Structuring is the act of breaking up transactions to evade legal reporting or recordkeeping requirements. FinCEN says structuring is the breaking up of transactions for the purpose of evading Bank Secrecy Act reporting and recordkeeping requirements, and the FFIEC states that structuring transactions to evade BSA reporting and certain recordkeeping requirements can result in civil and criminal penalties.

In the financial crime environment, structuring matters because it is one of the clearest signs that a person may be trying to keep cash or cash-equivalent activity below regulatory visibility thresholds. The most familiar example is breaking a cash transaction that would otherwise trigger a Currency Transaction Report into smaller amounts below $10,000, whether across one day, multiple days, multiple branches, or multiple institutions. The IRS’s structuring guidance gives examples such as making deposits into multiple accounts or at multiple institutions, all below $10,000 but together above that level.

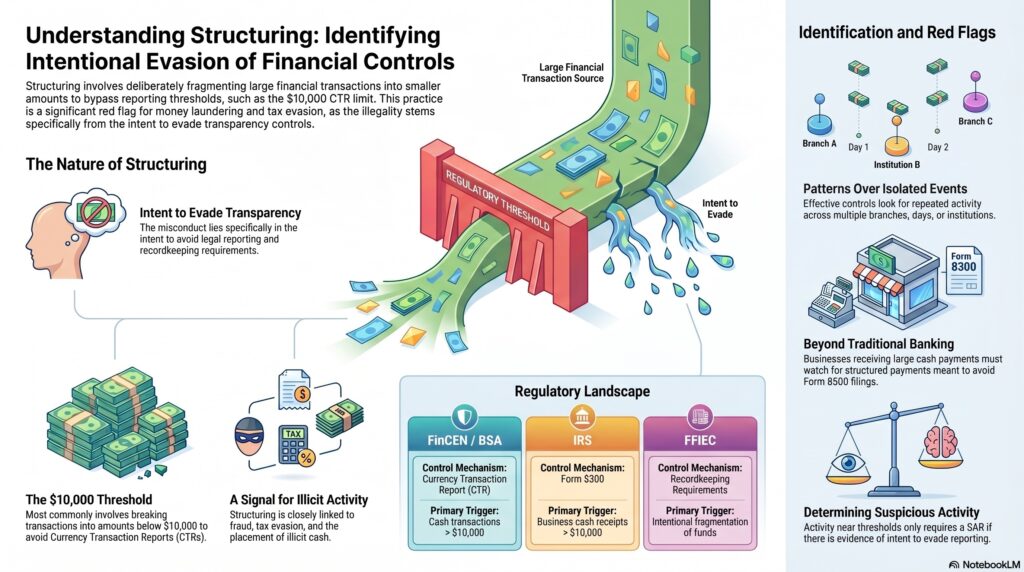

From a professional perspective, structuring is significant because the misconduct lies not only in the movement of funds, but in the intent to evade transparency requirements. A series of smaller transactions is not automatically improper. What makes it structuring is that the transactions are arranged for the purpose of avoiding reporting or recordkeeping obligations. The FFIEC’s definition and the eCFR reference both emphasize that the key element is conduct undertaken to evade CTR or related BSA requirements.

Watch on YouTube: Structuring

This is why structuring is closely linked to AML, fraud, tax evasion, and proceeds-of-crime risk. A customer who deliberately fragments transactions may be trying to place illicit cash into the financial system, disguise the scale of activity, avoid audit trails, or reduce the chance of law-enforcement attention. FinCEN’s CTR educational materials state that customers who attempt to break up transactions to evade CTR reporting face potential civil and criminal consequences.

Structuring is also relevant outside traditional bank deposits. The IRS Form 8300 guidance says structuring can include breaking up large cash transactions into smaller cash transactions to disguise the true amount involved and make it appear that Form 8300 filing is unnecessary. That means the concept is important not only for banks, but also for businesses receiving reportable cash payments.

A mature control framework therefore looks for patterns rather than isolated amounts. Relevant indicators include repeated cash transactions just below reporting thresholds, transactions split across branches or entities, multiple people acting on behalf of the same source of funds, or explanations that do not match the pattern of activity. FinCEN’s October 2025 SAR FAQs also make an important point: activity merely near the CTR threshold is not, by itself, enough to require a structuring SAR without information suggesting an intent to evade reporting requirements.

Ultimately, structuring is important in the financial crime environment because it is a deliberate attempt to defeat one of the financial system’s core transparency controls. It is not just small transactions; it is the intentional fragmentation of activity to avoid detection, reporting, or recordkeeping. For that reason, structuring should be treated as a serious AML red flag and a direct challenge to the integrity of regulatory reporting controls.