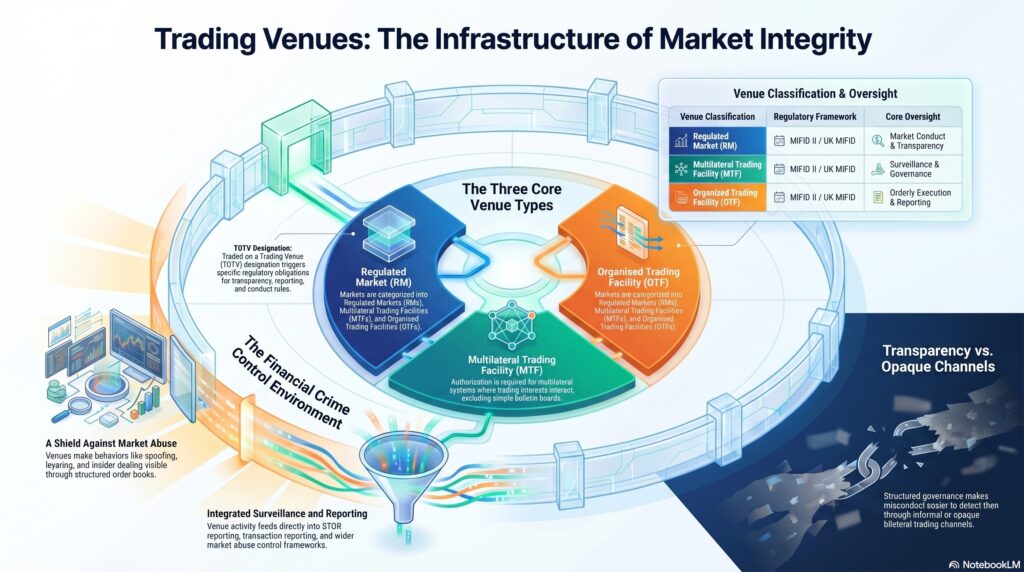

A trading venue is a defined market structure under the MiFID framework. ESMA’s MiFID II rulebook states that a “trading venue” means a regulated market, an MTF or an OTF, and the FCA says there are three types of trading venue under the UK MiFID framework: regulated markets (RMs), multilateral trading facilities (MTFs), and organised trading facilities (OTFs).

In the financial crime environment, trading venues matter because they are the organized settings in which financial instruments are bought and sold, and therefore where many important market-integrity and conduct risks either arise or become visible. While a trading venue is not itself a financial crime typology, it is a core part of the infrastructure through which market abuse, manipulative trading, insider dealing, false market signals, and suspicious order activity may occur or be detected. The FCA’s guidance on the trading venue perimeter says trading venues operate organised markets where financial instruments are bought and sold, and its market abuse framework treats trading behavior on these venues as a central area of regulatory concern.

From a professional perspective, the significance of a trading venue lies in market organization, transparency, and supervision. A venue brings together trading interests under defined rules, governance, and surveillance arrangements. That matters because financial crime and misconduct in markets are often easier to detect where activity occurs within a structured venue environment rather than through informal or opaque bilateral channels. ESMA’s market structure materials and MiFID definitions show that the concept of a trading venue is central to how European markets are categorized and supervised.

Watch on YouTube: Trading Venue

A key operational point is that not every system where buyers and sellers communicate is a trading venue. The FCA’s perimeter guidance explains that firms may require authorization as a trading venue where they operate a multilateral system, and its handbook guidance notes that a bulletin board would not usually be considered a trading venue where there is no interaction between trading interests within the system. That distinction matters because a venue designation carries regulatory obligations around market conduct, transparency, and operational controls.

In practical financial crime terms, trading venues are especially relevant to market abuse detection. Suspicious orders and transactions, spoofing, layering, marking the close, and other manipulative behaviors often play out through venue-based order books and execution activity. A trading venue therefore sits close to trade surveillance, STOR reporting, transaction reporting, and the wider market-abuse control framework. This is an inference supported by the central role venues play in organized trading and by MAR/MiFID-linked supervision of market conduct.

Trading venues are also important because they anchor a wider set of regulatory concepts. ESMA has specifically clarified the meaning of “traded on a trading venue” (TOTV) because that concept affects multiple MiFID II and MiFIR provisions. This shows that the trading venue concept is not merely descriptive; it determines how various transparency, reporting, surveillance, and conduct rules apply.

A mature financial crime and conduct framework therefore treats the trading venue as more than just a place where execution occurs. It is part of the control environment for orderly markets, fair access, transparent trading, and detection of abusive conduct. Where venue governance, surveillance, and reporting are strong, market-integrity risks are easier to identify and escalate. Where the perimeter is unclear or venue controls are weak, misconduct can become harder to supervise. This is an inference supported by the FCA’s perimeter guidance and ESMA’s MiFID framework.

Ultimately, a trading venue is significant in the financial crime environment because it is one of the core regulated settings in which market activity takes place and is monitored. It provides the organized framework within which trading is executed, transparency rules apply, and suspicious behavior can be identified and investigated.