Compliance risk is the risk that a firm’s activities, controls, decisions, or conduct fail to meet applicable laws, regulations, regulatory expectations, internal policies, or ethical standards, and that this failure causes legal, regulatory, financial, operational, or reputational harm. The OCC defines compliance risk as the risk to current or projected financial condition and resilience arising from violations of laws or regulations, or from nonconformance with prescribed practices, internal policies and procedures, or ethical standards. In the financial crime environment, this risk is especially important because failures in compliance can expose an institution to money laundering, sanctions breaches, fraud losses, market abuse, enforcement action, remediation costs, and loss of trust.

From a professional financial crime perspective, compliance risk is not limited to the possibility of a rule being broken in a technical sense. It is broader than that. It includes the risk that a firm misunderstands its obligations, designs weak controls, applies them inconsistently, fails to escalate concerns, or cannot evidence that it is managing financial crime risk in a proportionate and defensible way. The FCA’s Financial Crime Guide emphasizes that firms should establish and maintain effective systems and controls to counter the risk that they might be used to further financial crime, while FATF’s risk-based approach guidance expects firms to identify, assess, understand, and mitigate money laundering and terrorist financing risks proportionately.

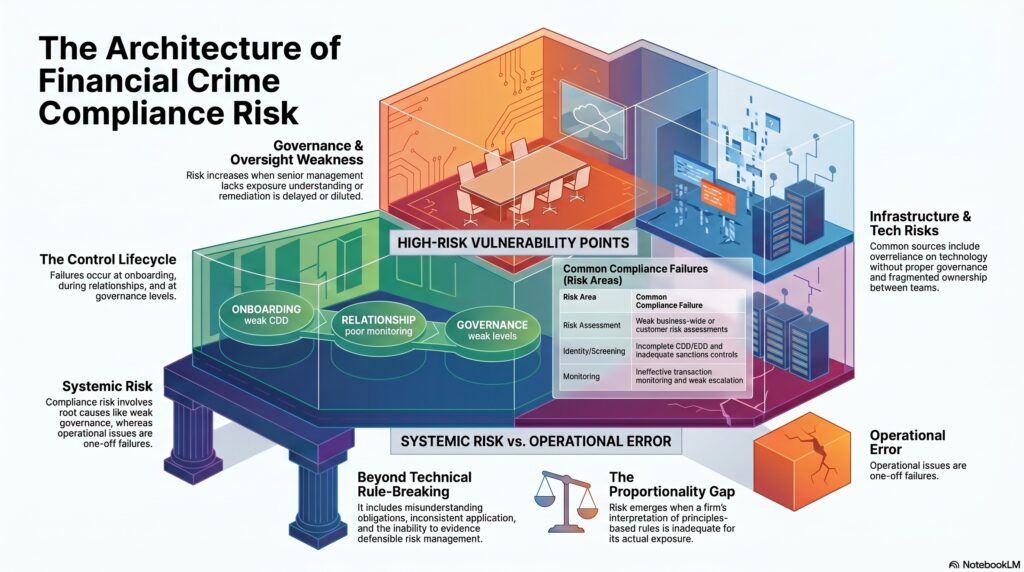

In the financial crime environment, compliance risk arises across the full control lifecycle. It can emerge at onboarding if customer due diligence is incomplete, if beneficial ownership is misunderstood, or if sanctions screening is weak. It can arise during the life of the relationship if transaction monitoring is ineffective, if suspicious activity is poorly investigated, or if customer risk ratings are not updated when circumstances change. It can also arise at governance level if management information is poor, if accountability is unclear, if training is inadequate, or if known weaknesses are allowed to persist without remediation. This means compliance risk is not confined to isolated errors. It often reflects structural weakness in how the institution interprets obligations and embeds controls.

Watch on YouTube: Compliance Risk

A key feature of compliance risk is that it sits between regulatory obligation and practical execution. Financial crime rules and expectations are often principles-based or risk-based rather than purely mechanical. Firms are not simply told to apply one fixed control in every circumstance. They are expected to understand their business model, identify where risk is highest, and build controls that are proportionate to that risk. FATF’s guidance for the banking sector makes this explicit, and the FCA’s financial crime materials reflect the same approach. This means compliance risk often emerges not because a rule was ignored entirely, but because the firm’s interpretation, calibration, or implementation of that rule was inadequate for its actual exposure.

This is why compliance risk should be distinguished from pure operational error. An operational issue may involve a one-off failure in processing or execution. Compliance risk is broader and more systemic. It concerns whether the firm’s control framework is capable of meeting the standard expected of it. A missed sanctions alert, for example, may be an operational failure. But if the root cause is weak screening governance, poor data quality, inadequate escalation, or ineffective testing, then the real issue is compliance risk. In the financial crime environment, many serious regulatory outcomes arise not from one incident alone, but from a pattern of weak compliance design, weak oversight, or weak challenge over time. This is an inference based on the regulatory focus on systems and controls rather than isolated mistakes.

Compliance risk is also highly connected to governance. A firm may have policies, systems, and committees, but still carry substantial compliance risk if senior management does not understand the firm’s exposure, if the second line lacks authority, or if remediation is delayed or diluted. The FCA’s guidance repeatedly points to governance, oversight, training, monitoring, and management information as key parts of a sound financial crime control framework. In professional terms, this means compliance risk is as much about decision-making quality and accountability as it is about technical rule interpretation.

In practical financial crime terms, common sources of compliance risk include weak business-wide risk assessments, poor customer risk assessments, incomplete CDD and EDD, inadequate sanctions controls, ineffective transaction monitoring, weak suspicious activity escalation, poor screening data, insufficient training, fragmented ownership between business and compliance teams, and overreliance on technology without proper governance. The FCA’s recent findings on firms’ risk assessment processes emphasize how important it is that firms identify, understand, assess, and mitigate risk effectively. Although those findings are broader than one control area, they directly reinforce the point that poor risk assessment itself is a major source of compliance risk.

A mature institution manages compliance risk through a combination of risk assessment, policy design, oversight, testing, training, escalation, and remediation. The objective is not to eliminate every possible breach, which is unrealistic, but to maintain a control environment that is proportionate, evidence-based, and capable of responding when issues arise. FATF’s risk-based approach supports this model by emphasizing that controls should be matched to the nature and level of risk rather than applied blindly or uniformly. In the financial crime environment, this approach is essential because products, customers, geographies, and criminal typologies vary too widely for compliance to be managed credibly through generic controls alone.

Ultimately, compliance risk is a core concept in the financial crime environment because it captures the danger that a firm’s framework for meeting legal and regulatory obligations is weaker than it appears. When that happens, the institution may be exposed not only to enforcement and financial penalties, but also to actual misuse by money launderers, fraudsters, sanctioned parties, or other bad actors. For that reason, compliance risk should be understood not as a narrow legal concern, but as a strategic control risk that affects the credibility, resilience, and integrity of the entire financial crime framework.