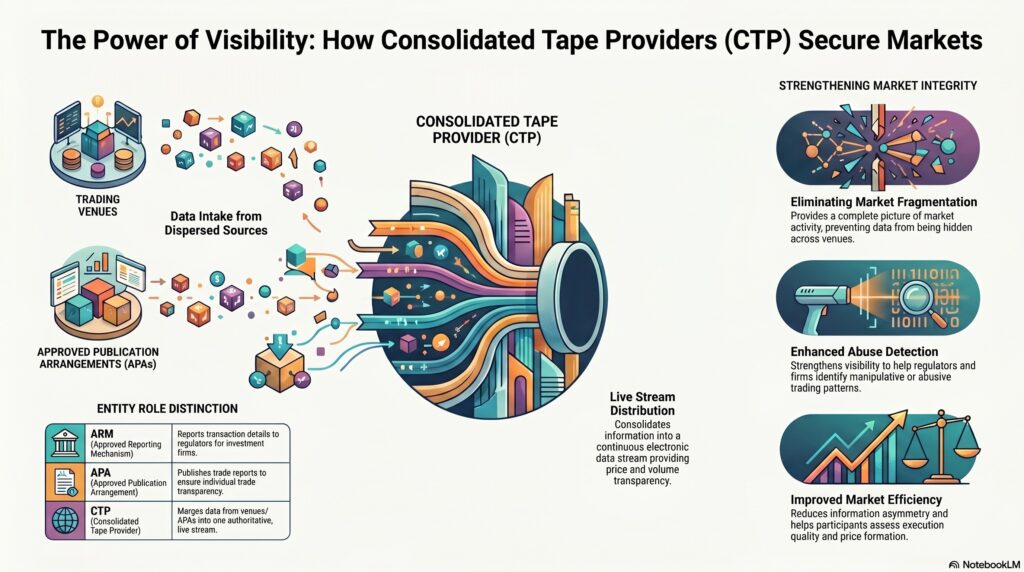

A Consolidated Tape Provider (CTP) is a regulated data reporting services provider that collects post-trade market data from trading venues and approved publication arrangements, consolidates that information, and distributes it as a continuous electronic data stream. MiFIR defines a CTP as a person authorised to collect data from trading venues and APAs and consolidate those data into a continuous electronic live data stream providing core market data and regulatory data. The FCA uses similar language and describes CTPs as providers that collect post-trade transparency reports from venues and APAs and consolidate them into a live data stream showing price and volume information per financial instrument.

In the financial crime environment, a CTP is important not because it performs customer due diligence or AML screening directly, but because it supports market transparency, surveillance, and integrity. ESMA states that consolidated tapes are intended to provide a continuous electronic live stream of market data, while the FCA explains that data reporting service providers play a key role in market transparency and integrity. That makes the CTP part of the data infrastructure that helps firms, regulators, and market participants understand what has traded, where, and at what price and volume.

From a professional compliance and market-conduct perspective, the significance of a CTP lies in the fact that fragmented post-trade data can weaken visibility across markets. If trade information is dispersed across multiple venues and publication mechanisms, it becomes harder to form a complete picture of market activity, compare execution quality, or identify unusual trading patterns across venues. The European Commission has stated that a consolidated tape is intended to provide consolidated data on prices and volumes across EU trading venues in order to improve price transparency, and the FCA has similarly described the CT as a single, authoritative, complete, and affordable source of market data.

Watch on YouTube: Consolidated Tape Provider

That transparency function matters in the financial crime environment because market abuse, manipulation, and other misconduct often become more difficult to detect when information is fragmented. A CTP does not replace trade surveillance systems or regulator-led investigations, but it can strengthen the underlying visibility on which those functions depend. Better consolidated post-trade data can support execution analysis, price formation review, and broader market monitoring. This is an inference from the stated transparency and market-integrity objectives of the consolidated tape framework.

A key professional distinction is that a CTP is not the same as an Approved Reporting Mechanism or an Approved Publication Arrangement. An ARM reports transaction details to regulators on behalf of investment firms. An APA publishes trade reports for transparency purposes. A CTP then draws in post-trade data from venues and APAs and consolidates it into a single stream. The FCA’s own description of data reporting service providers separates these functions clearly.

In current EU and UK market-structure discussions, the consolidated tape is also viewed as a way to improve market efficiency and reduce information asymmetry. The FCA has said that a consolidated tape should make it easier for market participants to access a consolidated view of trade transparency information, and in its bond CT materials it explains that the tape will collate data such as trade prices and volumes to provide a comprehensive picture of bond transactions, including trades executed on venues and over the counter.

This gives the CTP a meaningful, though indirect, role in the financial crime environment. It supports the evidential and transparency layer of market oversight rather than the customer-risk layer. In practice, stronger post-trade transparency can help firms assess best execution, help regulators and surveillance functions understand trading behaviour, and reduce the opacity in which manipulative or abusive activity can be harder to identify. That is an inference based on the consolidated tape’s stated purpose of improving transparency and market visibility.

The framework is also very much current rather than theoretical. ESMA states that MiFIR provides the legislative framework for CTPs and that ESMA has a role in selecting them, while FCA materials describe the UK bond consolidated tape framework and outline steps for appointing a provider. ESMA also launched the selection of a consolidated tape provider for OTC derivatives in January 2026, which shows the regime is actively developing.

Ultimately, a Consolidated Tape Provider is important in the financial crime environment because it helps create a more complete and transparent picture of post-trade market activity. It does not itself investigate fraud or market abuse, but it strengthens the data foundation on which market surveillance, execution analysis, regulatory oversight, and integrity controls depend. In that sense, the CTP should be understood as a market-transparency infrastructure function with real relevance to the broader control environment.