Regulatory compliance is the discipline through which a firm ensures that its activities, controls, and decisions conform to applicable laws, regulations, regulatory expectations, and internal standards. In the financial crime environment, this means translating requirements relating to anti-money laundering, sanctions, fraud prevention, market conduct, customer protection, suspicious activity reporting, and governance into practical, demonstrable control arrangements.

From a professional perspective, regulatory compliance is not simply about avoiding fines or maintaining a rulebook. It is the framework that connects legal obligation to operational reality. A firm may understand the text of a regulation, but if it cannot embed that requirement into customer onboarding, transaction monitoring, sanctions screening, employee conduct, surveillance, escalation, and remediation processes, it is not truly compliant in any meaningful sense. In that way, regulatory compliance is both an interpretive function and a control function.

In the financial crime environment, regulatory compliance is especially important because firms operate in areas where misuse of the financial system can cause direct customer harm, market harm, legal exposure, and reputational damage all at once. Financial institutions are expected not only to refrain from wrongdoing themselves, but also to maintain systems and controls that reduce the risk of being used by others for money laundering, fraud, sanctions evasion, bribery, corruption, market abuse, or other illicit conduct. Regulatory compliance is the mechanism through which those expectations are understood, assigned, and tested.

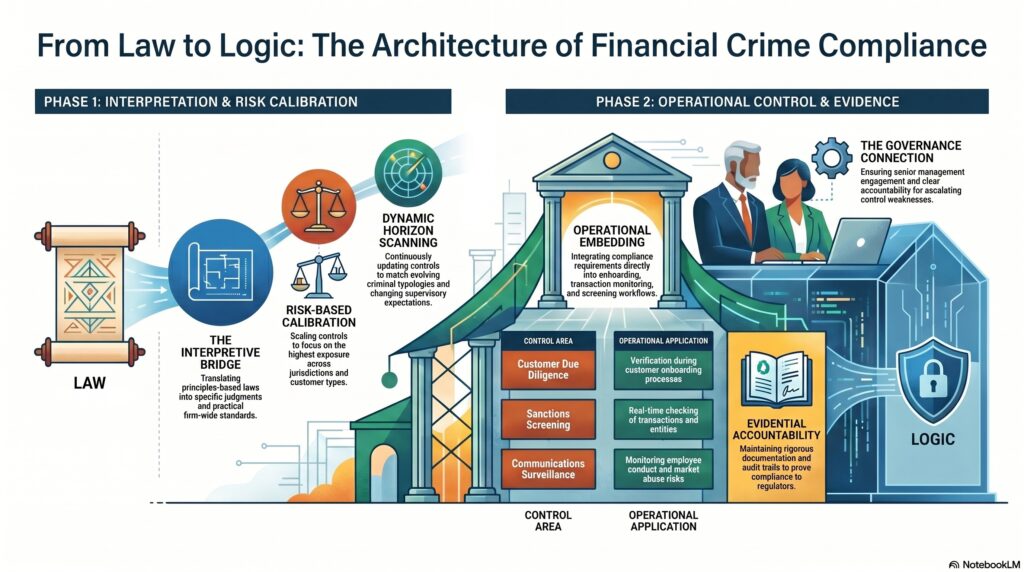

A central feature of regulatory compliance is interpretation. Financial regulation is often principles-based, risk-based, or written at a level that requires firms to apply judgment. Regulations may require “effective systems and controls,” “proportionate measures,” or “enhanced due diligence” without prescribing every operational step in detail. Compliance therefore involves understanding what the rule requires in context, how that requirement applies to the firm’s products and services, and what evidence will show that the requirement is being met. In practice, this means compliance is as much about interpretation and challenge as it is about documentation.

Watch on YouTube: Regulatory Compliance

This is why regulatory compliance is closely linked to governance. A firm cannot demonstrate compliance credibly unless roles and responsibilities are clear, senior management is engaged, policies are current, decisions are documented, and control weaknesses are escalated and remediated properly. Regulatory compliance depends on more than technical expertise in laws and rules. It depends on whether the institution has a functioning governance structure capable of turning those rules into accountable action across the business.

In the financial crime environment, regulatory compliance usually spans a wide range of control areas. These include customer due diligence, enhanced due diligence, beneficial ownership review, sanctions screening, transaction monitoring, fraud controls, suspicious activity escalation, employee conduct, communications surveillance, recordkeeping, training, and regulatory reporting. What unites these areas is not that they all belong to the same team, but that they all sit within the wider obligation to operate lawfully, transparently, and with controls proportionate to the firm’s risk profile.

A professionally mature regulatory compliance framework is therefore risk-based. Not every customer, product, or transaction requires the same level of scrutiny, and not every rule creates the same type of risk. Compliance helps the firm understand where its greatest exposure lies and how controls should be calibrated accordingly. This is particularly important in financial crime, where jurisdictions, customer types, delivery channels, and criminal typologies vary significantly. A compliance framework that is too generic may appear comprehensive on paper while missing the actual risks that matter most in practice.

Regulatory compliance is also fundamentally evidential. It is not enough for a firm to say that it takes financial crime seriously. It must be able to show what its obligations are, how it interpreted them, which controls were designed to meet them, how those controls are monitored, what issues have arisen, and how those issues have been addressed. Policies, procedures, management information, case records, approval logs, training records, audit findings, and remediation tracking all form part of the evidence base. In regulated environments, the ability to evidence compliance is often almost as important as the underlying control itself.

Another important aspect is that regulatory compliance is dynamic rather than static. Laws change, supervisory expectations evolve, typologies shift, technology develops, and firms themselves change products, channels, and operating models. A control that was compliant and proportionate two years ago may no longer be adequate today. This means regulatory compliance requires horizon scanning, periodic review, control testing, and an ability to respond to regulatory developments without waiting for a formal breach to reveal the problem.

In the financial crime environment, regulatory compliance also acts as a bridge between the first line of defense and independent oversight functions. The business owns and operates many controls directly, but compliance provides interpretation, guidance, challenge, monitoring, and escalation. It helps ensure that commercial activity does not drift away from regulatory obligations and that control failures are not treated as isolated operational inconveniences when they may in fact create serious legal or supervisory exposure. In this sense, compliance is one of the main disciplines that preserves the integrity of the control framework over time.

Ultimately, regulatory compliance is central to the financial crime environment because it is the structured process through which firms understand what is required of them and turn those requirements into practical control. It protects the firm not only from regulatory breach, but from the deeper risk of operating with policies, systems, and decisions that are disconnected from legal and supervisory expectations. For that reason, regulatory compliance should be understood not as a narrow technical function, but as a core element of governance, accountability, and financial crime resilience.