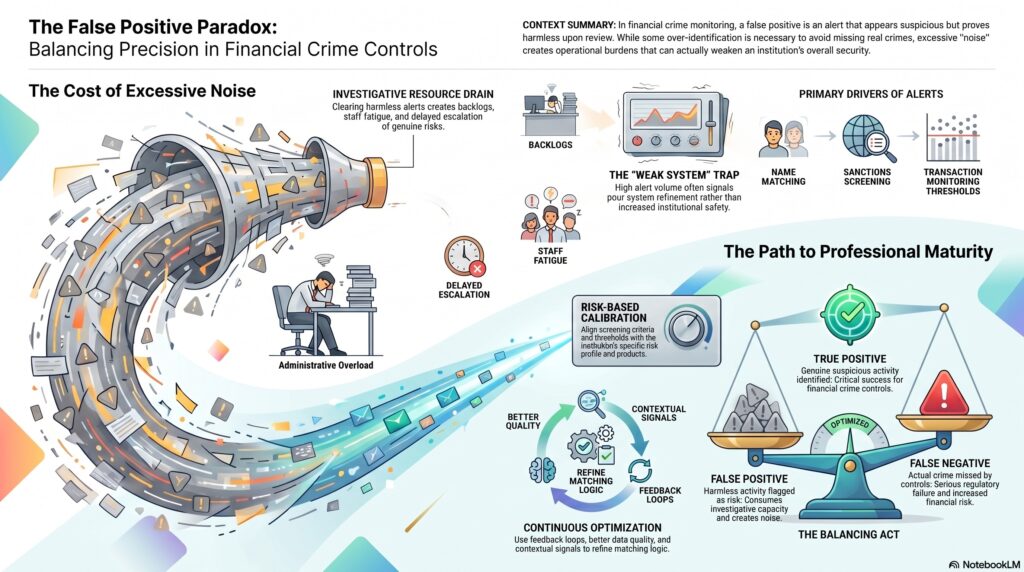

A false positive is an alert, match, or detection outcome that appears to indicate financial crime risk but, after review, turns out not to represent genuine suspicious, prohibited, or criminal activity. In the financial crime environment, false positives most commonly arise in sanctions screening, transaction monitoring, fraud detection, adverse media screening, and name matching. FATF’s digital-transformation work notes that new technologies can help reduce the number of false positives, and the FCA’s updated Financial Crime Guide materials refer directly to the proportion of false positives as part of transaction-monitoring implementation and calibration.

From a professional perspective, false positives are not merely a technical inconvenience. They are a core control-quality issue. Every financial crime monitoring framework is designed to identify potential risk, which means some over-identification is inevitable. A system that never produces false positives is usually one that is too weak to detect much at all. The problem arises when alert volumes become so noisy that investigators cannot distinguish meaningful cases from harmless activity, or when the institution uses broad screening logic that captures too many irrelevant matches. FATF explicitly notes that reducing false positives can make AML/CFT compliance timelier and less burdensome, which reflects the wider point that alert quality matters as much as alert quantity.

In practical terms, false positives are especially visible in name screening and sanctions controls. A customer or counterparty may have a name similar to a sanctioned person, appear to match a watchlist entry, or trigger a possible hit because of transliteration, spelling variation, or incomplete identifiers. The FFIEC’s OFAC manual states that a high volume of false hits may indicate a need to review the bank’s interdiction program and that screening criteria should be based on the level of OFAC risk associated with the product or transaction. In other words, a high false-positive rate is often a sign that the screening framework needs refinement, not that the institution is safer.

Watch on YouTube: False Positive

False positives are also a major issue in transaction monitoring. A transaction may breach a rule threshold, match a scenario, or look unusual compared with generic norms, yet still be entirely explainable when considered in the context of the customer profile, account purpose, or commercial activity. The FCA’s current guidance work on transaction monitoring specifically refers to calibration and to the proportion of false positives, including examples where threshold-based systems are poorly calibrated. That is important because a transaction-monitoring system that generates excessive low-value alerts may overwhelm investigators and reduce the institution’s ability to identify the genuinely higher-risk activity that matters most.

From a governance standpoint, false positives matter because they consume investigative capacity. Every false positive requires some level of review, triage, or disposition. If alert quality is poor, analysts spend large amounts of time clearing activity that poses no real risk, and that can create backlogs, inconsistent decision-making, staff fatigue, and delayed escalation of genuine suspicious activity. FATF’s digital-transformation work and executive summary both note that reducing false positives helps analysts focus on more relevant cases and reduces the noise in the system.

A professionally mature firm therefore does not try to eliminate false positives completely. Instead, it manages them through better calibration, data quality, segmentation, and feedback loops. This may include improving customer data, refining matching logic, introducing risk-based thresholds, using contextual signals, separating higher-risk and lower-risk activity, and learning from prior alert dispositions. The FCA’s guidance and consultation materials on transaction monitoring are aligned with this approach, emphasizing implementation, monitoring, and responsible calibration rather than simply increasing sensitivity.

False positives also need to be distinguished from false negatives. A false positive is an alert that proves harmless. A false negative is the more serious failure where genuinely suspicious or prohibited activity is missed entirely. In practice, firms are constantly balancing these two risks. If thresholds are too loose or screening logic too broad, false positives rise. If thresholds are too narrow or controls too permissive, false negatives may increase. Effective financial crime control therefore depends on finding a defensible balance that reflects the firm’s risk profile, legal obligations, products, customers, and available investigative resources. This is an inference supported by the FCA’s emphasis on risk-based calibration and by FFIEC guidance that screening criteria should reflect OFAC risk.

Ultimately, a false positive is not just an incorrect alert. It is a signal about the quality of the detection framework itself. Some false positives are unavoidable and even necessary in any credible control environment, but excessive or poorly managed false positives can weaken detection effectiveness, consume resources, and reduce confidence in the monitoring system. For that reason, false positives should be treated as a central performance metric in financial crime controls, especially in sanctions screening, transaction monitoring, and fraud detection.