Fraud prevention is the set of controls, decisions, and operational practices designed to stop fraud before a loss occurs or before criminal proceeds enter or move through the financial system. In the financial crime environment, it is broader than blocking a suspicious transaction. It includes controlling how customers are onboarded, how identities are verified, how accounts are secured, how payments are challenged, how staff escalate concerns, and how firms design customer journeys to reduce exploitable weakness. The FCA states that firms are a vital line of defence against fraud and wider financial crime, while the FFIEC says financial institutions should rely on multiple layers of control to prevent fraud and safeguard customer information.

From a professional perspective, fraud prevention is most effective when it is treated as a lifecycle discipline rather than a single control point. Fraud can begin at application, continue through account access and payment initiation, and end with the rapid movement of proceeds through mule accounts or other channels. FATF’s work on cyber-enabled fraud stresses that digital fraud is increasingly linked to wider illicit financial flows and that operational responses must address both the fraud event and the movement of proceeds. That means prevention needs to begin before money is lost, not only after suspicious behavior has already become obvious.

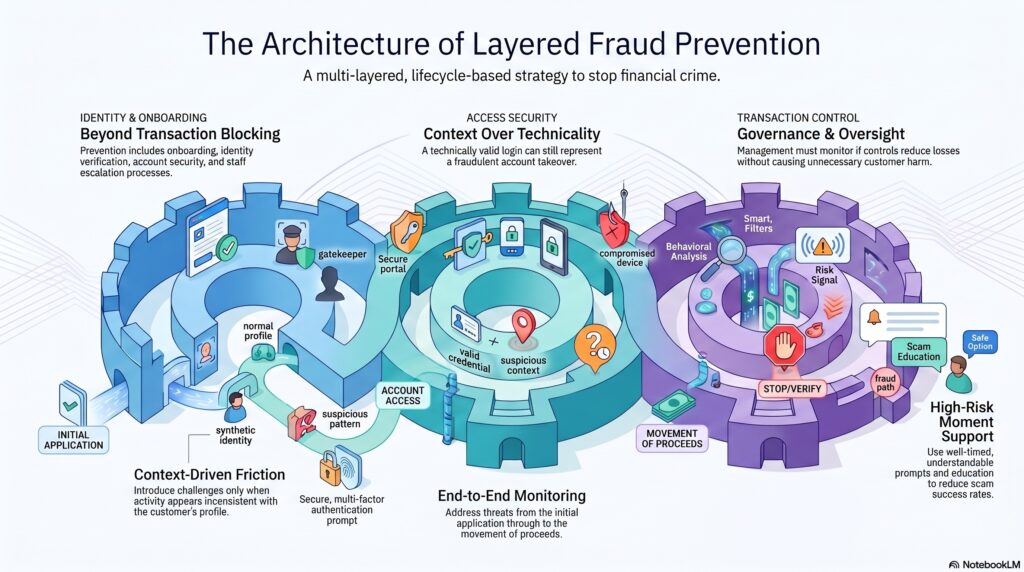

A mature fraud prevention framework usually combines several layers. One layer is strong identity and onboarding control, aimed at preventing application fraud, identity theft, and synthetic identity abuse. Another is access security, including authentication, device controls, and protection against phishing and credential compromise. A third is payment and transaction control, where the firm uses context, behavior, and risk signals to introduce friction or challenge when activity appears inconsistent with the customer profile or account history. FFIEC guidance on authentication and access makes clear that institutions should use layered security and risk management practices rather than relying on a single safeguard.

Watch on YouTube: Fraud Prevention

This layered approach matters because many frauds do not rely on defeating one control. Criminals often exploit small weaknesses across several stages: weak onboarding, reused credentials, poor account recovery, insufficient challenge for beneficiary changes, or limited customer understanding of scam risks. A payment may be technically authorised and still be fraudulent if it was induced by deception. A login may be technically valid and still represent account takeover. Fraud prevention therefore depends on understanding context, not just checking whether a single step was completed correctly. FATF’s cyber-enabled fraud work supports this broader view by linking digital fraud to evolving criminal techniques and to the wider financial crime chain.

Customer protection is also a core part of fraud prevention. Warnings, payment prompts, customer education, and secure servicing processes can materially reduce scam success where they are well timed and understandable. The FCA’s broader financial crime strategy emphasizes reducing and preventing financial crime through coordinated action by firms, regulators, and other stakeholders. In practical terms, this means prevention is not only a matter of back-end analytics; it also depends on how clearly firms communicate risk and how well they support customers at high-risk moments.

Governance is essential. Fraud prevention works only when controls are calibrated, owned, monitored, and updated as threats evolve. Senior management should understand where fraud risk is concentrated, whether existing controls are reducing losses meaningfully, and whether known weaknesses are being remediated. Firms also need to balance prevention with customer experience and operational efficiency: too little friction increases exposure, while poorly designed friction can create unnecessary harm without improving security. The FCA’s Financial Crime Guide points to management oversight, risk assessment, and fraud data as central to fraud control quality.

Ultimately, fraud prevention is one of the most important parts of the financial crime framework because it determines whether a firm can stop fraud before it becomes customer harm, financial loss, or wider illicit fund movement. It is not simply a technical feature or a fraud rule set. It is the practical discipline of designing customer, account, and payment controls that make criminal misuse harder at every stage of the relationship.