Trade reconstruction is the process of rebuilding, in a reliable and reviewable way, the full lifecycle of a trade or order from the available records, data, and related communications. In the market-regulation context, this usually means being able to recreate who placed the order, when it was entered, how it was modified, routed, executed, or cancelled, and what related records or communications explain it. ESMA’s MiFID II recordkeeping guidance links transaction reporting and order-record requirements to scenarios involving transaction and order recordkeeping, and industry regulatory materials refer to trade reconstruction as part of responding to regulatory inquiries and surveillance reviews.

In the financial crime environment, trade reconstruction matters because many forms of market misconduct are pattern-based and sequence-dependent. Insider dealing, spoofing, layering, front running, marking the close, wash trading, and other abusive behaviors are often impossible to assess from a single trade record alone. Regulators and firms need to reconstruct the sequence of orders, executions, amendments, cancellations, positions, and related communications to understand whether the activity had a legitimate rationale or was manipulative or abusive. This is an inference supported by ESMA’s and FCA’s market-abuse frameworks, which depend on effective surveillance and reporting of suspicious orders and transactions.

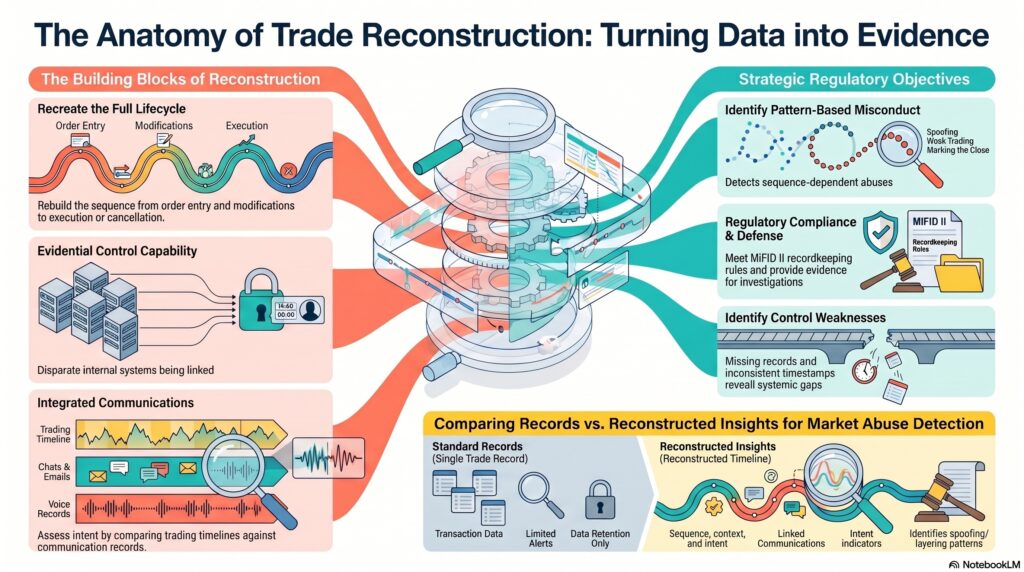

From a professional perspective, trade reconstruction is not just a data-retention issue. It is an evidential control capability. A firm may store huge volumes of order and trade data, but if those records cannot be linked coherently across systems, timestamps, users, venues, and communications, the firm may still be unable to explain what happened. That becomes a serious problem in surveillance, internal investigations, regulatory inquiries, and enforcement matters. The older FINRA comment material explicitly refers to regulatory inquiries involving trade reconstruction and related document production, which reflects how central this capability is in practice.

Watch on YouTube: Trade Reconstruction

This is why trade reconstruction depends heavily on recordkeeping quality. MiFID II/MiFIR recordkeeping and reporting rules are designed in part so that competent authorities can understand trading behavior after the event. ESMA’s transaction-reporting and order-recordkeeping guidance shows that the regime is built around consistent, structured, and reviewable records rather than only real-time monitoring. In practical terms, good reconstruction requires accurate timestamps, account and trader identifiers, order history, venue data, execution records, and, where relevant, links to communications and client instructions.

Trade reconstruction is especially important in market surveillance and investigations. A suspicious pattern may first appear as an alert, but the next step is often reconstructing the trade sequence to see whether the alert reflects genuine misconduct. That may include looking at pre-trade activity, order-book behavior, amendments and cancellations, fills, positions, and post-trade effects. Where communications surveillance is also available, investigators may compare the trading timeline against chats, emails, or voice records to assess intent and awareness. This is an inference supported by the role of order and transaction recordkeeping in market-abuse supervision.

A mature trade-reconstruction capability therefore supports several objectives at once. It helps firms investigate internal alerts, respond to regulator questions, support STOR decisions, evidence best execution and order handling, and defend or challenge allegations of market abuse. It also helps identify control weaknesses, such as missing records, poor system linkage, inconsistent timestamps, or gaps between trading and communications data. This is an inference from the cited reporting and recordkeeping frameworks and their supervisory use.

Ultimately, trade reconstruction matters in the financial crime environment because it turns fragmented order and trade records into a coherent account of what actually happened in the market. Without it, firms and regulators may see suspicious outcomes but be unable to prove the sequence, context, or intent behind them. With it, they gain a critical evidential tool for market abuse detection, investigation, and enforcement.