Fraud management is the end-to-end framework through which an organization prevents, detects, investigates, responds to, and learns from fraud risk. In the financial crime environment, it is broader than fraud detection alone. It includes governance, risk assessment, control design, customer protection, investigation, escalation, recovery, remediation, and continuous improvement. The FCA states that firms are a vital line of defence against fraud and broader financial crime, and the OCC’s fraud risk management principles say firms should anticipate fraud and deploy a combination of preventive and detective controls.

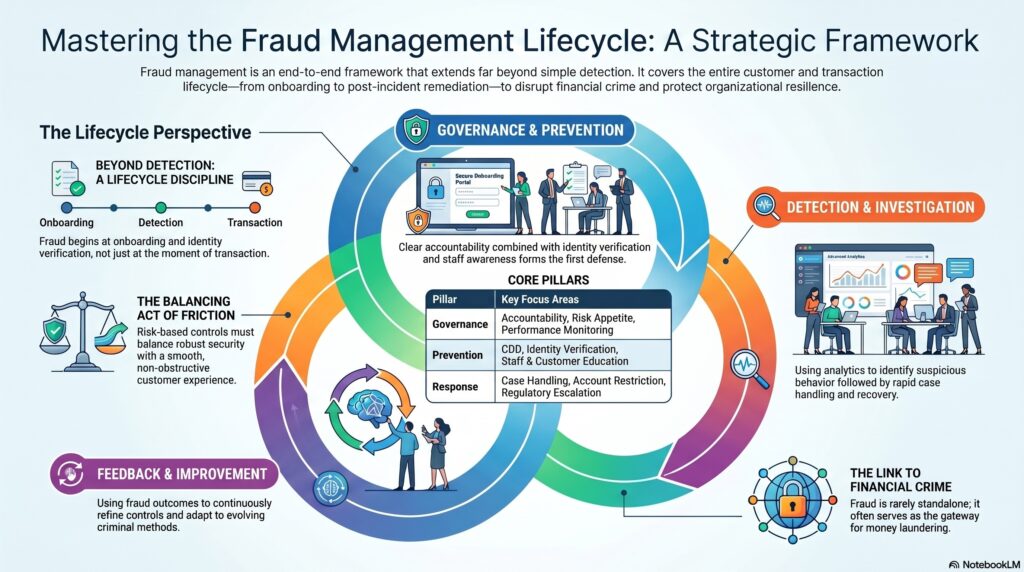

From a professional perspective, fraud management is best understood as a lifecycle discipline. Fraud does not begin and end with a suspicious transaction. It may start with weak onboarding, identity compromise, social engineering, poor account security, weak payment controls, insider misconduct, or gaps in customer communications. Effective fraud management therefore looks across the full customer and transaction lifecycle: application, onboarding, authentication, servicing, payment initiation, account monitoring, investigation, and post-incident remediation. FATF’s recent work on cyber-enabled fraud highlights that modern fraud increasingly overlaps with money laundering and wider AML/CFT risks, which reinforces the need to manage fraud as part of a broader financial crime framework rather than as a narrow operational issue.

A mature fraud management framework usually has five core components. The first is governance and ownership. There must be clear accountability for fraud risk appetite, decision-making, escalation, remediation, and performance monitoring. The second is prevention, including onboarding controls, customer due diligence where relevant, identity verification, account security, staff awareness, and customer education. The third is detection, meaning the ability to identify suspicious behavior through monitoring, screening, analytics, and front-line escalation. The fourth is investigation and response, which includes case handling, customer contact, account restriction, recovery action, suspicious activity assessment, and where necessary regulatory or law-enforcement escalation. The fifth is feedback and improvement, where fraud outcomes are used to refine scenarios, controls, customer journeys, and governance. This lifecycle view is consistent with FCA expectations for firms’ systems and controls and the FFIEC’s focus on monitoring, identifying, researching, and reporting suspicious activity.

Watch on YouTube: Fraud Management

In the financial crime environment, fraud management is especially important because fraud rarely remains a standalone loss event. Fraud proceeds often move through mule accounts, payment chains, or other structures that raise AML concerns. A customer deceived into making a payment may become the source of illicit funds entering another institution. A compromised account may be used to move or layer proceeds. An application fraud may create infrastructure for later criminal use. FATF’s cyber-enabled fraud report is explicit that digital fraud creates connected money laundering, terrorist financing, and proliferation-financing risks. That means effective fraud management must connect prevention and victim protection with suspicious-activity monitoring and broader financial crime escalation.

One of the central challenges in fraud management is balancing prevention, customer experience, and operational efficiency. Too little friction can make scams, account takeover, and payment fraud easier. Too much friction can block legitimate customers, increase abandonment, and create poor outcomes. The FCA has repeatedly stressed that firms should use new systems, processes, data, and approaches to keep up with financial crime risks, which implies fraud controls must be effective without becoming mechanically obstructive. The strongest fraud management frameworks are risk-based: they introduce stronger intervention where risk indicators are higher, while allowing low-risk legitimate activity to proceed smoothly.

Detection remains a major part of fraud management, but not the whole of it. A firm may detect suspicious behavior successfully and still have weak fraud management if investigations are inconsistent, response is slow, customer treatment is poor, or lessons are not fed back into the control environment. The FFIEC states that suspicious activity monitoring and reporting are critical internal controls and that institutions should have appropriate processes to monitor and identify unusual activity. In practical terms, that means fraud management depends not only on identifying alerts, but on having the operational capability to act on them effectively.

Data and intelligence are also fundamental. Strong fraud management relies on customer data, transaction data, device and access data, prior fraud outcomes, typology intelligence, and cross-functional information sharing. FCA materials on financial crime emphasize the importance of fraud data, and FATF’s digital transformation work points to the value of new technologies in improving detection efficiency and reducing ineffective alert noise. But better technology does not remove the need for strong governance. Poor-quality data, weak scenario ownership, or fragmented case handling can make an apparently sophisticated fraud programme perform badly in practice.

Ultimately, fraud management is the practical operating model through which firms protect customers, reduce losses, disrupt criminal activity, and prevent fraud from becoming wider financial crime. It is not only about catching fraud after the event. It is about building a control environment that anticipates fraud, detects it early, responds effectively, and improves continuously as criminal methods evolve. In a financial system shaped by digital channels, fast payments, identity abuse, and increasingly adaptive fraud typologies, effective fraud management is one of the clearest indicators of whether a firm’s wider financial crime framework is genuinely resilient.