The Bank Secrecy Act (BSA) is the foundational U.S. anti-money laundering framework that authorizes the Treasury to impose recordkeeping, reporting, and program requirements on financial institutions and certain other businesses to help detect and prevent money laundering and related financial crime. FinCEN describes it as the nation’s first and most comprehensive federal AML statute, and explains that its reporting and recordkeeping requirements create a financial trail for investigators to follow.

In the financial crime environment, the BSA is significant because it turns private-sector financial activity into a source of actionable intelligence for law enforcement, regulators, and national-security authorities. It does not criminalize money laundering by itself in the same way that substantive criminal statutes do; rather, it creates the compliance architecture through which suspicious activity, large cash transactions, customer records, and transactional information can be captured, reviewed, and escalated. FinCEN states that the BSA requires institutions vulnerable to money laundering to take precautions against financial crime, including filing data about large cash transactions and suspicious transactions.

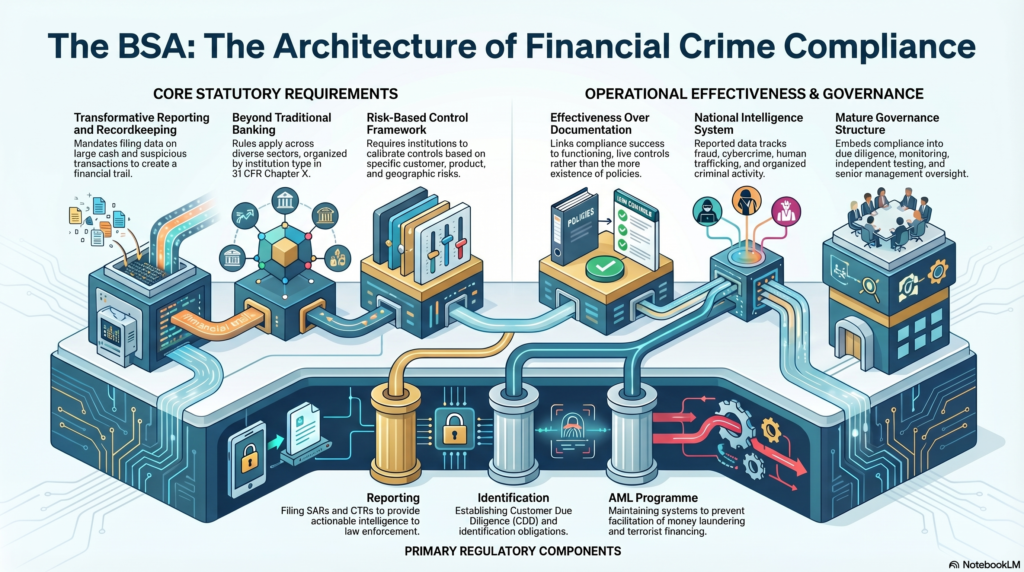

A professionally accurate understanding of the BSA begins with its operational purpose. The statute is not limited to banks, and its implementing regulations sit primarily in 31 CFR Chapter X, where FinCEN’s rules are organized by institution type and subject matter. Those rules cover general requirements and sector-specific obligations for institutions such as banks and money services businesses, among others. This matters in the financial crime environment because BSA obligations are not identical across all sectors; they are applied through a combination of general rules and industry-specific requirements.

From a control perspective, the BSA is the legal backbone of the U.S. AML compliance programme. It underpins requirements for suspicious activity reporting, currency transaction reporting, record retention, customer identification and due diligence obligations, and the maintenance of AML programmes reasonably designed to prevent institutions from being used to facilitate money laundering and terrorist financing. For banks, the BSA/AML compliance programme requirement is reflected in 31 CFR 1020.210, and comparable programme requirements exist for other covered sectors.

Watch on YouTube: Bank Secrecy Act (BSA)

In practical terms, the BSA matters because it forces institutions to look beyond individual transactions and understand the broader financial crime risk presented by their customers, products, services, delivery channels, and geographies. The FFIEC BSA/AML Manual explains that examination focuses on BSA/AML compliance programme requirements, risk management expectations, and risk-focused supervision. That means BSA compliance is not merely a filing exercise. It is a risk-based control framework that requires institutions to assess exposure, calibrate controls, investigate unusual activity, and maintain governance proportionate to their risk profile.

The reporting dimension of the BSA is especially important in the financial crime environment. FinCEN’s BSA filing framework requires electronic reporting through the BSA E-Filing System, and the reports generated under the regime are central to intelligence and investigative work. Suspicious activity reports, currency transaction reports, and related filings help identify patterns associated with fraud, money laundering, terrorist financing, sanctions evasion, structuring, human trafficking, cyber-enabled crime, and other illicit conduct. In this sense, the BSA is not only a compliance requirement imposed on firms; it is also a national information system for detecting and analyzing criminal finance.

One of the most important professional features of the BSA is that it links compliance effectiveness to program quality rather than to policy existence alone. A firm can have written procedures and still fail if its controls are weak in practice, if suspicious activity is poorly investigated, if data quality is deficient, or if management oversight is ineffective. The FFIEC materials emphasize risk assessment, scoping, programme assessment, and examination procedures, which reflects the expectation that institutions maintain live, functioning AML controls rather than static documentation.

The BSA also has a strong relationship to broader financial crime typologies. Although it is most closely associated with AML, the information gathered and reported under the BSA is used in cases involving fraud, cybercrime, sanctions-related concerns, corruption, and organized criminal activity. FinCEN’s overview explicitly notes that BSA information supports federal, state, local, and international law enforcement, and that the BSA’s reporting and recordkeeping requirements establish a financial trail to track criminals, their activities, and their assets. That makes the BSA relevant well beyond traditional laundering typologies alone.

Governance is central to BSA effectiveness. In a mature institution, BSA compliance should be embedded in customer due diligence, transaction monitoring, investigations, reporting, independent testing, training, and board or senior-management oversight. The FFIEC manual’s structure around risk assessment, programme review, and examination reinforces that BSA compliance must be demonstrable and proportionate to the institution’s business model. Put differently, the BSA does not simply ask whether an institution filed reports; it asks whether the institution has built a credible system for identifying when those reports and related controls are necessary.

Ultimately, the Bank Secrecy Act is fundamental in the financial crime environment because it provides the legal and regulatory framework through which the U.S. financial system is used to detect, document, and escalate suspicious financial behavior. It creates the recordkeeping, reporting, and programme obligations that make AML control possible at scale, while also supplying critical intelligence for investigations and enforcement. For that reason, the BSA should be understood not as a narrow technical statute, but as the core compliance architecture supporting U.S. financial crime detection, regulatory oversight, and investigative visibility.