The Financial Industry Regulatory Authority (FINRA) is the U.S. self-regulatory organization for member broker-dealers. FINRA says it is responsible under federal law for supervising its member firms, under SEC oversight, and that its mission is to protect investors and safeguard the integrity of U.S. capital markets.

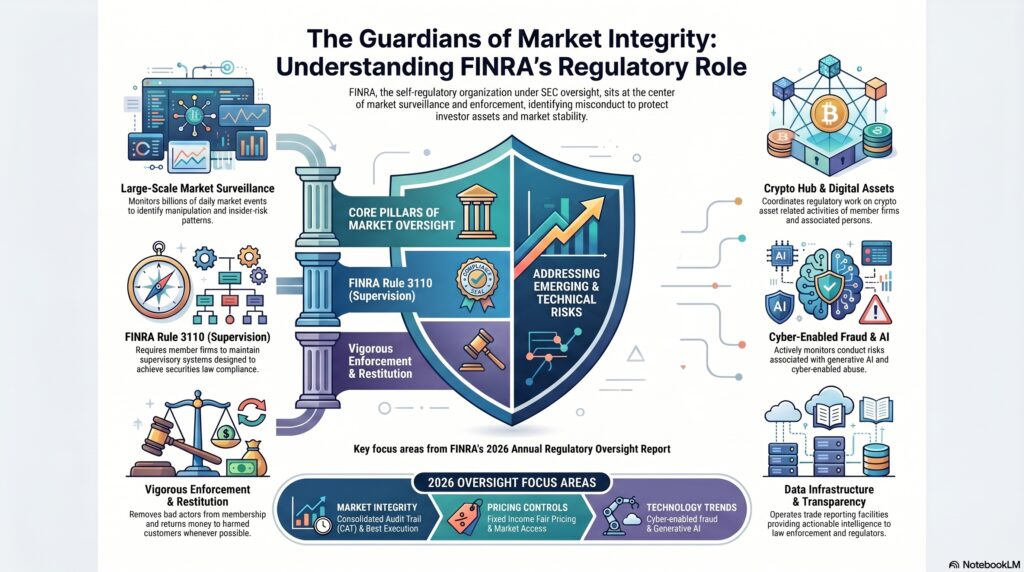

In the financial crime environment, FINRA is significant because it sits at the center of broker-dealer supervision, market surveillance, enforcement, licensing, and conduct oversight. It is not a bank AML regulator in the same way that FinCEN or the prudential banking agencies are, but it plays a major role in the detection and prevention of misconduct that overlaps with fraud, market abuse, books-and-records failures, weak supervision, sales-practice violations, and other conduct that can harm investors and undermine market integrity. FINRA states that it writes and enforces rules, examines member firms, identifies manipulation and other misconduct by monitoring billions of daily market events, and returns money to harmed customers whenever possible.

From a professional compliance perspective, FINRA is best understood as a markets and broker-dealer control authority. Its relevance to the financial crime environment comes through several channels. First, it supervises firms that sit close to customer assets, securities transactions, capital raising, and retail and institutional order flow. Second, it maintains surveillance and enforcement capabilities aimed at identifying manipulation, insider-risk patterns, communications failures, and other misconduct. Third, it imposes supervision, recordkeeping, and conduct obligations on member firms that directly affect how firms detect and escalate suspicious or abusive behavior. FINRA Rule 3110, for example, requires each member to establish and maintain a supervisory system reasonably designed to achieve compliance with securities laws, regulations, and FINRA rules.

Watch on YouTube: Financial Industry Regulatory Authority

A central reason FINRA matters in the financial crime environment is market integrity. FINRA’s public materials state that it identifies manipulation and other misconduct through large-scale market monitoring, and its 2026 Annual Regulatory Oversight Report includes a dedicated market integrity section covering areas such as the Consolidated Audit Trail, best execution, fixed income fair pricing, market access, and related controls. That means FINRA is not merely reacting to misconduct after the fact; it is actively shaping how firms build preventive and detective controls around trading, order handling, and client activity.

FINRA is also important because it has a strong enforcement function. FINRA says its enforcement work advances confidence in the securities markets through vigorous, fair, and effective enforcement of FINRA and MSRB rules and federal securities laws and rules, and that it acts quickly to identify misconduct, stop fraud, prevent losses, obtain restitution, and remove bad actors from FINRA membership where appropriate. In the financial crime environment, this matters because it gives FINRA a direct role in addressing fraud, weak supervision, recordkeeping failures, off-channel communication issues, sales abuses, and other misconduct that can have financial crime implications even where the issue is not framed as classic AML.

Another major element is surveillance and data infrastructure. FINRA states that it operates trade reporting facilities to provide transparency to market participants in fixed income and equity markets, and it also highlights an insider trading detection program that provides actionable intelligence to law enforcement and regulators. That combination of market-data infrastructure and surveillance capability makes FINRA a key participant in the broader evidential environment for detecting misconduct in U.S. securities markets. This is especially relevant where manipulative trading, insider dealing, or misleading market behavior overlap with broader financial crime concerns.

FINRA’s current oversight work also shows its role in emerging risks. The 2026 Annual Regulatory Oversight Report includes content on cyber-enabled fraud and trends in generative AI, while FINRA’s site highlights a crypto hub intended to coordinate its regulatory work on crypto asset-related activities of member firms and associated persons. In practical terms, this shows that FINRA’s financial crime relevance is not limited to legacy securities misconduct; it extends into new channels where cyber-enabled abuse, digital-asset exposure, and technology-related conduct risks can affect broker-dealers and investors.

A professionally mature firm therefore treats FINRA as more than a licensing and examinations body. It is a source of supervisory expectations for how broker-dealers should structure compliance, supervision, communications controls, books and records, sales practices, market access, and customer protection. FINRA’s Annual Regulatory Oversight Report is explicitly designed to help firms identify emerging risks and strengthen their compliance programs. That makes FINRA highly relevant to firms’ control design, testing, and remediation planning.

Ultimately, FINRA is significant in the financial crime environment because it helps govern one critical part of the U.S. securities industry through supervision, surveillance, enforcement, transparency infrastructure, and investor-protection standards. It does not replace the SEC or FinCEN, but it is a central authority in shaping how broker-dealers detect, prevent, and respond to misconduct that threatens investors and market integrity.