The Senior Managers and Certification Regime (SM&CR) is the UK individual-accountability framework for financial services firms. The FCA says the regime aims to reduce harm to consumers and strengthen market integrity by creating a system that enables firms and regulators to hold people to account. HM Treasury’s 2025 reform consultation also states that the regime’s objectives are to reduce harm to consumers, strengthen market integrity, and improve the safety and soundness of the financial services sector.

In the financial crime environment, SM&CR is significant because it shifts the focus from firm-level controls alone to personal accountability for how those controls are designed, overseen, and operated. AML, sanctions, fraud, market abuse, customer due diligence, and wider conduct controls do not fail only because a policy was missing. They often fail because no senior person took reasonable steps to ensure the relevant area was properly controlled, resourced, escalated, and monitored. The PRA has said the regime was introduced to support a change in culture at firms, and the PRA’s 2023 review materials describe a core requirement that the most senior decision-makers be fit and proper and take reasonable steps in carrying out their duties.

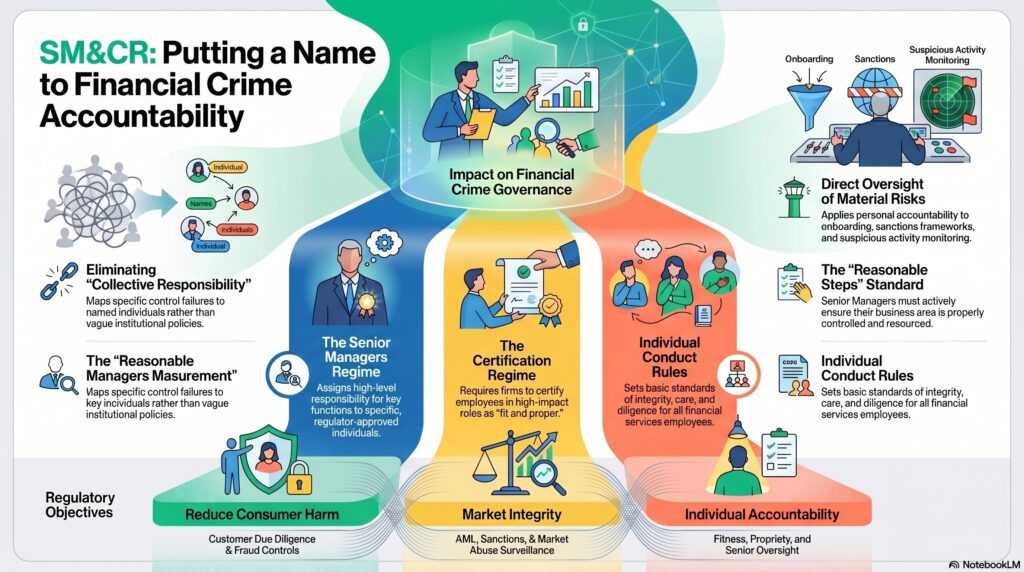

From a professional perspective, SM&CR matters because it makes financial crime governance more explicit, allocated, and challengeable. The regime is built around three parts: the Senior Managers Regime, the Certification Regime, and the Conduct Rules. HM Treasury’s 2025 consultation sets out those three parts directly, and the FCA’s SM&CR overview describes the regime in the same way.

Watch on YouTube: Senior Managers and Certification Regime

The Senior Managers Regime is the part most closely associated with accountability at the top of the firm. The FCA says the most senior people performing key roles, known as Senior Management Functions or SMFs, need FCA or PRA approval before starting. In financial crime terms, this matters because responsibility for areas such as compliance, AML oversight, operational controls, or business lines can be clearly mapped to named individuals. That makes it harder for serious control failures to disappear into vague collective responsibility.

The Certification Regime extends the accountability logic below the most senior tier. The FCA says it covers functions that are not SMFs but can have a significant impact on customers or the firm, and firms must assess these people as fit and proper. In the financial crime environment, this is highly relevant because many material risks sit with people who are not board-level senior managers: traders, relationship managers, onboarding approvers, surveillance staff, sanctions specialists, and others whose decisions can materially affect customer outcomes, market integrity, or the firm’s exposure to criminal misuse.

The Conduct Rules are equally important. PRA consultation material from July 2025 reiterates that the Individual Conduct Rules require employees to act with integrity, due care, skill and diligence, and to be open and cooperative with regulators. It also notes that Senior Manager Conduct Rules include the requirement to take reasonable steps to ensure that the business for which a senior manager is responsible is controlled effectively. In the financial crime environment, those standards matter because many AML, fraud, sanctions, and market-conduct failures are ultimately failures of integrity, competence, escalation, or effective control.

This is why SM&CR is so relevant to financial crime governance. A firm may have policies, monitoring systems, and committees, but the regime requires clearer allocation of responsibility and a stronger expectation that individuals in senior roles will understand and manage the risks in their area. In practical terms, this can affect the oversight of onboarding, suspicious activity processes, sanctions frameworks, fraud controls, surveillance, and remediation of known weaknesses. This is an inference supported by the FCA’s stated purpose of holding people to account and the PRA’s emphasis on reasonable steps and effective control.

SM&CR is also a live and evolving regime. The FCA published CP25/21 on 15 July 2025, proposing first-phase reforms to make the regime more proportionate and efficient while preserving its core accountability aims, and HM Treasury consulted in parallel on wider reforms. That means firms should understand SM&CR not as a fixed historical implementation, but as an active accountability framework still being refined.

Ultimately, the Senior Managers and Certification Regime matters in the financial crime environment because it helps ensure that responsibility for preventing and managing financial crime is not left vague or purely institutional. It puts individual accountability, fitness and propriety, and conduct standards at the center of how firms govern risk. That makes it one of the key UK frameworks linking financial crime controls to named human responsibility.