Business Email Compromise, commonly referred to as BEC, is a fraud typology in which criminals use deceptive or compromised business communications to induce the transfer of funds, the diversion of payments, or the disclosure of sensitive information. The FBI describes BEC as one of the most financially damaging online crimes, and its recent public materials explain that it is frequently carried out through social engineering or computer intrusion involving legitimate business or personal email accounts. Europol likewise describes BEC as a fraud type in which criminals impersonate company executives or employees to trick victims into transferring funds or revealing sensitive information.

In the financial crime environment, BEC is significant because it sits at the intersection of fraud, cyber-enabled crime, payments abuse, and money laundering. It is not merely an email scam. It is a mechanism for converting trust in business communications into the movement of money. A criminal does not always need to penetrate a bank or defeat payment authentication directly; instead, they manipulate the human and operational processes around invoice approval, vendor management, executive instruction, payroll, legal settlements, or treasury operations. Once the payment is made, the funds are often routed through mule accounts or layered onward, making BEC both a fraud event and a laundering-enablement event. Europol and the FBI both frame BEC as a socially engineered fraud with significant downstream financial consequences.

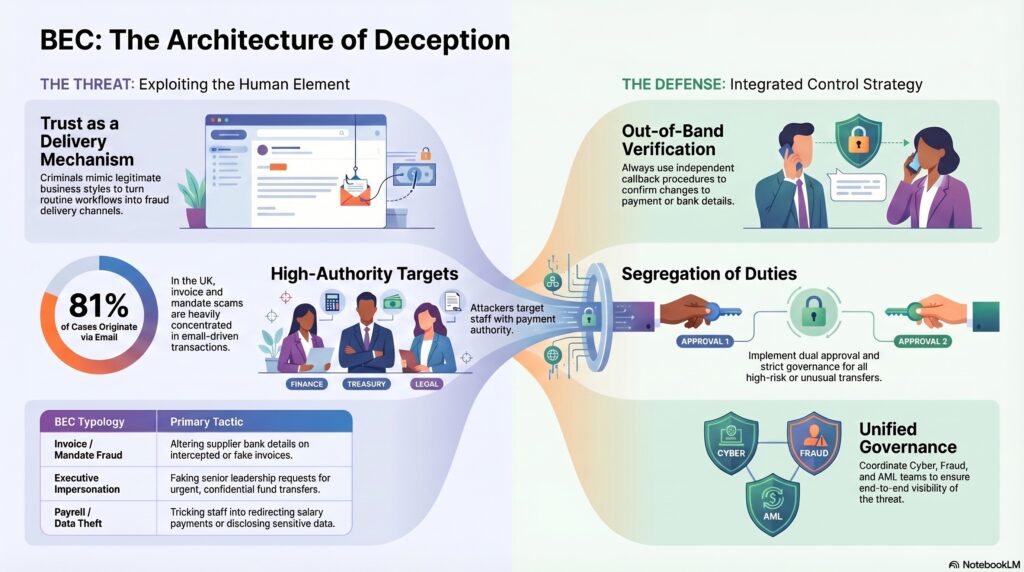

A defining feature of BEC is that the communication often appears legitimate. The attacker may spoof an email address, compromise a genuine mailbox, mimic writing style, hijack an existing email thread, or pose as a trusted executive, supplier, lawyer, or business partner. The FBI notes that BEC exploits the fact that businesses and individuals rely heavily on email for routine transactions, while its spoofing and phishing guidance explains how criminals disguise sender identity to appear trusted. This means the fraud succeeds not because the instruction looks obviously suspicious, but because it fits naturally into an existing business process.

From a professional financial crime perspective, BEC is especially dangerous because it often targets moments of legitimate financial authority. Finance teams, treasury staff, accounts payable personnel, senior executives, law firms, and real estate professionals are common targets because they either control payment release or influence payment decisions. The instruction may appear urgent, confidential, commercially plausible, and consistent with the victim’s role. In many cases, the victim is not being asked to do something unusual in principle, only to do something routine under manipulated circumstances. This is why BEC is best understood as a control-evasion strategy rather than just a phishing event. It turns normal business workflow into the delivery mechanism for fraud. This is an inference supported by law-enforcement descriptions of BEC as involving compromised or spoofed communications used to conduct unauthorized fund transfers.

Watch on YouTube: Business Email Compromise (BEC) Fraud

The typology can take several forms. One common model is invoice or mandate fraud, where a supplier’s payment details are altered and future invoices are paid into a criminal-controlled account. Another is executive impersonation or “CEO fraud,” where a senior employee appears to instruct a subordinate to make an urgent confidential transfer. There are also payroll and data-theft variants, where employees are tricked into changing salary payment details or disclosing sensitive information that enables further fraud. Europol’s and the FBI’s public material both describe impersonation of executives or trusted business contacts as central to the typology, and UK Finance links invoice and mandate scams directly to compromised or intercepted email activity.

In the financial crime environment, the payment implications are critical. BEC usually culminates in an authorized payment, meaning the transfer may pass normal access and authentication controls because the payer believes it is legitimate. In that respect, BEC overlaps with authorized push payment fraud, but it often carries a stronger corporate and operational focus. The criminal objective is not just to trick an individual consumer, but to exploit formal business payment channels and trusted commercial relationships. Once funds arrive in the destination account, they are often moved quickly onward, which is why BEC frequently intersects with mule activity and laundering networks. Europol notes that stolen funds are swiftly transferred onward in online fraud schemes, and UK Finance reports that invoice and mandate scam losses are heavily concentrated in non-personal accounts and frequently originate via email.

This makes BEC a particularly important typology for firms managing both fraud and AML exposure. A bank or payment institution may first see BEC as an unusual outbound payment, an altered beneficiary instruction, or an incoming transfer to an account behaving like a mule destination. If the institution treats the matter only as a customer-authorized payment issue, it may miss the wider criminal infrastructure. Conversely, if it focuses only on the receiving account, it may not understand the upstream compromise or social-engineering channel that produced the funds. A mature response therefore requires coordination across cyber, fraud, payments, AML, investigations, and customer-contact functions. This is an inference based on the way official sources connect BEC to compromised communications, payment diversion, and onward movement of stolen funds.

Control design for BEC must therefore go beyond email security alone. Technical controls such as mailbox security, phishing resistance, access monitoring, and domain verification are important, but they are not sufficient by themselves. BEC succeeds when business process controls fail alongside communication controls. Effective mitigation usually requires independent verification of payment detail changes, callback procedures using trusted contact information, segregation of duties, dual approval for higher-risk transfers, stricter controls over beneficiary amendments, and challenge procedures for unusual urgency or secrecy. The FBI’s public materials stress that BEC frequently leverages compromised or spoofed communications to induce unauthorized transfers, which supports the need for out-of-band verification and stronger payment-governance controls.

Behavioral and contextual detection is also important. BEC-related payments may be suspicious because of the surrounding circumstances rather than because the value or beneficiary alone is inherently unusual. Indicators can include sudden changes in supplier bank details, payments to new jurisdictions, urgent requests outside normal workflow, deviations from historic invoice patterns, or instructions received through unusual channels or timings. On the receiving side, accounts may show mule characteristics such as rapid pass-through, multiple unrelated inbound credits, or activity inconsistent with the customer profile. These are practical inferences from the official descriptions of BEC, invoice-and-mandate scams, and money mule usage.

Governance is especially important because BEC often exploits weak ownership of payment controls across departments. Cyber teams may focus on mailbox compromise, finance teams on invoice handling, fraud teams on payment loss, and AML teams on suspicious fund flows. If no function has end-to-end visibility, the institution may address the visible symptom but not the systemic weakness. A professionally mature framework should therefore include BEC within fraud risk assessments, payment-control design, vendor-management procedures, cyber awareness, incident response, and management information. This broader governance need is an inference drawn from the cross-functional nature of BEC described by law-enforcement and industry sources.

The scale of the threat reinforces its importance. The FBI has called BEC one of the most financially damaging online crimes, and its 2024 Internet Crime Report separately tracks BEC losses as a major complaint category. In the UK, invoice and mandate scams, which often involve email compromise or interception, produced £20.9 million in losses in 2024, and 81% of reported cases originated via email. These figures show that BEC is not a niche cyber-fraud scenario but an established and costly component of the wider financial crime landscape.

Ultimately, Business Email Compromise is a major financial crime threat because it weaponises trusted business communication to trigger legitimate-looking payment actions that are criminal in substance. It exploits people, process, and payment workflow at the same time, and once successful it often feeds directly into mule networks and illicit fund movement. In a financial system where commercial payments depend heavily on email, digital collaboration, and remote approval, BEC cannot be treated as a simple phishing problem. It must be managed as a core financial crime typology requiring integrated controls across cyber security, payments governance, fraud prevention, AML monitoring, and operational response.