Sanctions are legal restrictions imposed by governments or supranational bodies to restrict dealings with specified countries, regions, sectors, entities, vessels, or individuals. In the U.S., OFAC says sanctions can be comprehensive or selective and can use asset blocking and trade restrictions to achieve foreign policy and national security goals. In the EU, the European Commission describes sanctions as restrictive measures used under the Common Foreign and Security Policy to prevent conflict or respond to crises, and notes that they are intended to change harmful policies or activities rather than punish for their own sake.

In the financial crime environment, sanctions are significant because they sit at the point where law, geopolitics, payments, trade, and financial services intersect. A sanctions breach is not simply a compliance failure on paper. It can mean that a firm has provided funds, economic resources, trade access, or financial services to a prohibited party or activity. That creates legal, regulatory, operational, and reputational exposure, and in some contexts can also support broader illicit activity such as sanctions evasion, proliferation finance, terrorist financing, or concealed cross-border movement of value. This is an inference supported by the official sanctions frameworks and their focus on blocking or prohibiting dealings with targeted parties and activities.

From a professional perspective, sanctions are not the same as AML, but they overlap closely in practice. AML is primarily concerned with identifying suspicious or illicit funds and reporting or disrupting financial crime risk. Sanctions are more directly prohibitive: they can require firms to freeze assets, block transactions, or refuse dealings involving designated persons, countries, or sectors. OFAC states that sanctions can range from blocking the property of specific persons to broad prohibitions involving an entire country or geographic region. In the UK, OFSI says it helps ensure financial sanctions are properly understood, implemented, and enforced.

This is why sanctions controls are often treated as a distinct but closely related discipline within the wider financial crime framework. A firm may have strong AML monitoring and still fail if it does not identify a designated person, a prohibited sectoral exposure, or a restricted geographic nexus before processing a transaction or providing a service. Conversely, a sanctions alert may also reveal wider AML or fraud concerns, especially where the customer structure, routing, or transaction purpose appears designed to conceal the true counterparty. This is an inference from the structure of sanctions regimes and the way firms operationalize them alongside AML and payment controls.

Watch on YouTube: Sanctions

In practical terms, sanctions can take several forms. They may involve asset freezes, transaction prohibitions, trade embargoes, import or export bans, sectoral restrictions, or limits on the provision of services. OFAC’s public materials expressly say sanctions can include blocking property and trade restrictions, and the European Commission’s sanctions pages similarly refer to bans and restrictions on trade and financial dealings.

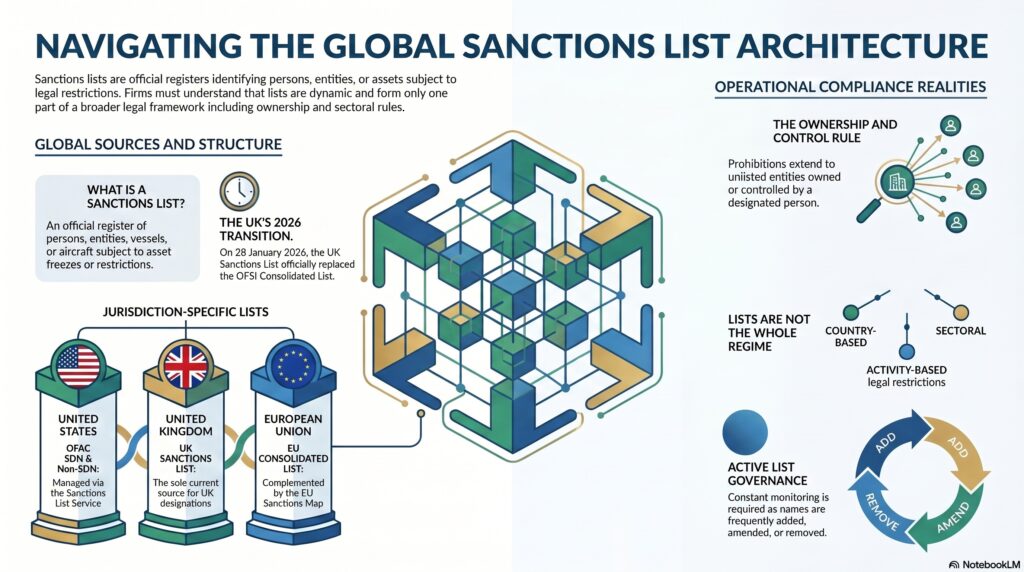

A key control issue is that sanctions compliance depends heavily on accurate identification and transparency. Firms need to know who their customer is, who ultimately owns or controls them, who the counterparties are, where the transaction is going, and whether any party, vessel, jurisdiction, or goods nexus is restricted. That makes sanctions highly dependent on customer due diligence, beneficial ownership review, payment screening, trade controls, and ongoing monitoring. In the UK, the UK Sanctions List is the official list of persons, entities, and ships designated under UK sanctions regulations. OFAC likewise provides current sanctions list data and search tools for immediate download and screening use.

This is also why sanctions screening is not enough on its own. Name screening may identify a direct listed party, but many sanctions risks arise through indirect ownership, control, trade routing, sector exposure, or evasion tactics. A payment may not contain a direct list hit and still be prohibited because it involves a restricted jurisdiction, a blocked ownership chain, or prohibited goods or services. That is a professional inference supported by the breadth of current U.S., UK, and EU sanctions regimes and their use of both list-based and activity-based restrictions.

Sanctions are also a live enforcement issue. In the UK, OFSI says it is responsible for monitoring compliance, assessing suspected breaches, and imposing monetary penalties, and notes that breaches of financial sanctions are a serious criminal offence. That matters because sanctions frameworks are not merely advisory; they are backed by active supervisory and enforcement mechanisms.

Another important feature is that sanctions are dynamic. Lists, programs, FAQs, and restrictions change regularly in response to geopolitical developments. OFAC maintains current sanctions programs and recent actions, OFSI updates UK guidance and FAQs, and the European Commission continues to update sanctions resources and consolidated materials. In March 2026, the UK Sanctions List was updated, and the EU also published updated consolidated FAQ materials in March 2026 relating to sanctions adopted after Russia’s aggression against Ukraine.

Ultimately, sanctions are a core part of the financial crime environment because they determine who a firm may not deal with, what activity it must block or restrict, and how geopolitical restrictions translate into operational controls. They require firms to combine legal interpretation, customer transparency, screening, trade and payment controls, and escalation discipline. For that reason, sanctions should be understood not as a narrow list-management task, but as a major control framework governing whether financial and commercial activity can proceed lawfully at all.