The risk-based approach is the principle that firms should identify, assess, understand, and mitigate financial crime risk in a way that is proportionate to the level and nature of that risk. FATF states that the risk-based approach is central to effective implementation of its standards and means that countries, competent authorities, and firms identify, assess, and understand money laundering and terrorist financing risk and then apply mitigation measures in accordance with the level of risk.

In the financial crime environment, the risk-based approach matters because not all customers, products, channels, jurisdictions, or transactions create the same exposure. A firm serving low-risk domestic retail customers through standard products does not face the same profile as a firm handling cross-border payments, complex corporate structures, correspondent banking, high-risk geographies, or politically exposed persons. The approach exists so firms do not apply the same intensity of control everywhere regardless of risk. FATF and FFIEC both frame this as a way to align controls with real exposure rather than treating all activity identically.

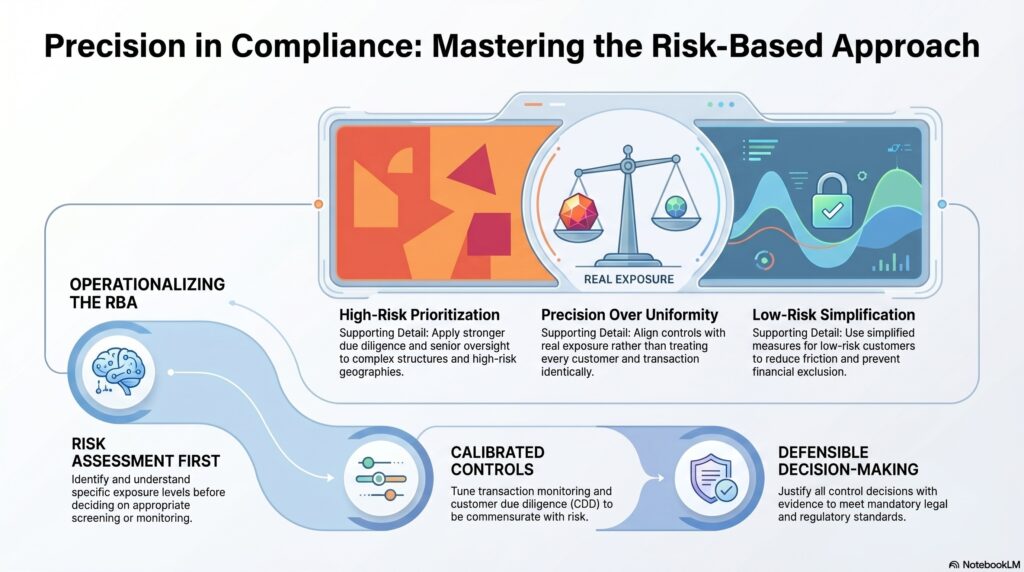

From a professional perspective, the risk-based approach is not a relaxation of standards. It is a method of prioritization and proportionality. Higher-risk areas should receive stronger due diligence, tighter monitoring, and more senior oversight. Lower-risk areas may justify simplified measures where the law allows and where the firm can still explain why the lower risk assessment is reasonable. FATF’s standards were revised to increase focus on proportionality and to require countries to allow and encourage simplified measures in lower-risk areas where appropriate.

Watch on YouTube: Risk-Based Approach

This is why the risk-based approach begins with risk assessment. A firm must understand where its exposure lies before it can decide how much due diligence, screening, monitoring, or escalation is appropriate. FCA findings from its 2025 review of firms’ risk assessment processes focused specifically on how firms identify, understand, assess, mitigate, and manage risk, while FATF’s banking guidance says banks’ identification and assessment of their own ML/TF risk should consider national risk assessments and the legal and regulatory framework.

In practical terms, the risk-based approach usually shapes several core control areas. It determines how customer due diligence is calibrated, when enhanced due diligence is required, how transaction monitoring is tuned, how sanctions and screening controls are prioritized, how fraud and payment controls are applied, and where management attention should be focused. The FFIEC says the level and type of CDD should be commensurate with the risks presented by the customer relationship, which is one of the clearest operational expressions of this approach.

A key professional distinction is that the risk-based approach does not mean firms are free to do whatever they judge convenient. It still requires them to operate within mandatory legal standards and to justify their decisions with evidence. The FCA’s Financial Crime Guide says firms must put in place systems and controls to identify, assess, monitor, and manage money laundering, terrorist financing, and proliferation-financing risk, while the Guide is designed to help firms adopt a more effective, risk-based, and outcomes-focused approach to mitigating financial crime risk.

The approach is also important because it helps avoid two opposite failures. One is under-control, where higher-risk activity is treated too lightly and the firm misses real exposure. The other is over-control, where lower-risk customers or activities are subjected to unnecessary friction, cost, or exclusion without clear benefit. FATF’s recent financial inclusion work is explicit that a risk-sensitive approach should also consider the risks of financial exclusion and the benefits of bringing people into the regulated financial system.

This matters especially in payments and fraud. The FCA’s 2024 finalised guidance on a risk-based approach to payments was issued to support firms in tackling APP fraud while still allowing payment services to function proportionately. That illustrates a wider point: the risk-based approach is not confined to AML onboarding. It is a broader control principle for deciding when stronger intervention is justified and when smoother processing is appropriate.

Ultimately, the risk-based approach is central to the financial crime environment because it is the method by which firms turn broad legal obligations into proportionate, defensible, and effective controls. It ensures that attention and resources are focused where financial crime risk is greatest, while avoiding a rigid one-size-fits-all model that can be both ineffective and unnecessarily burdensome.