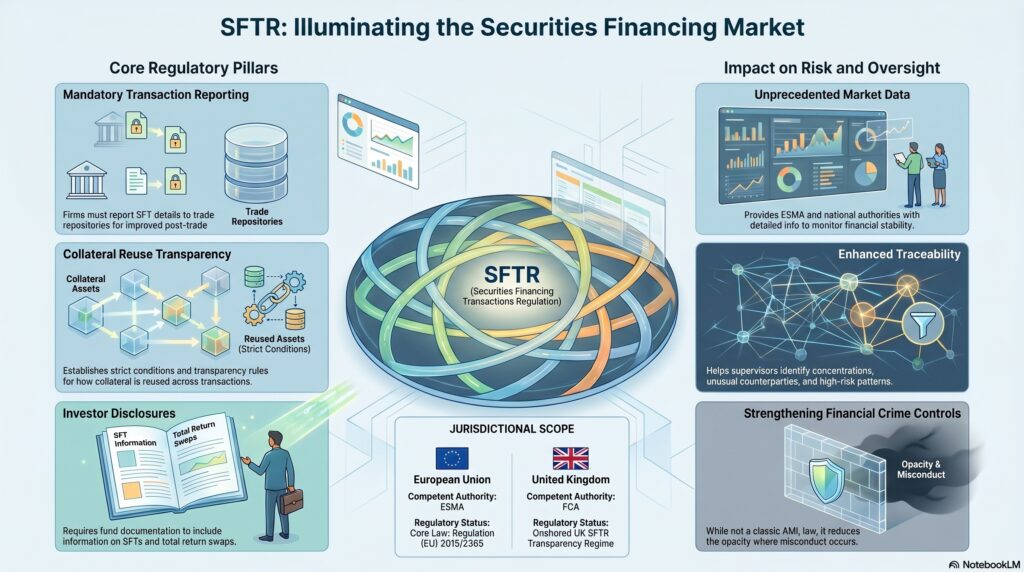

The Securities Financing Transactions Regulation (SFTR) is the EU transparency regime for securities financing transactions (SFTs) and the reuse of collateral. The core law is Regulation (EU) 2015/2365, which the European Commission describes as the framework for reporting details of SFTs to trade repositories and for improving transparency around SFTs and total return swaps. ESMA’s rulebook presents SFTR as the regulation on transparency of securities financing transactions and of reuse.

In the financial crime environment, SFTR matters because it improves visibility over a part of the market that can otherwise be complex, high-volume, and opaque. Securities financing transactions such as repos, securities lending, and similar arrangements are legitimate and important market activities, but they also involve rapid movement of securities and collateral, cross-border counterparties, and layered market infrastructure. The European Commission says the EU SFT regime was designed to increase transparency so that securities financing markets can be monitored and risks identified.

From a professional perspective, SFTR is not a classic AML statute. It is a post-trade transparency and reporting framework. Its financial-crime relevance comes from the fact that better reporting and better data make it easier for regulators and firms to understand who is transacting, what instruments and collateral are involved, and how risk is moving through the market. ESMA says SFTR reporting covers data access, collection, verification, aggregation, comparison, and publication of data on SFTs by trade repositories. That stronger data environment supports supervision and reduces opacity, which is often where misconduct and control failures are harder to detect.

Watch on YouTube: Securities Finance Transaction Regulation

A key reason SFTR matters is that securities financing markets are systemically important. ESMA’s April 2024 overview of EU securities financing markets said SFTR created a Union-wide framework under which details of SFTs can be efficiently reported, giving national competent authorities and ESMA an unprecedented level of detailed information on the characteristics of SFTs and supporting financial stability monitoring. In the financial crime environment, that means SFTR strengthens the evidential and supervisory foundation around transactions that can otherwise look operationally routine but may mask concentration, unusual collateral movement, or other higher-risk patterns. This is an inference from ESMA’s description of the reporting framework and its use in supervisory activity.

SFTR is also important because it does not focus only on reporting. The regulation also addresses reuse of collateral and disclosure of SFTs and total return swaps to investors in certain contexts. The European Commission’s summary of the regulation says SFTR establishes EU rules for reporting SFTs to trade repositories, for information on SFTs and total return swaps in fund documentation and reports, and for conditions governing reuse. That matters because transparency is not only for regulators; it also supports market discipline and investor understanding.

In practical financial crime terms, SFTR’s relevance lies in traceability and market observability. A reporting regime that captures details of repos, securities lending, margin lending, and related SFT activity can help supervisors identify concentrations, unusual counterparties, and market practices that deserve further scrutiny. It does not by itself prove market abuse, laundering, or sanctions evasion, but it strengthens the information environment in which such risks can be assessed. This is an inference supported by the Commission’s and ESMA’s descriptions of SFTR as a transparency and monitoring regime.

There is also a UK dimension. The FCA says the UK SFTR introduces requirements to improve transparency and monitor risks associated with the securities financing transactions market, and its reporting-obligation page explains the UK reporting requirements for firms. That means SFTR remains important not only in the EU framework but also in the onshored UK transparency regime for SFTs.

Ultimately, the Securities Financing Transactions Regulation matters in the financial crime environment because it makes a complex part of the capital markets ecosystem more transparent and more monitorable. It is not an AML rulebook in the narrow sense, but it materially strengthens supervisory visibility over securities financing activity, collateral reuse, and related post-trade data. For that reason, SFTR should be understood as a market-transparency framework with real relevance to the broader control environment for misconduct, opacity, and systemic risk.