The term “citizen fraudster” is not a formal regulatory category in the way that terms such as money mule, politically exposed person, or beneficial owner are. It appears instead as an industry phrase, and its meaning is used inconsistently across glossaries and commentary. In one usage, it refers to an otherwise ordinary individual who opportunistically commits fraud when the opportunity seems easy and the perceived consequences seem low. In another usage, it refers more narrowly to a person who commits fraud against public-sector or government programmes. Because of that inconsistency, firms should use the term carefully and define it explicitly if they include it in policy, training, or typology libraries.

In the financial crime environment, the more useful interpretation is the first one: a person who is not necessarily part of an organized professional fraud network, but who engages in fraud opportunistically using their own identity, genuine customer relationship, or access to a legitimate process. NICE Actimize’s glossary defines a citizen fraudster as an individual who may not have engaged in criminality until the right circumstances and the possibility of easy funds arose, and industry commentary has used the phrase to distinguish opportunistic fraudsters from organized fraud rings.

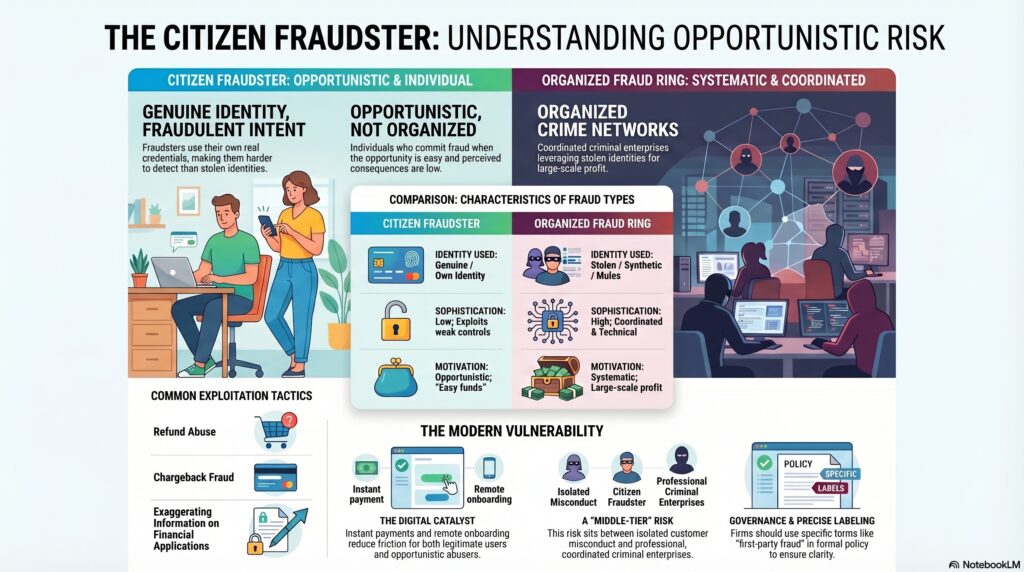

From a professional financial crime perspective, this matters because it captures a type of fraud risk that sits between isolated customer misconduct and organized criminal enterprise. A citizen fraudster may be a genuine customer who exaggerates information on an application, abuses a refund or chargeback process, misuses a financial hardship scheme, participates in first-party fraud, opens an account for opportunistic misuse, or assists with fraud because the barrier to entry appears low. The key feature is not sophistication, but willingness to exploit a system that appears vulnerable. That interpretation is consistent with the way industry sources contrast “citizen fraudsters” with fraud rings and organized cybercriminals.

Watch on YouTube: Citizen Fraudster

This concept is especially relevant in modern digital financial services because easier onboarding, remote servicing, instant payments, self-service changes, and online refund or dispute mechanisms can reduce friction for both legitimate users and opportunistic abusers. Industry commentary has linked the rise of the so-called citizen fraudster to digitization and easier access to online channels. In practical terms, that means firms may face fraudulent behavior not only from external attackers or coordinated networks, but also from ordinary users who exploit weak controls, low-verification journeys, or generous reimbursement processes.

In control terms, the citizen fraudster concept is closely related to first-party fraud, friendly fraud, and some forms of application fraud and chargeback abuse. The individual often uses real credentials, a real identity, or a real customer relationship, which makes detection harder than in classic third-party impersonation fraud. The problem is not that the customer is fictitious, but that the conduct is dishonest. That is why firms that rely too heavily on identity validation alone may miss this type of risk: the identity can be genuine while the intent is fraudulent. This is partly an inference from the industry definition of the term as opportunistic fraud by ordinary individuals rather than organized criminals.

There is also a second, narrower usage that appears in at least one financial crime glossary: a citizen fraudster as a person committing fraud against government agencies or public programmes. That usage is not the dominant one in the broader payments and fraud commentary I found, but it is relevant because it shows the term lacks a settled industry meaning. Where public-sector fraud is the subject, it is usually clearer to use more precise language such as benefits fraud, tax fraud, public-sector fraud, or government programme fraud rather than relying on “citizen fraudster.”

For governance purposes, the main lesson is that institutions should avoid treating “citizen fraudster” as a technical or universally understood label. If the term is used internally, it should be anchored to a defined typology such as opportunistic first-party fraud by genuine customers or applicants. That allows firms to build clearer controls around customer behavior, refund abuse, dispute misuse, promotional abuse, application misrepresentation, and low-level mule participation, rather than relying on a phrase that can mean different things to different teams. The inconsistent glossary usage itself is the strongest reason for this caution.

Ultimately, citizen fraudster is best treated as an informal industry expression for an ordinary individual who commits fraud opportunistically, usually outside the structure of a professional fraud ring. In the financial crime environment, the term is useful only if it helps firms recognize that meaningful fraud risk can come from genuine users exploiting weak controls, not just from organized external criminals. But because the term is not standardized and is used inconsistently, more precise labels are usually better in formal compliance, risk, and policy documents.