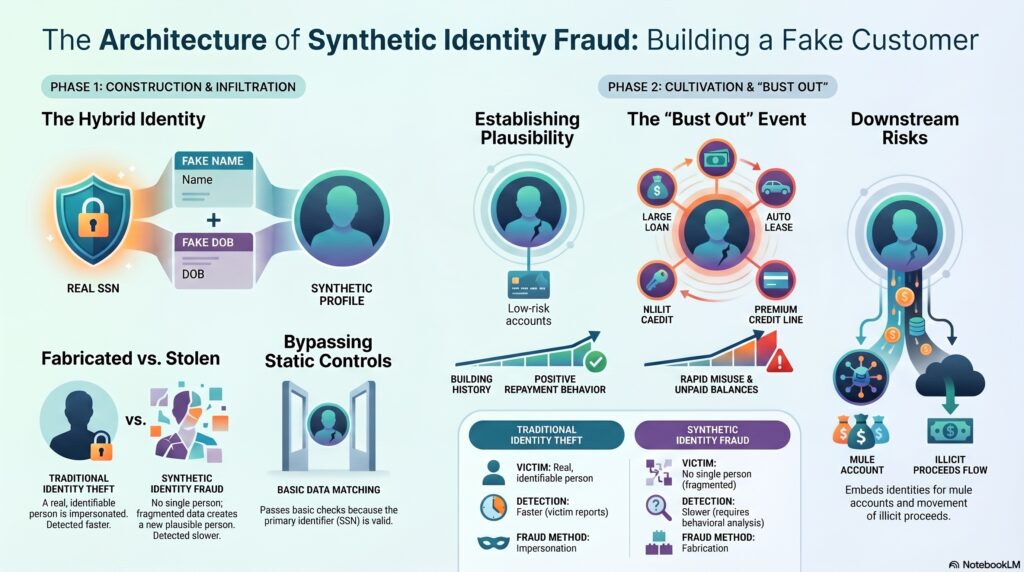

Synthetic fraud, more commonly called synthetic identity fraud, is a fraud typology in which criminals create a false identity by combining real personal information with fabricated information. The Federal Reserve’s interagency authentication guidance states that, unlike typical identity theft where a real person’s identity is stolen and used, a synthetic identity is a completely fabricated identity that does not correspond to any actual person. Industry and fraud-management sources often describe it as mixing a real identifier, such as a Social Security number, with a false name, date of birth, address, or other details to create a new identity.

In the financial crime environment, synthetic identity fraud matters because it attacks one of the basic assumptions of financial services: that the identity presented at onboarding corresponds to a real, knowable person. With synthetic identity fraud, the criminal does not always impersonate an existing customer in the traditional sense. Instead, they manufacture a customer that appears credible enough to pass parts of the onboarding, credit, or servicing process. That makes the typology especially dangerous in lending, payments, cards, deposit accounts, and digital onboarding environments. This is an inference supported by the Federal Reserve’s distinction between synthetic identities and traditional stolen-identity fraud.

A key professional distinction is that synthetic identity fraud differs from ordinary identity theft. The CFPB’s regulation defines identity theft as a fraud committed or attempted using the identifying information of another person without authority. Synthetic identity fraud may involve misuse of a real identifier, but the overall identity is often not a real existing person in full. That is why the typology can be harder to detect and harder to remediate than standard true-name identity theft.

Watch on YouTube: Synthetic Fraud or Synthetic Identity Fraud

From a professional perspective, the fraud often develops over time rather than in a single event. A synthetic identity may first be used to open a low-risk account or obtain a small amount of credit. The fraudster may then cultivate that identity by creating transaction history, establishing repayment behavior, or building a credit profile before “busting out” with larger fraud, unpaid balances, or rapid misuse. While the exact lifecycle varies, the underlying control problem is consistent: the institution is dealing with an identity that appears plausible but is fundamentally false. This is an inference supported by common industry descriptions of synthetic identity fraud as the creation of a “new” identity from mixed real and fake data.

This typology is important in the financial crime environment because it sits at the intersection of identity fraud, application fraud, account abuse, and wider illicit-finance risk. A synthetic identity can be used to obtain credit, payment instruments, account access, or transactional infrastructure that later supports other frauds or movement of illicit proceeds. In that sense, synthetic identity fraud is not only an onboarding problem. It can become a downstream fraud, mule-account, or suspicious-activity issue once the false identity is embedded in the financial system. This is an inference drawn from how synthetic identities are created and then used to commit fraud.

For firms, the core challenge is that synthetic identities can pass controls that focus too narrowly on document presenceor basic data matching. A real identifier paired with fabricated details may produce a partial appearance of legitimacy. That means effective control usually requires more than static verification. It may require identity-resolution logic, behavioral analysis, cross-field consistency checks, linked-account analysis, device and contact-point review, and stronger scrutiny of thin-file or recently created identities. This is an inference supported by the Federal Reserve’s warning that synthetic identities are fabricated rather than straightforwardly stolen.

Ultimately, synthetic fraud or synthetic identity fraud is significant in the financial crime environment because it allows criminals to create a false customer that can interact with the financial system as if it were real. It is harder to detect than many traditional identity-fraud typologies because the identity may not belong fully to any one victim, and it can mature into broader fraud and illicit-value movement over time. For that reason, it should be treated as a distinct and serious identity-risk typology within fraud, onboarding, and financial crime control frameworks.