Chargeback fraud is a form of payment abuse in which a cardholder, or someone acting through a cardholder account, disputes a transaction that was in fact legitimate in order to obtain a reversal of funds while retaining the goods, services, or benefit received. In the financial crime environment, this is more than a routine disputes issue. It is a fraud typology that exploits consumer protection mechanisms built into card payment systems and shifts loss, operational burden, and evidential pressure onto merchants, acquirers, and payment service providers. While chargebacks are an essential safeguard for unauthorized transactions and genuine service failures, they can also be misused as a vehicle for deception when the dispute itself is dishonest.

From a professional financial crime perspective, chargeback fraud is significant because it attacks trust at the post-transaction stage rather than at the point of authorization alone. The original purchase may have passed authentication, authorization, and merchant controls successfully, yet the transaction is later challenged as unauthorized, unrecognized, or unfulfilled. This creates a distinct control problem: the fraud is not necessarily in how the payment was initiated, but in how the payment is later contested. That makes chargeback fraud fundamentally different from many other payment fraud typologies, because the criminal act may occur after the transaction has been completed and value has already been delivered.

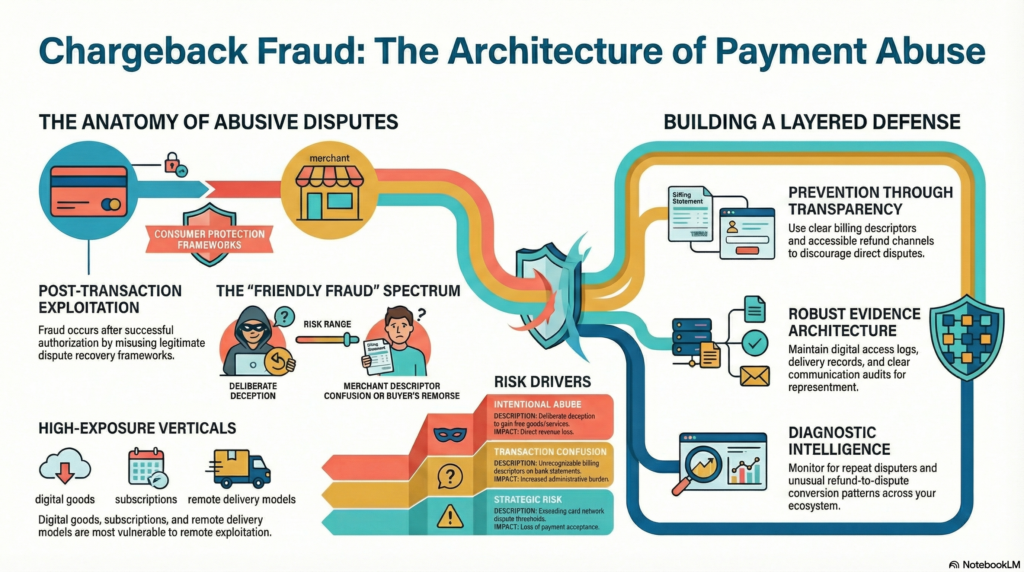

A central feature of chargeback fraud is the misuse of a legitimate dispute framework. Card chargebacks exist to protect consumers where fraud, processing error, non-delivery, duplicate billing, or service failure has occurred. In genuine cases, the mechanism is an important component of payment system integrity. However, the same framework can be manipulated where a customer falsely claims that a valid transaction was unauthorized, that goods were not received when they were, or that a subscription or recurring payment was not understood despite proper disclosure. In some cases the dispute is deliberate; in others it may arise from transaction confusion, household misuse, poor descriptor recognition, or buyer’s remorse that is later framed as fraud. From an institutional perspective, these distinctions matter operationally, but all can generate losses and control stress if not managed properly.

In the financial crime environment, chargeback fraud should be understood as part of a broader ecosystem of payment abuse rather than as an isolated merchant inconvenience. It can overlap with first-party fraud, digital commerce abuse, subscription fraud, refund abuse, account misuse, and friendly fraud typologies. The term “friendly fraud” is often used for cases where the genuine cardholder, or someone within their household, initiates a false dispute against a legitimate transaction. Despite the label, the commercial and control impact is not benign. Fraudulent disputes can create direct revenue loss, administrative cost, higher scheme fees, deterioration in fraud ratios, and elevated risk of merchant monitoring or remediation programmes where chargeback thresholds are exceeded.

Watch on YouTube: Chargeback Fraud

One reason chargeback fraud is so difficult to manage is that it often sits in a grey area between true criminal intent, customer misunderstanding, and weak transaction transparency. A cardholder may fail to recognize a merchant descriptor, forget a purchase, dispute a family member’s transaction, or wrongly assume that a chargeback is simply another route to a refund. In more deliberate cases, a customer may knowingly consume a service, receive a product, or benefit from digital content and then dispute the payment afterward. This ambiguity creates evidential and operational complexity. Unlike card-not-present fraud, where the central question is often whether the payment was authorized, chargeback fraud often turns on whether the later dispute is honest and whether the merchant can evidence legitimacy convincingly enough to withstand reversal.

The typology is especially important in digital commerce and remote payment environments. E-commerce, digital subscriptions, online services, downloadable goods, gaming, travel, and recurring billing models are particularly exposed because delivery is remote, physical proof may be limited, and the customer relationship often depends on digital records rather than face-to-face interaction. Where transactions are frictionless and fulfillment is immediate, it may be difficult for the merchant to reconstruct a sufficiently persuasive audit trail after the fact. This means chargeback fraud is not simply a payments issue; it is also a data, evidence, and operational-design issue. Businesses that cannot demonstrate clear authorization, recognizable descriptors, transparent billing terms, fulfillment records, and customer communications are more vulnerable even when the underlying transaction was genuine. This is an inference supported by the way card networks and payment providers describe dispute prevention and chargeback management.

From a financial crime control standpoint, chargeback fraud exposes the limits of viewing authorization as the end of risk assessment. A transaction that is properly authenticated can still become a loss event if the post-sale environment is weak. Clear receipts, recognizable billing names, delivery confirmation, customer service responsiveness, cancellation transparency, digital access logs, and evidence of use all become part of the control framework. In that sense, effective prevention of chargeback fraud extends beyond fraud screening at checkout and into merchant operations, communications design, refunds handling, and dispute intelligence. Firms that separate fraud prevention from post-transaction servicing too rigidly often leave exploitable gaps.

There is also a strong governance dimension. Excessive chargebacks can trigger card-network monitoring programmes, higher compliance costs, remediation requirements, and potentially serious consequences for merchants or payment partners. That makes chargeback fraud not only a source of direct loss but also a strategic risk to payment acceptance capability and commercial sustainability. Where dispute rates rise materially, institutions need to understand whether the driver is true third-party fraud, weak customer communication, merchant descriptor confusion, poor fulfilment, abusive customer behavior, or deliberate first-party fraud. A high chargeback rate is therefore a diagnostic signal, not merely an accounting outcome.

A mature financial crime response to chargeback fraud requires layered controls across prevention, detection, evidence, and escalation. Preventive measures include clear transaction descriptors, transparent pricing and renewal terms, strong customer communication, robust delivery and fulfillment records, authentication where appropriate, and accessible refund channels that reduce the incentive to go directly to a dispute. Detection controls should identify patterns such as repeat disputers, unusual refund-to-dispute conversion, clustering by merchant category, high-risk digital goods, abusive subscription behavior, or concentration of disputes linked to the same customer, device, or household. Strong case management is equally important because the institution must be able to distinguish ordinary consumer remediation from suspected abusive conduct. This operational approach is an inference grounded in the dispute-management and friendly-fraud guidance reflected across payment-network materials.

Chargeback fraud also has implications for the wider financial crime framework. While many cases are commercial in nature, repeated abusive disputes may indicate broader first-party fraud behavior, exploitation of digital commerce systems, collusive activity, or connected misuse across multiple merchants and payment instruments. Where accounts show repeated patterns of disputed legitimate spending, linked identities, or beneficiary relationships associated with broader fraudulent conduct, the issue may move beyond merchant-loss management into a wider fraud and AML assessment. Not every chargeback fraud case is a laundering concern, but repeated abuse of payment reversals can form part of a larger pattern of deception, value extraction, and illicit use of customer or merchant infrastructure. This is an inference based on the nature of first-party fraud and the way payment abuse can intersect with wider financial crime behavior.

Operational response matters once chargeback fraud is suspected. Firms need structured dispute review processes, evidence standards, representment strategies where appropriate, customer-service pathways, and escalation routes for repeated or abusive conduct. The objective is not simply to contest every dispute, but to distinguish efficiently between genuine claims and suspicious ones, preserve evidence early, and reduce future exposure through control improvements. Poorly managed responses can increase losses twice: first through the original chargeback, and then through avoidable repeat abuse caused by weak learning loops and inconsistent handling.

Ultimately, chargeback fraud is a material financial crime risk because it weaponises a legitimate consumer-protection mechanism against the payment ecosystem itself. It allows bad actors to reverse valid transactions, externalize loss, and exploit the evidential asymmetry between cardholders and merchants after value has already changed hands. In a digital commerce environment shaped by remote delivery, subscription models, fast checkout, and high transaction volumes, this typology cannot be treated as a minor disputes nuisance. It requires disciplined governance, strong evidence architecture, intelligent detection, and close coordination across fraud, payments, operations, merchant risk, and customer service functions. Only by treating chargeback fraud as part of the broader financial crime landscape can institutions build controls that are commercially practical, operationally defensible, and resilient over time.