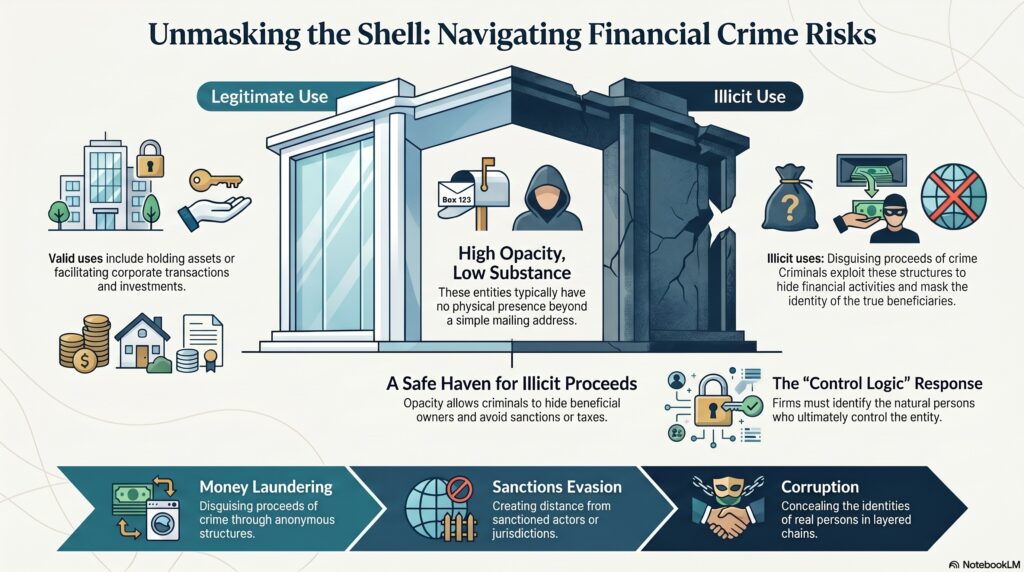

A shell company is generally a legal entity that has little or no independent business activity, few or no significant operations, and limited or no related assets. FATF’s beneficial ownership guidance says that, for its purposes, shell companies are companies that are incorporated but have no significant operations or related assets. FinCEN similarly describes shell companies, in its 2006 guidance usage, as non-publicly traded corporations, LLCs, and trusts that typically have no physical presence other than a mailing address and generate little to no independent economic value.

In the financial crime environment, shell companies matter because they can be used to separate legal ownership from real control. A shell company is not inherently illegal. FATF and FinCEN both recognize that shell companies may be formed for legitimate purposes, such as holding assets, facilitating corporate transactions, or structuring investment activity. The financial crime concern arises when the shell company is used to obscure the beneficial owner, hide the source or destination of funds, create distance from a sanctioned or corrupt actor, or give illicit activity an appearance of legitimacy.

From a professional perspective, the core risk is opacity. A shell company can provide a legal form without meaningful commercial substance. That makes it easier to hide who really owns or controls the entity, why it exists, and whether the activity flowing through it has a genuine economic purpose. FATF states that shell companies can become a safe haven for illicit proceeds and says anonymous shell companies are among the most widely used methods for laundering the proceeds of crime and corruption.

Watch on YouTube: Shell Company

This is why shell companies are closely associated with money laundering, corruption, sanctions evasion, tax abuse, and concealment of beneficial ownership. FATF and Egmont case analysis found that legal persons, principally shell companies, are a key feature in schemes designed to disguise beneficial ownership. In practical terms, that means a shell company may be used to open bank accounts, hold real estate, move funds, enter contracts, or sit within layered ownership chains while shielding the real person behind the structure.

For financial institutions, the existence of a shell company is therefore not the end of the analysis. The real question is whether the entity has a credible purpose, understandable ownership, and commercially coherent activity. The FCA’s financial crime work has highlighted failures to understand the reasons for complex and opaque offshore company structures, which is directly relevant here. A shell company with transparent ownership and a clear holding purpose may be manageable. A shell company with nominee-style arrangements, unexplained layering, or no obvious economic rationale is far more concerning.

This is why shell companies are central to beneficial ownership due diligence. FATF’s current beneficial ownership work is aimed at ensuring shell companies can no longer be a safe haven for illicit proceeds, and FinCEN has described beneficial ownership reporting as an effort to unmask shell companies used by money launderers, drug traffickers, sanctioned oligarchs, and other criminals. Even where legal reporting obligations evolve, the control logic remains the same: firms need to know the natural persons who ultimately own or control the entity.

A mature control response therefore looks beyond incorporation documents and asks several practical questions. Who ultimately owns or controls the company? What assets or activity does it actually have? Why is the structure needed? Does its jurisdictional footprint make commercial sense? Are the incoming and outgoing funds consistent with its stated purpose? Where firms cannot answer those questions satisfactorily, the shell company creates heightened AML, sanctions, and fraud risk. This is an inference supported by the FATF and FCA materials on beneficial ownership transparency and opaque structures.

Ultimately, a shell company is significant in the financial crime environment because it can provide a legally valid but economically thin vehicle through which ownership, control, and illicit financial activity are concealed. It is not suspicious by definition, but it is one of the most important legal structures for firms to understand properly when assessing money laundering, corruption, sanctions, and broader financial crime risk.