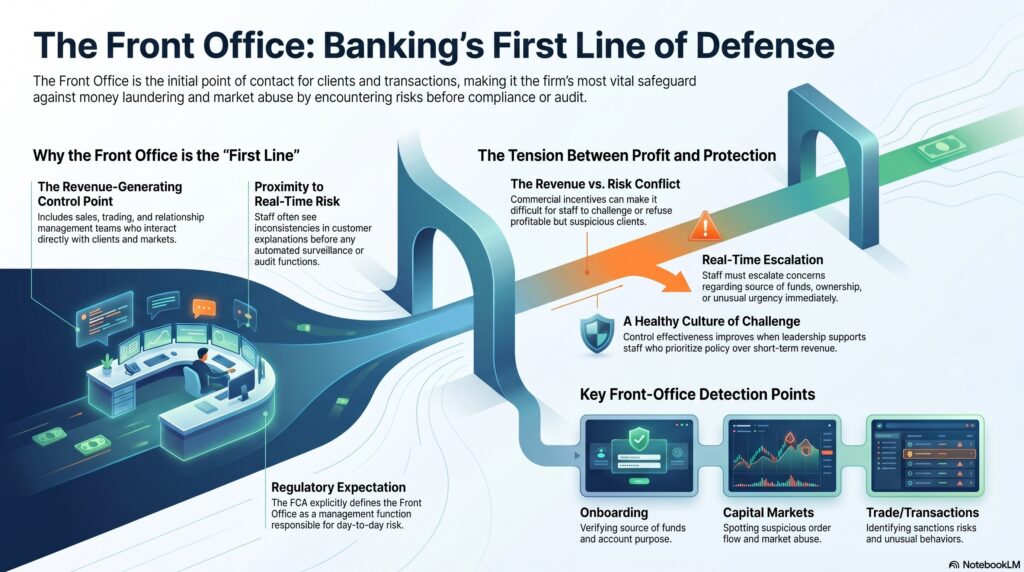

The front office is the customer-facing, revenue-generating part of a financial institution, typically including sales, trading, relationship management, deal origination, and other roles that interact directly with clients, markets, and transactions. In the financial crime environment, the front office is especially important because it often sits within the first line of defense. The IIA’s Three Lines Model describes first-line roles as management functions that lead actions and manage risk in the course of business, and FCA thematic work has explicitly said that the first line of defense includes management, front office, and support functions responsible for day-to-day activities, risks, and controls.

From a professional perspective, the front office is not simply a commercial function. It is one of the earliest control points in the financial crime framework because it often encounters customers, instructions, transactions, and sensitive information before compliance, surveillance, or audit functions do. Relationship managers may see inconsistencies in customer explanations. Sales staff may notice unusual urgency or pressure around transactions. Traders and brokers may encounter suspicious orders or behavior suggestive of market abuse. The FCA has stated that financial services firms are the first line of defence against financial crime and must use systems, processes, data, and new approaches to keep up with emerging risks.

In the financial crime environment, the significance of the front office lies in its combination of proximity to risk and commercial influence. Because front-office staff are close to customers and markets, they often hold information that is highly relevant to fraud, money laundering, sanctions exposure, or market abuse. At the same time, because they are frequently linked to revenue generation and client relationships, they can also face incentives that make effective challenge harder. This tension is one of the central control challenges in financial crime governance. A profitable client may be treated too leniently. A suspicious transaction may not be escalated quickly enough. A problematic order may be accepted because of commercial pressure. The FCA has specifically said that where the front office has information suggesting a client is seeking to trade manipulatively or on the basis of inside information, it should refuse the order where it is able to do so.

Watch on YouTube: Front Office

This makes the front office especially important in several financial crime areas. In onboarding and relationship management, front-office staff may be the first to hear explanations about the purpose of an account, source of funds, expected activity, or ownership structure. In wholesale and capital-markets environments, they may be closest to order flow, client instructions, confidential information, and possible signs of market abuse. In trade and transaction environments, they may see early indicators of sanctions risk, trade-based money laundering concerns, or unusual customer behaviour. If the front office does not escalate concerns or challenge implausible explanations, second-line and third-line functions may only see the issue after risk has already entered the firm. This is an inference supported by the FCA’s description of the front office as part of the first line and by its expectations around order refusal and information control.

A mature financial crime framework therefore expects the front office to do more than originate business. It must also operate controls in real time. That means understanding customer-risk indicators, following onboarding and escalation requirements, respecting information barriers, handling confidential information properly, recognizing red flags, and being willing to challenge business that appears inconsistent with policy or market integrity. FCA materials on healthy cultures also stress that a firm’s three lines of defence should be separate but cohesive, which is directly relevant to how the front office interacts with compliance and audit.

The front office also has an important cultural role. If senior front-office leadership signals that revenue takes priority over challenge, the financial crime framework weakens. If front-office staff are encouraged to escalate concerns early and supported when they do so, control effectiveness improves materially. This is why front-office conduct, incentives, and supervision matter so much in the financial crime environment. The issue is not just whether compliance has written a policy, but whether the people closest to customers and transactions are actually applying it when commercial interests are in play. That is an inference supported by the FCA’s first-line emphasis and broader governance expectations.

Ultimately, the front office is a core part of the financial crime control environment because it is where business opportunity and financial crime risk often meet first. It is the commercial face of the firm, but also a first-line control function with direct responsibility for identifying, challenging, and escalating suspicious activity, problematic clients, and conduct concerns. For that reason, the front office should be understood not only as a revenue generator, but as one of the most important operational lines of defence against fraud, money laundering, sanctions breaches, and market abuse.