has not been made public, relates directly or indirectly to one or more issuers or financial instruments, and would be likely to have a significant effect on prices if it were made public. This definition is important because insider dealing depends not just on confidentiality, but on the market significance of the information. Not all confidential information is inside information, but where confidentiality and price sensitivity combine, the regulatory and criminal risk becomes acute.

In practical terms, insider dealing often arises around earnings, mergers and acquisitions, capital raises, takeover approaches, major contracts, profit warnings, regulatory events, or other material corporate developments. It can also arise in fixed income, derivatives, and other markets where price-sensitive information is held before disclosure. The FCA’s market abuse materials and speeches emphasize that firms must maintain effective controls over confidential and inside information because weak information barriers, poor surveillance, or careless communication can allow insider dealing risk to materialize.

Insider dealing is also closely linked to unlawful disclosure and front-running-like misuse of information. A person may not trade personally, but may tip another person, facilitate trading through an associate, or improperly share confidential deal or issuer information. That means the control framework must address not only direct trading, but also who has access to information, how that information is recorded, what restrictions apply, and whether communications and personal account dealing are effectively monitored. This is an inference supported by the MAR framework’s treatment of insider dealing and unlawful disclosure as linked forms of market abuse.

For firms, effective prevention depends on strong information barriers, control-room processes, restricted and watch lists, wall-crossing procedures, personal account dealing controls, and communications and trade surveillance. The FCA has highlighted the importance of effective information barriers and surveillance arrangements, while SEC and FINRA materials in the U.S. similarly treat misuse of material non-public information as a core market-integrity risk. In UK and EU market environments, firms are also expected to submit suspicious transaction and order reports where they have reasonable grounds to suspect market abuse.

Governance is critical because insider dealing risk often sits where commercial activity and sensitive information meet. Investment banking, research, trading, corporate broking, and advisory functions may all handle information that could move markets. If front-office staff are poorly supervised, incentives discourage escalation, or controls over who knows what and when are weak, the risk of insider dealing rises materially. The FCA’s thematic and supervisory work repeatedly points to governance, information control, and culture as key determinants of whether market abuse risks are properly managed.

Ultimately, insider dealing is a major financial crime and market abuse risk because it converts confidential, price-sensitive information into unfair trading advantage. It harms investors, weakens confidence in markets, and undermines the principle that markets should operate on equal and transparent information. For that reason, insider dealing should be treated as a core market-integrity offence requiring strong information control, surveillance, escalation, and governance across firms that handle sensitive market information.