Conflicts of interest arise where a person, firm, or function has competing interests that could impair objective judgment, influence decision-making, or create incentives to act in a way that is inconsistent with the interests of customers, market integrity, or regulatory obligations. In regulated financial services, the concept is well established. The FCA’s SYSC rules require firms to take all appropriate steps to identify and prevent or manage conflicts of interest, and MiFID II requires investment firms to maintain effective arrangements to prevent conflicts from adversely affecting clients’ interests.

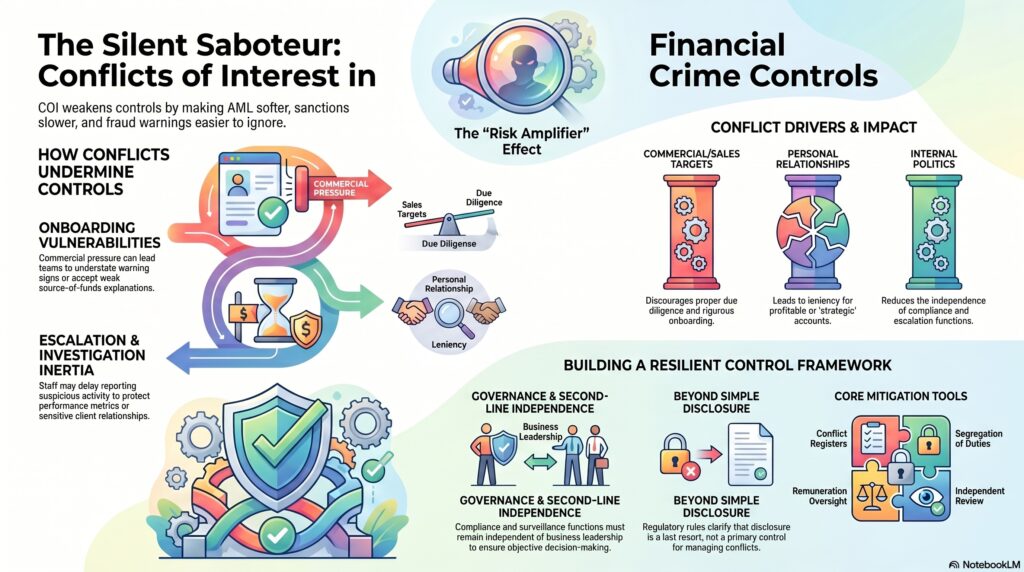

In the financial crime environment, conflicts of interest are especially important because they can weaken controls without appearing at first to be a financial crime issue. A firm may have AML, sanctions, fraud, and market abuse policies in place, yet those controls can be undermined if commercial incentives, personal relationships, remuneration structures, client-pressure dynamics, or internal politics distort how decisions are made. A profitable customer may be treated too leniently. A suspicious transaction may not be escalated promptly. A sanctions concern may be rationalized away. A market abuse alert may receive weak challenge because of revenue pressure or relationship sensitivity. In that sense, conflicts of interest are often an underlying cause of financial crime control failure rather than a separate or purely ethical topic. This is an inference supported by the FCA and ESMA emphasis on conflicts arrangements as part of broader conduct and client-protection frameworks.

A professionally mature understanding of conflicts of interest goes beyond obvious personal corruption. The risk does not arise only where an employee receives a bribe or has a hidden side arrangement. Conflicts can be structural and entirely internal to the business model. For example, sales targets may discourage proper due diligence. Relationship managers may resist exiting higher-risk customers. Trading incentives may encourage behavior that is misaligned with fair client outcomes. Surveillance or compliance functions may lack independence where business leadership influences resourcing or escalation decisions. The FCA’s guidance makes clear that conflicts can arise between a firm and its clients, between different clients, or between staff and the firm’s obligations, which is directly relevant to financial crime governance.

Watch on YouTube: Conflicts of Interest

In the financial crime environment, conflicts of interest are particularly relevant at onboarding. Customer acceptance decisions are often commercially sensitive, especially for higher-value relationships or strategic accounts. That creates a risk that business teams understate warning signs, accept weak explanations for source of funds or ownership structures, or pressure control functions to approve a relationship that should receive deeper scrutiny. If this occurs, the institution may onboard a customer whose financial crime risk was visible but not acted upon because commercial interests conflicted with control expectations. FATF’s risk-based approach expects firms to identify and mitigate higher-risk relationships proportionately, which becomes difficult if conflicted incentives interfere with objective assessment.

Conflicts of interest are also critical in investigations and escalation. A financial crime framework depends on timely challenge, independent review, and willingness to escalate concerns even where doing so may inconvenience clients or reduce revenue. Where staff fear that escalation will damage performance metrics, internal standing, or client relationships, suspicious matters may be minimized or delayed. This is one reason governance and second-line independence matter so much. The FCA’s systems-and-controls framework places emphasis on effective governance, independent oversight, and clear allocation of responsibility, all of which help reduce the risk that conflicted judgment undermines compliance outcomes.

In markets businesses, conflicts of interest have an additional market-integrity dimension. Order handling, execution, research, corporate relationships, personal account dealing, allocation decisions, and communication of information can all be affected by conflicting incentives. ESMA’s investor-protection and market-integrity materials reflect the expectation that firms identify and manage these risks properly. In practice, unmanaged conflicts can contribute to poor client outcomes, weak best execution, selective information handling, and increased market abuse exposure. This does not mean every conflict becomes misconduct, but it does mean the firm’s financial crime and conduct framework is less reliable where conflicts are not controlled.

A mature control framework therefore treats conflicts of interest as a governance risk that must be identified, documented, mitigated, and monitored. This usually includes a conflicts policy, registers of actual and potential conflicts, disclosure standards where appropriate, segregation of duties, independent review, restricted lists, remuneration oversight, personal account dealing controls, gift and hospitality rules, and escalation channels where staff believe judgment may be compromised. FCA rules also make clear that disclosure alone is not enough if the firm cannot be reasonably confident that arrangements prevent damage to client interests; disclosure is a last resort rather than the primary control.

The financial crime relevance becomes clearest when conflicts are viewed as a risk amplifier. Weak incentives can make AML controls softer, sanctions decisions slower, fraud warnings easier to ignore, and surveillance outcomes less independent. Strong controls on paper are not enough if the people applying them have incentives to avoid uncomfortable decisions. For that reason, conflicts of interest should be understood as a core part of the control environment, not as a narrow legal disclosure topic. They shape whether the institution can make objective, defensible decisions when financial crime risk collides with commercial pressure. This is an inference from the cited regulatory frameworks on conflicts, governance, and risk-based control design.

Ultimately, conflicts of interest matter in the financial crime environment because they can silently distort judgment at the exact points where objectivity is most needed: onboarding, escalation, surveillance, investigations, client treatment, and market conduct. If unmanaged, they weaken control credibility and increase the likelihood that financial crime risk is tolerated, misunderstood, or concealed. For that reason, effective conflicts management is an essential part of a resilient compliance and financial crime framework.