Risk assessment is the process by which a firm identifies, understands, evaluates, and prioritizes the financial crime risks to which it is exposed, so that it can apply controls proportionate to those risks. FATF describes the risk-based approach as one in which countries, competent authorities, and firms identify, assess, and understand money laundering and terrorist financing risk and then take mitigation measures in line with the level of risk. The FFIEC similarly says a BSA/AML risk assessment should provide a comprehensive analysis of a bank’s money laundering, terrorist financing, and other illicit financial activity risks.

In the financial crime environment, risk assessment is significant because it is the starting point for almost every serious control decision. A firm cannot apply customer due diligence, sanctions controls, fraud monitoring, transaction monitoring, escalation thresholds, or governance oversight proportionately unless it first understands where its exposure actually lies. The FCA’s November 11, 2025 findings on firms’ risk assessment processes say its review focused on how firms identify, understand, assess, mitigate, and effectively manage risk.

From a professional perspective, risk assessment is not a paper exercise or a one-time regulatory deliverable. It is the analytical foundation of the risk-based approach. FATF’s guidance states that the risk-based approach is central to effective implementation of the FATF Recommendations, and the FFIEC says the risk assessment helps the bank apply appropriate risk-management processes to mitigate risk and comply with BSA requirements. In practice, that means risk assessment should actively shape the compliance program rather than sit beside it.

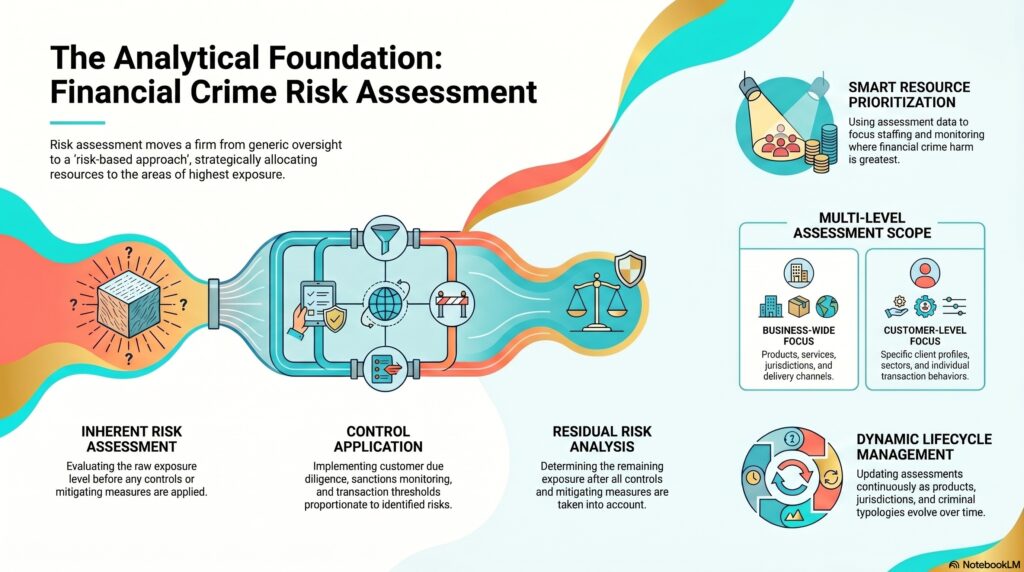

A mature financial crime risk assessment usually operates at more than one level. At the broadest level, firms conduct a business-wide risk assessment to understand their exposure across products, services, customers, jurisdictions, channels, and delivery models. At a more granular level, they conduct customer risk assessments, and in some cases product, channel, or transaction-level assessments as well. The FCA’s 2025 multi-firm review specifically examined both business-wide risk assessment and customer risk assessment processes.

Watch on YouTube: Risk Assessment

This matters because financial crime exposure is rarely uniform across the business. Some customers are higher risk than others. Some products are easier to misuse. Some jurisdictions create greater sanctions, corruption, or ML/TF exposure. Some delivery channels reduce transparency or increase fraud vulnerability. FATF’s national risk assessment guidance and sector guidance both emphasize that the risk-based approach depends on identifying, assessing, and understanding the risks to which firms are exposed before applying controls.

In practical terms, a strong risk assessment asks several core questions. What kinds of financial crime are relevant to the firm: money laundering, terrorist financing, fraud, sanctions evasion, market abuse, bribery, corruption, or proceeds-of-crime movement? Which customers, sectors, jurisdictions, payment routes, and business models are most exposed? Which controls are already in place, and how effective are they? Where are the residual risks highest after mitigation? The FFIEC says the purpose of the BSA/AML risk assessment is to help identify and mitigate gaps in controls and to support a risk-based monitoring system for higher-risk products, services, customers, and geographies.

A key professional distinction is between inherent risk and residual risk. Inherent risk is the level of financial crime exposure before controls are considered. Residual risk is what remains after the firm’s controls and mitigating measures are taken into account. A firm offering cross-border payments, correspondent banking, high-risk jurisdictions, or wholesale market access may have substantial inherent risk even if its controls are strong. Good risk assessment does not hide that exposure; it makes it visible and assesses whether the current control environment is sufficient. This is an inference supported by the FFIEC’s linkage of risk assessment to control gaps and to the BSA/AML compliance program.

Risk assessment is also closely tied to control design and resource allocation. FATF said in August 2025 that a risk-based approach ensures smart prioritization of resources to combat financial crime where it is doing the most harm. In operational terms, that means a firm should use risk assessment to decide where enhanced due diligence is needed, where monitoring should be tighter, where specialist staffing is required, and where governance attention should be focused.

This is why weak risk assessment is such a serious control failure. If the assessment is generic, outdated, unsupported by data, or disconnected from actual business activity, the firm may end up applying the wrong controls to the wrong risks. The FCA’s 2025 findings were published specifically to help firms reflect on whether they are meeting existing risk assessment requirements and highlighted both good and poor practice in how firms identify, assess, and mitigate risk.

A professionally mature risk assessment is also dynamic. It should be updated when products change, new jurisdictions are entered, customer profiles shift, criminal typologies evolve, or control weaknesses are found. The FFIEC says banks should have a process for updating the BSA/AML risk assessment as necessary to reflect changes in products, services, customers, and geographic locations so it remains an accurate reflection of the bank’s risks.

Governance is central throughout. Senior management should understand the methodology, assumptions, and outputs of the risk assessment, and should be able to show how the results influence policy, controls, monitoring, and risk appetite. The FCA’s financial crime materials continue to emphasize that firms must be an effective line of defence against financial crime, which in practice depends on governance having a realistic picture of exposure rather than a formal one.

Ultimately, risk assessment is one of the most important disciplines in the financial crime environment because it determines whether a firm understands the risks it is trying to control. It is the bridge between regulatory expectation and operational prioritization. Without effective risk assessment, controls become generic, resources are misallocated, and the firm is more likely to miss the areas where misuse of the financial system is most likely to occur.