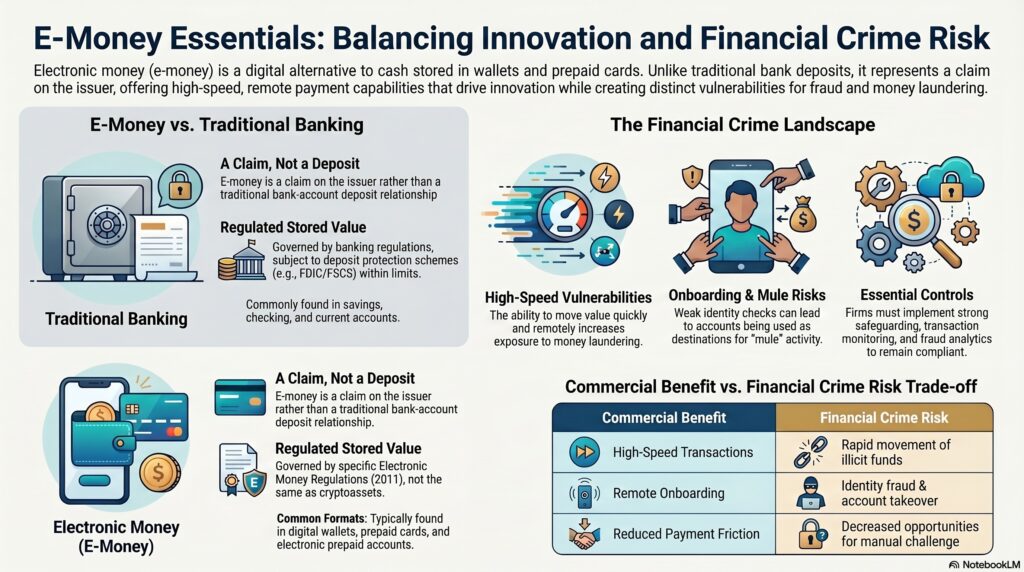

Electronic money, or e-money, is electronically stored monetary value that is issued on receipt of funds and used to make payment transactions. Under the FCA’s current UK regulatory framing, e-money is electronically, including magnetically, stored monetary value represented by a claim on the issuer, issued on receipt of funds for the purpose of making payment transactions, and accepted by a person other than the issuer. The European Commission similarly describes e-money as a digital alternative to cash.

In the financial crime environment, e-money is important because it combines the functionality of digital payments with a specific legal and regulatory structure. It is not the same as a bank deposit, and it is not the same as a cryptoasset. E-money usually sits within prepaid cards, digital wallets, electronic prepaid accounts, and similar stored-value arrangements that can be used for purchases, transfers, or other payment activity. The FCA’s current approach materials and the Electronic Money Directive framework both treat e-money as a regulated form of monetary value designed to support payments innovation while remaining subject to prudential and conduct safeguards.

From a professional financial crime perspective, the significance of e-money lies in its ability to move and store value quickly, remotely, and at scale. Those features make e-money commercially useful, but they can also create exposure to fraud, mule activity, money laundering, sanctions evasion, and account misuse if controls are weak. A prepaid or wallet-based product may allow customers to receive, hold, and spend funds with less friction than traditional banking, which is beneficial for convenience and inclusion, but it can also reduce the points at which firms gather information, apply challenge, or identify suspicious use. This is an inference supported by the regulatory aim to facilitate innovative e-money services while supervising issuers under the Electronic Money Regulations and EU framework.

Watch on YouTube: Electronic Money (E-Money)

A key professional distinction is that e-money is a claim on the issuer rather than a deposit held in a traditional bank-account relationship. That distinction matters because it affects the prudential and safeguarding framework, as well as customer expectations about how funds are held and protected. The FCA’s electronic money pages and approach document make clear that e-money is regulated under the Electronic Money Regulations 2011 and that e-money firms are subject to safeguarding and conduct obligations. More recently, the FCA finalized changes to the safeguarding regime for payments and e-money firms in August 2025, which underlines that the area remains live and supervisory expectations continue to develop.

In the financial crime environment, the main risks associated with e-money often resemble those found in other payment products but are shaped by the product design. If onboarding is weak, an e-money account or wallet may be obtained under false pretences or used as a mule destination. If funding and withdrawal controls are weak, the product can be used to pass funds through quickly. If device or account security is weak, the product may be abused through account takeover, credential compromise, or scam-induced transfers. Because e-money products often operate digitally and at high speed, firms need strong customer due diligence, transaction monitoring, fraud analytics, and safeguarding controls to reduce those risks. This is an inference drawn from the nature of e-money as a digital payment instrument and the FCA’s emphasis on risk management for e-money firms.

E-money is also relevant because it sits close to wider questions of financial inclusion and innovation. The European Commission states that e-money rules are intended to support innovative and secure e-money services, encourage competition, and provide new companies with access to the market. In practical terms, that means regulators are trying to balance innovation and competition with financial crime control and customer protection. This balance is one reason the regulatory framework is precise about what e-money is and who can issue it.

For firms operating in this space, effective financial crime control depends on understanding both the legal classification and the operational behavior of the product. A firm needs to know whether it is issuing e-money, providing payment services around e-money, or doing both, because the regulatory perimeter and control expectations may differ. The FCA’s current approach document is designed specifically to help businesses navigate the Payment Services Regulations 2017 and the Electronic Money Regulations 2011 and understand how the FCA interprets the regime.

Ultimately, electronic money is significant in the financial crime environment because it represents a regulated digital store of value that can support fast, convenient payments outside a traditional deposit-account structure. Its legitimate role in payments innovation does not reduce the need for strong control. On the contrary, because e-money products can move and store funds quickly and remotely, they require clear customer understanding, strong safeguarding, effective fraud prevention, and robust AML controls. For that reason, e-money should be understood not just as a payments innovation concept, but as a distinct and important part of the modern financial crime control landscape.