Customer fraud is fraud committed against, through, or in some cases by a customer relationship, depending on the context in which the term is used. The phrase is not always applied consistently across firms. NICE Actimize’s glossary uses “customer fraud” to describe situations where fraudsters pose as customers and deceive a business, while the FCA frames fraud more broadly as part of the financial crime risks firms must prevent and manage. Because of that variation, firms should define the term clearly in their own taxonomy rather than assume a single industry meaning.

In the financial crime environment, the most useful professional meaning of customer fraud is fraud that targets or exploits the customer relationship itself. This can include identity theft, account takeover, authorized push payment scams, card fraud, application fraud, social-engineering fraud, and other typologies where the customer is either the victim, the impersonated party, or the channel through which the fraud is executed. It can also overlap with first-party misconduct where a real customer abuses a product or disputes a legitimate obligation dishonestly, though many firms would classify that more precisely as first-party fraud rather than customer fraud. This need for clearer classification follows from the broader FCA view that fraud sits within financial crime and from the inconsistent glossary usage seen in industry sources.

From a professional risk perspective, customer fraud matters because the customer relationship is one of the most trusted points in the financial system. Firms design onboarding, authentication, servicing, payments, and support processes on the assumption that the customer identity is genuine, that the person interacting with the institution is authorized, and that customer instructions are legitimate unless there is reason to doubt them. Fraud exploits that trust. A criminal may impersonate a customer, manipulate a customer into authorizing a payment, take over the customer’s account, or use stolen customer data to obtain products and services. Once the customer relationship is compromised, downstream controls can become less reliable because the activity may still appear to come from a genuine account or identity. This is an inference supported by the FCA’s treatment of fraud as a core financial crime issue for regulated firms.

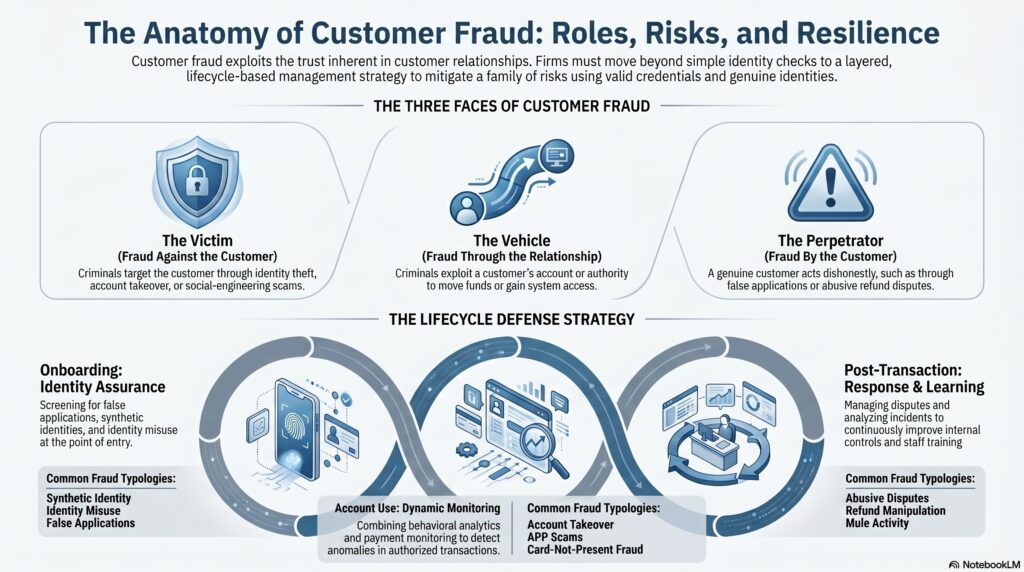

One reason customer fraud is such a broad and important category is that it spans multiple stages of the customer lifecycle. At onboarding, fraud may appear as false applications, identity misuse, or synthetic identity abuse. During account use, it may appear as account takeover, card-not-present fraud, payment fraud, or scam-induced transfers. After a transaction, it may surface through abusive disputes, refund manipulation, or other forms of post-transaction deception. In this sense, customer fraud is not one single typology. It is a family of typologies linked by the fact that the customer relationship is central to how the fraud is carried out or experienced. This is consistent with industry glossary treatment of customer fraud and with the FCA’s wider framing of fraud risks across firms’ customer-facing activities.

Watch on YouTube: Customer Fraud

In practical terms, customer fraud usually takes one of three broad forms. The first is fraud against the customer, where the customer is the victim, such as in impersonation scams, account takeover, or misuse of stolen card data. The second is fraud through the customer relationship, where criminals exploit the customer account, identity, or payment authority to move funds or obtain access. The third is fraud by the customer, where a genuine customer behaves dishonestly, for example through false applications or abusive disputes. Not every firm will use the term customer fraud for all three categories, but this framework is often useful because it shows how the customer can be victim, vehicle, or perpetrator. That last point is an inference based on the different definitions and related fraud categories shown in the searched sources.

This broadness is exactly why customer fraud has strong links to other financial crime disciplines. It overlaps with fraud prevention, AML, identity assurance, sanctions controls, and customer protection. A customer who is deceived into sending money may become the source of an APP fraud loss. A compromised customer account may become a mule conduit for suspicious payments. A falsified customer application may expose the institution to both fraud loss and AML weakness. The FCA’s financial crime materials explicitly place fraud within the broader financial crime framework and identify firms as a vital line of defence against criminal misuse of financial services.

From a controls perspective, customer fraud is especially challenging because it often involves valid-looking identities and instructions. A fraudster may use correct credentials, genuine customer data, or apparently normal servicing channels. A scam victim may authorize a transaction themselves. A dishonest customer may use their own identity and account while still acting fraudulently. This means that customer fraud cannot be managed through identity checks alone. Institutions need layered controls that combine identity verification, behavioral monitoring, payment analytics, account-security measures, staff training, and customer communications. The FCA’s fraud page specifically points firms toward the Financial Crime Guide and its risk-based payments guidance, reflecting the expectation that fraud controls be tailored to the way firms and customers actually interact.

Customer fraud also has a strong customer-outcomes dimension. When fraud is committed against customers, the harm is not limited to immediate financial loss. It can involve emotional distress, service disruption, loss of trust, denial of legitimate access, and difficulty recovering from identity misuse or unauthorized activity. The FCA’s consumer-facing material on rights with financial services and its wider fraud work reflect the importance of protecting customers and addressing financial harm. In a professional financial crime framework, this means customer fraud should not be treated solely as a loss-prevention issue; it is also a customer-protection issue.

A mature institution therefore manages customer fraud through a lifecycle approach. It assesses fraud risk at onboarding, protects account access and customer data during the relationship, monitors behavior and transactions dynamically, responds quickly to suspicious events, and learns from incidents to improve controls. It also distinguishes clearly between external impersonation, internal account misuse, and first-party dishonest conduct, because each requires a different control response. This is an inference based on the broad risk areas covered by the FCA’s financial crime guidance and the industry definition of customer fraud.

Ultimately, customer fraud is best understood as fraud that exploits the customer relationship as the point of attack, deception, or misuse. It is significant in the financial crime environment because the customer relationship is one of the main channels through which trust enters the financial system. When that trust is manipulated, firms can face fraud losses, AML exposure, conduct issues, and serious customer harm. For that reason, customer fraud should be treated as a core part of the wider financial crime framework, with clear taxonomy, strong controls, and close integration between fraud, customer protection, and compliance functions.