Social engineering is the use of deception, manipulation, or impersonation to persuade a person to reveal information, bypass controls, or take an action that benefits the attacker. CISA describes it as tricking someone into revealing information such as a password or taking an action that can expose them to compromise, and its glossary defines it as the use of deception to manipulate individuals into divulging confidential or personal information.

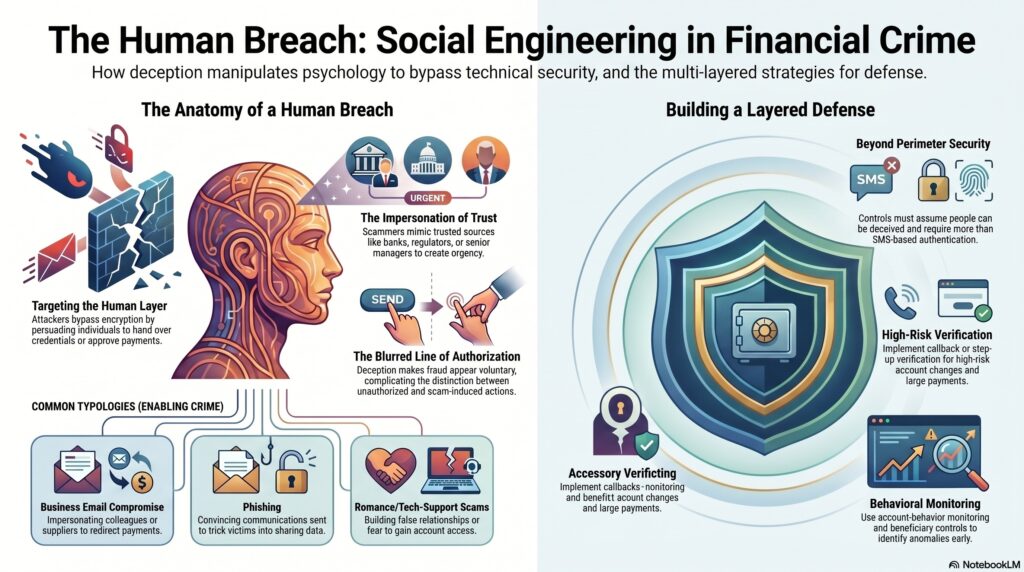

In the financial crime environment, social engineering matters because it targets the human control layer rather than the technical one. A criminal may not need to defeat encryption, break a system, or steal a device if they can instead persuade an employee, customer, or third party to hand over credentials, approve a payment, reset an account, or trust a false instruction. CISA notes that attackers use human interaction and social skills to obtain or compromise information, and the FTC’s business guidance explains that scammers often create urgency or fear while pretending to be a trusted source such as a senior employee or familiar organization.

From a professional perspective, social engineering is not a narrow cyber term. It is a core fraud and financial crime enabler. Phishing, impersonation scams, business email compromise, tech-support scams, romance scams, fake invoice requests, and account-recovery fraud all depend on some form of social engineering. The FTC’s phishing materials explain that phishing messages aim to get victims to provide personal information or access, while FATF’s recent cyber-enabled fraud paper says digitalisation has accelerated increasingly sophisticated social engineering schemes.

Watch on YouTube: Social Engineering

This is why social engineering is so important operationally. It can compromise several parts of the financial crime framework at once. It may defeat authentication by capturing passwords or one-time codes. It may undermine payments controls by tricking a victim into authorizing a transfer. It may weaken customer due diligence and identity controls by obtaining stolen personal data. It may also compromise internal escalation or supervisory processes if employees are manipulated into overriding normal controls. FATF’s cyber-enabled fraud work explicitly links deceptive social engineering techniques to illicit financial flows and broader AML/CFT concerns.

A key feature of social engineering is impersonation of trust. The attacker typically claims to be someone the victim is expected to trust: a bank, regulator, supplier, colleague, senior manager, telecom provider, or government body. The FTC notes that phishing messages often appear to come from a well-known source, while CISA’s glossary describes phishing as a social engineering technique where threat actors send convincing communications to trick individuals into clicking, sharing, or responding.

In financial crime terms, social engineering is especially dangerous because it can make a fraudulent action appear voluntary or authorized. A victim may initiate a payment themselves, disclose security details directly, or confirm a fraudulent request because they believe the request is genuine. That blurs the line between unauthorized compromise and scam-induced authorization, which is why social engineering is central to APP fraud, business email compromise, SIM-swap-related account takeover, and many other typologies. This is an inference supported by the FTC’s and CISA’s descriptions of how attackers manipulate victims into acting against their own interests.

A mature control response therefore cannot rely only on perimeter technology. It needs layered controls that assume people can be deceived. These include stronger-than-SMS authentication, callback or step-up verification for high-risk changes or payments, clear customer and employee awareness training, account-behavior monitoring, beneficiary controls, and rapid incident-response processes. CISA’s phishing and social engineering guidance emphasizes recognition and reporting, which reflects the importance of early interruption before the deception turns into account compromise or loss.

Ultimately, social engineering is a core concept in the financial crime environment because it converts trust, urgency, and human judgment into a pathway for fraud, account abuse, identity compromise, and illicit fund movement. It is often the first step in a wider financial crime chain. For that reason, social engineering should be understood not just as a cybersecurity problem, but as a foundational fraud and financial crime technique that cuts across customer protection, AML, payments, and internal controls.